CALGARY, ALBERTA–(Marketwired – Dec. 14, 2016) – Athabasca Oil Corporation (TSX:ATH) (“Athabasca” or “the Company”) is pleased to announce that is has entered into agreements with Statoil ASA (“Statoil”) and its wholly owned subsidiary Statoil Canada Ltd. to acquire its Canadian Thermal Oil assets for consideration of $435 million cash, 100 million common shares and contingent value payments triggered at oil prices above US$65/bbl WTI. The acquired assets include the operating Leismer Thermal Oil Project (currently producing 24,000 bbl/d), the delineated Corner lease and related strategic infrastructure. The acquisition establishes Athabasca as an intermediate oil weighted growth company with a production base of approximately 40,000 boe/d (2017e). Upon closing, cash flow from the low decline production base will support thermal sustaining capital requirements and economic growth in the liquids rich Montney and Duvernay resource plays.

Mr. Robert Broen, Athabasca’s President and Chief Executive Officer said, “This transaction is transformational for Athabasca and establishes scale with top tier thermal assets and people. We are pleased to have Statoil, a global energy leader, as an investor in the Company. Shareholders are positioned with a unique and compelling return proposition. Athabasca has the financial strength to drive oil weighted growth at competitive metrics in the current environment.”

Mr. Paul Fulton, President, Statoil Canada, said “We are pleased to announce this agreement with Athabasca. The transaction allows Statoil to redeploy proceeds to our global portfolio of opportunities. We firmly believe Athabasca is very well placed to continue the development of these assets.”

The acquisition complements Athabasca’s strategy and positions the Company for strong growth and financial sustainability into the future:

The acquisition complements Athabasca’s strategy and positions the Company for strong growth and financial sustainability into the future:

- Light Oil: Defined and Material Growth – A scalable operated Montney position and funded Duvernay development through the joint venture with Murphy Oil Company Ltd. (“Murphy”).

- Thermal Oil: Leverage to Oil Prices – A large low decline asset base accelerates free cash flow generation with future low risk expansion options.

- Financial Sustainability – Maturing cash flow profile with a significantly stronger sustainability metrics. A diverse asset base provides flexibility in future capital allocation decisions.

Throughout 2016, Athabasca has executed a number of strategic transactions aimed at securing a funding model for its core plays and monetizing long dated resources. These transactions have helped Athabasca transform into a unique intermediate oil Company with meaningful exposure to several of the largest resource plays in Western Canada.

The Acquisition

Asset Highlights

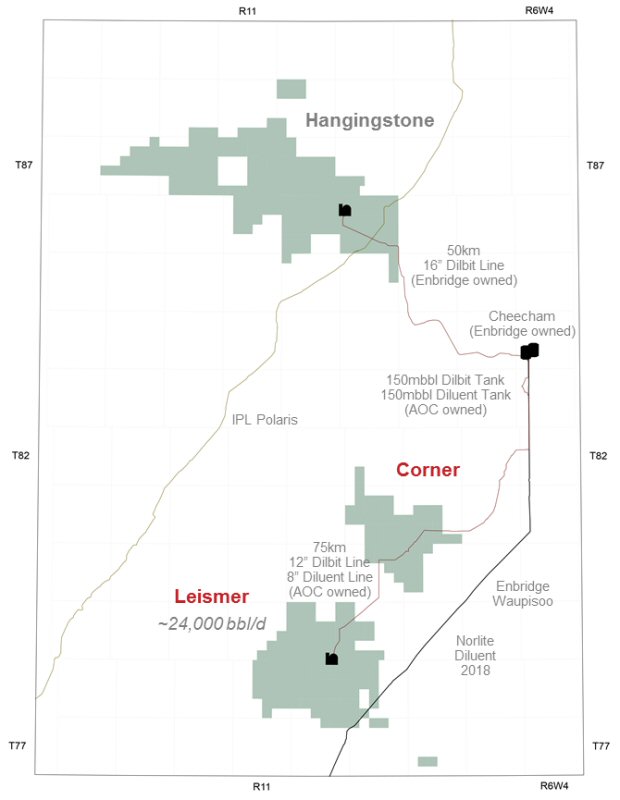

Statoil’s Canadian Thermal Oil assets include the producing Leismer lease, delineated Corner lease and strategic regional infrastructure.

The Leismer project was commissioned in 2010 with current production of approximately 24,000 bbl/d. The project has proved reserves in place to support a flat production profile for over 30 years and a reserve life index approximately 70 years (proved plus probable). Athabasca intends to maintain a stable production base for the foreseeable future. The Leismer and Corner leases have received regulatory approval for future development phases up to a combined 80,000 bbl/d.

The assets are high quality and resilient to lower commodity prices. Leismer’s current steam oil ratio (“SOR”) of ~2.7x ranks it as one of the lowest among operating projects in the basin. Operating income break-even is estimated at ~US$44/bbl WTI. In Q4 to date, the assets generated approximately $9 million of operating income per month at an average WTI price of approximately $48/bbl. Over the next five years, the Company estimates that Leismer will generate free cash flow in excess of $575 million and $325 million under US$60/bbl WTI and strip commodity forecasts (Dec. 3, 2016), respectively.

Strategic infrastructure includes ownership of dilbit and diluent pipelines from Leismer to Cheecham Terminal, 300,000 barrels of storage capacity at the Cheecham Terminal and access to multiple sales points with marketing agreements on the Enbridge Waupisoo and optionality on the Kinder Morgan Trans Mountain pipeline expansion.

Strategic Rationale

- Transitions Asset Portfolio to a More Sustainable Business Model – Throughout 2016, Athabasca has significantly strengthened its balance sheet through the Light Oil joint venture with Murphy ($486 million total consideration) and the Thermal Oil Contingent Bitumen Royalty granted to Burgess Energy ($307 million cash consideration; amended terms outlined in the financing section below). These transactions secured creative funding for Athabasca’s core plays and established the financial flexibility to acquire very high quality assets.

- Bolsters Sustainability Metrics and Accelerates Free Cash Flow Generation – The assets immediately drive a larger cash flow base and accelerate the Company’s transition to sustainable free cash flow generation, which is expected in early 2018 at US$60/bbl WTI or early 2019 on strip pricing (Dec. 3).

- Significant Flexibility in Capital Allocation – Upon closing, cash flow from the low decline production base will support thermal sustaining capital requirements and meaningful economic growth in the liquids rich Montney (150 – 200 locations) and Duvernay (1,500 locations) resource plays.

- Highly Accretive to Cash Flow and Reserves Per Share – The acquisition is forecasted to be highly accretive on key operating and financial metrics within the Company’s five year forecast period. Specifically, 275% and 60% accretive on 2017 and 2018 cash flow per basic share (strip pricing Dec. 3) respectively and approximately 250% accretive on proved plus probable reserves per share.

- Scale in the Thermal Oil Division with Low Risk Expansion Opportunities – A 33,000 bbl/d low decline thermal production base lowers operating break evens and improves resiliency to challenging oil prices. The Company has regulatory approval for expansions up to a combined 80,000 bbl/d from the Leismer, Hangingstone and Corner leases.

- Strengthened Reserve Base – The assets enhance the Company’s reserve base by adding 31 mmbbl proved developed producing, 291 mmbbl proved and 856 mmbbl proved plus probable reserves. The Company’s estimate for corporate pro forma proved plus probable reserves is approximately 1,100 mmbbl with a 75 year reserve life index based on 2017 forecasted production.

- Strategic Thermal Oil infrastructure – The assets include key strategic infrastructure and marketing agreements which provide access to multiple end markets. Combined with Hangingstone volumes, the company will have opportunities for commercial synergies in the future.

- Best-in-Class Innovation and Sustainable Development – Statoil is recognized as an industry leader in energy efficiency and reducing carbon dioxide emissions per barrel of produced oil. Statoil has invested significantly in technology for application on Thermal projects to increase development efficiency and lower overall carbon footprint. Leismer and Corner are top tier leases which will improve Athabasca’s overall asset quality with a net benefit to the Company’s already high environmental standards.

Acquisition Mechanics and Metrics

Consideration for the Acquisition is as follows:

- Cash – $435 million funded through cash on hand.

- Equity – 100 million common shares of Athabasca. Statoil will become an investor in Athabasca with just under 20% basic ownership.

- Contingent Value Payments – Athabasca has agreed to a series of contingent value payments over a four year term ending in 2020. The annual payment is calculated as: 33% of Leismer Bitumen Production x Oil Factor (Monthly Average WTI less US$65/bbl adjusted for inflation). The payment is capped at $75 million annually and $250 million over the term. For context, at US$65/bbl the Leismer asset is expected to have an operating income of approximately $215 million with no contingent value payment, at US$75/bbl an estimated operating income of approximately $315 million with a $39 million contingent value payment. Under strip commodity pricing the Company does not expect to make any contingent payments over the four year term.

The Acquisition will have an effective date of January 1, 2017 with closing anticipated in the first quarter of 2017. The Acquisition is subject to usual closing conditions and regulatory approvals, including TSX approval, and is not subject to a financing condition.

| ACQUISITION HIGHLIGHTS AND METRICS | |

| Purchase Price1 | $582MM |

| Current Production | ~24,000 bbl/d |

| Proved Reserves & NPV10 BT2 | 291 mmbbl & $1,549MM |

| Proved plus Probable Reserves & NPV10 BT2 | 856 mmbbl & $2,574MM |

| Contingent Resource (Best Estimate Unrisked)3 | 628 mmbbl |

| 2017e Cash Flow4 | $90 – 105MM |

| $/bbl/d Current Production | ~$24,000/bbl/d |

| $/boe Proved + Probable | $0.68/boe |

| P/CF | ~5.8x |

| Notes: | |

| 1. | A $582 million purchase price reflects $435 million cash and 100 million Athabasca common shares at $1.47 per share. |

| 2. | Preliminary GLJ & Associates reserve evaluation as at November 30, 2016. |

| 3. | Preliminary GLJ & Associates resource evaluation as at November 30, 2016. Best Estimate Contingent Resources Unrisked. |

| 4. | Management estimate based on preliminary 2017 production and cash flow based on December 3, 2016 strip price outlook. |

Acquisition Financing and Balance Sheet Update

The cash component of the purchase price will be sourced from existing cash balances. In 2017, the Company intends to access the capital markets to refinance its Senior Secured Second Lien Notes (the “Notes”). Athabasca also notes the following:

- Existing Cash on Hand – Athabasca’s current cash balance is approximately $760 million.

- Expanded Credit Facilities – The Company is in discussions with its banking syndicate to establish a new reserve based loan facility. The acquisition significantly enhances the Company’s cash flow profile and proved developed producing reserve base.

- Hedging – In conjunction with the acquisition, the Company is evaluating hedging opportunities and plans to hedge up to 50% of 2017 corporate production. The hedge program will be designed to protect a base level of cash flow to support capital plans and has the potential to expand reserve based loan facilities.

- Amended Contingent Bitumen Royalty – The Company is amending its existing Contingent Bitumen Royalty (the “Royalty”) with Burgess Energy Holdings LLC (“Burgess”) for additional cash proceeds of $50 million. The amendment includes converting the existing sliding scale to a linear scale and is based on the Western Canadian Select (“WCS”) benchmark. The minimum trigger for the Royalty is US$60/bbl WCS for Hangingstone and US$70/bbl WCS for the Company’s other Thermal assets (Dover West, Birch and Grosmont). Following close, which is anticipated in conjunction with closing of the Statoil acquisition or earlier, total cash proceeds raised through the Royalty will be $307 million. There is no Royalty assigned to the newly acquired Leismer or Corner assets.

- Anchor 2017 Notes Refinancing Commitment – The Company has advanced discussions with a number of existing and potential investors regarding its refinancing plans and has secured an anchor commitment of $125 million towards a new debt instrument.

The acquisition significantly bolsters Athabasca’s credit quality and cash flow profile. The Company forecasts a low decline production base of approximately 40,000 boe/d (~90% liquids, 2017e) and intends to optimize its capital structure to ensure a multi-year funding outlook. The Company anticipates net debt to cash flow metrics of less than

Outlook

The Company maintains significant flexibility to adapt its capital expenditures to external market conditions.

In the Light Oil division, Athabasca intends to complete its winter program in the Montney at Placid which will include the drilling of 20 horizontal wells and the completion and tie-in of 12 wells by spring break-up. Capital for the Montney is forecasted at approximately $115 – 125 million. In the Duvernay, 2017 joint venture plans are being finalized with Murphy and the joint development agreement contemplates approximately $200 million of gross capital ($15 million net) with the majority of spending directed towards drilling and completion operations across the acreage base.

In the Thermal Oil division, activity will be focused on maintaining a stable production base on the acquired assets and the continued ramp-up of Hangingstone to design capacity. 2017 Capital is expected to be approximately $90 – 110 million, with the majority on the newly acquired Leismer asset.

The Company will release its official capital budget and guidance in conjunction with closing of the acquisition.

| Preliminary 2017 Operational & Financial Guidance | Full Year | |

| CORPORATE (net) | ||

| Production (boe/d) | 38,000 – 42,000 | |

| Liquids Weighting (%) | ~90% | |

| Funds Flow from Operations1 ($MM) | ~$90 | |

| THERMAL OIL | ||

| Bitumen Production1 (bbl/d) | 31,500 – 34,500 | |

| Operating Income ($MM) | ~$90 | |

| LIGHT OIL | ||

| Production1 (boe/d) | 6,500 – 7,500 | |

| Operating Income ($MM) | ~$80 | |

| COMMODITY ASSUMPTIONS (strip pricing as at Dec. 3, 2016) | ||

| WTI (US$/bbl) | $54.25 | |

| Edmonton Par (C$/bbl) | $68.00 | |

| Western Canadian Select (C$/bbl) | $50.50 | |

| AECO Gas (C$/mcf) | $3.15 | |

| FX (US$/C$) | 0.75 | |

| Notes: | |

| 1. | Reflects full year impact of the Statoil asset acquisition. Jan. 1, 2017 effective date with closing expected in Q1 2017, volumes and cash flows will be adjusted to reflect a closing adjustment. |

| 2. | Corporate funds flow based on mid-points of guidance and debt refinancing assumptions similar to current capital structure. |

Advisors

Goldman Sachs Canada Inc. and TD Securities Inc. are acting as financial advisors for Athabasca in connection with the acquisition.

Conference Call

A conference call to discuss the acquisition will be held for the investment community on Thursday, December 15, 2016 at 7:00 a.m. MT (9:00 a.m. ET).

| Conference Call Details: |

| Date: Thursday, December 15, 2016 |

| Time: 7:00am MT (9:00am ET) |

| Dial In: (877) 291-4570 (toll-free in North America) or (647) 788-4919 |

| Replay: (800) 585-8367 (toll-free in North America) or (416) 621-4642 |

| Replay code: 38582031 |

| Webcast Details: |

| http://www.gowebcasting.com/8268 |

About Athabasca Oil Corporation

Athabasca Oil Corporation is a Canadian energy company with a focused strategy on the development of thermal and light oil assets. Situated in Alberta’s Western Canadian Sedimentary Basin, the Company has amassed a significant land base of extensive, high quality resources. Athabasca’s common shares trade on the TSX under the symbol “ATH”. For more information, visit www.atha.com.

{kind=link}