2012 Highlights

Operational Highlights

| Three Months Ended December 31 |

Twelve Months Ended December 31 |

|||||||||

| 2012 | 2011 | % Change | 2012 | 2011 | % Change | |||||

| Crude oil (bbls/d) | 400 | 1,305 | (69 | ) | 696 | 1,200 | (42 | ) | ||

| Field condensate (bbls/d) | 165 | 131 | 26 | 213 | 121 | 76 | ||||

| Natural gas liquids (bbls/d) | 1,055 | 1,405 | (25 | ) | 1,101 | 1,217 | (10 | ) | ||

| Total crude oil and natural gas liquids | 1,620 | 2,841 | (43 | ) | 2,010 | 2,538 | (21 | ) | ||

| Natural gas (mcf/d) | 33,654 | 38,973 | (14 | ) | 37,589 | 37,992 | (1 | ) | ||

| Total (boe/d) | 7,229 | 9,337 | (23 | ) | 8,276 | 8,870 | (7 | ) | ||

| Financial Highlights ($ thousands except per unit amounts) | |||||||||||||||

| Three Months Ended December 31 |

Year Ended December 31 |

||||||||||||||

| 2012 | 2011 | % Change | 2012 | 2011 | % Change | ||||||||||

| Petroleum and natural gas sales | 18,858 | 33,115 | (43 | ) | 85,754 | 126,887 | (32 | ) | |||||||

| Per boe | 28.35 | 38.55 | (26 | ) | 28.31 | 39.19 | (28 | ) | |||||||

| Funds from operations | 6,269 | 17,081 | (63 | ) | 32,305 | 66,872 | (52 | ) | |||||||

| Per boe | 9.43 | 19.89 | (53 | ) | 10.65 | 20.65 | (48 | ) | |||||||

| Per share – Basic | 0.04 | 0.14 | (71 | ) | 0.24 | 0.57 | (58 | ) | |||||||

| Per share – Diluted | 0.04 | 0.14 | (71 | ) | 0.24 | 0.56 | (57 | ) | |||||||

| Net earnings (loss) | (29,394 | ) | 825 | (3,663 | ) | (58,030 | ) | 11,602 | (600 | ) | |||||

| Per boe | (44.19 | ) | 0.96 | (4,703 | ) | (19.18 | ) | 3.58 | (636 | ) | |||||

| Per share – Basic | (0.21 | ) | 0.01 | (2,200 | ) | (0.43 | ) | 0.10 | (530 | ) | |||||

| Per share – Diluted | (0.21 | ) | 0.01 | (2,200 | ) | (0.43 | ) | 0.10 | (530 | ) | |||||

| Capital invested | 11,538 | 37,282 | (69 | ) | 83,728 | 114,477 | (27 | ) | |||||||

| Disposition of properties | (45 | ) | (4,835 | ) | (99 | ) | (34,664 | ) | (12,873 | ) | 169 | ||||

| Net capital invested | 11,493 | 32,447 | (65 | ) | 49,064 | 101,604 | (52 | ) | |||||||

| Acquisition of properties | 139 | 56 | 148 | 139 | 273 | (49 | ) | ||||||||

| Total capital invested | 11,632 | 32,503 | (64 | ) | 49,203 | 101,877 | (52 | ) | |||||||

| December 31, 2012 |

December 31, 2011 |

% Change | ||||

| Debt plus working capital deficiency (1) | 92,815 | 95,632 | (3 | ) | ||

| Total assets | 401,649 | 447,073 | (10 | ) | ||

| Shares outstanding (thousands) | ||||||

| Basic | 153,049 | 131,000 | 17 | |||

| Diluted | 162,104 | 141,591 | 14 | |||

| (1) | excludes fair value of financed instruments. |

MESSAGE TO SHAREHOLDERS

2012 was an exciting year for Delphi as the Company initiated its development of the East Bigstone Montney project and began the transition to a condensate-rich natural gas resource based growth platform, mitigating an ongoing challenging natural gas pricing environment.

Year in Review

During 2012, Delphi made significant progress in advancing its condensate-rich Montney play at East Bigstone. Since commissioning its 100 percent owned compression and dehydration facility in May 2012, the Company averaged approximately 1,200 boe/d (30 percent or 68 barrels per million cubic feet (“bbls/mmcf”) NGL”s) from the three Montney horizontal wells drilled during the year. Condensate represented 62 percent of the total NGL production. Subsequent to year end, Delphi has drilled an additional three Montney wells, two of which have already been completed and are now on production. Current production over the past 14 days from the five wells now on production has averaged approximately 3,850 boe/d (37 percent or 95 bbls/mmcf NGL”s). The optimization of the Company”s drilling and completions techniques resulting in significantly enhanced production performance will have a positive impact on the play economics and overall corporate performance.

In December 2012, Delphi also increased its exposure in its Bigstone Montney area with an industry farm-in agreement to earn up to a 75 percent working interest in 35 sections of Montney and Nordegg petroleum and natural gas (“PNG”) rights. Upon full earning, the Company will grow its land position by nearly 60 percent from 41.7 net sections to approximately 66.2 net sections. The farm-in nearly doubles the East Bigstone low-risk development drilling inventory in the proven upper and middle Montney formations.

The total capital program in 2012 was $83.9 million with approximately 75 percent of the expenditures directed to the Montney development project at Bigstone drilling four gross (3.75 net) wells and constructing the required facility and major gathering system infrastructure. The Company directed approximately $24.3 million or 29 percent of its capital expenditures to new facility and pipeline construction. In total the Company drilled seven gross (6.5 net) wells, including one net well that was drilled in the fourth quarter of 2012 but not completed. This compares to 30 gross (23.8 net) wells drilled in 2011. Strategic non-core asset disposition proceeds of $34.7 million were utilized to partially fund the capital program resulting in net capital expenditures in 2012 of $49.2 million.

Production during the fourth quarter 2012 of 7,229 boe/d and full year 2012 production of 8,276 boe/d were negatively impacted by the property dispositions during the year. Disposition production volumes totalled approximately 667 boe/d (54 percent light oil).

Financial results in 2012 were also affected by lower commodity prices, particularly lower natural gas prices, with Canadian benchmark natural gas prices decreasing 34 percent to average $2.39 per million cubic feet in 2012. Funds from operations decreased 52 percent to $32.3 million for 2012 as a result of a seven percent decline in average production and a 27 percent reduction in the realized sales price per boe as compared to 2011.

Petroleum and natural gas reserve additions from the capital program increased the Company”s reserve life index to 14.2 years. Total proved plus probable reserves increased in 2012 by seven percent to 43.0 million boe.

At December 31, 2012, unutilized credit available on the Company”s $125.0 million banking facilities was nearly $32.1 million (26 percent of available bank facilities), providing support for the Q1 2013 capital program.

Delphi”s undeveloped land position at December 31, 2012, a measure of its future growth prospect inventory, was 196,543 net acres (307 sections). The Company has regulatory approval to drill up to four natural gas wells per pool per section on its lands at its three core properties of Bigstone, Hythe and Wapiti. Delphi increased its land holdings in 2012 (including the farm-in lands) on its East Bigstone Montney play to 78.5 gross (66.2 net) sections.

Bigstone Montney Program

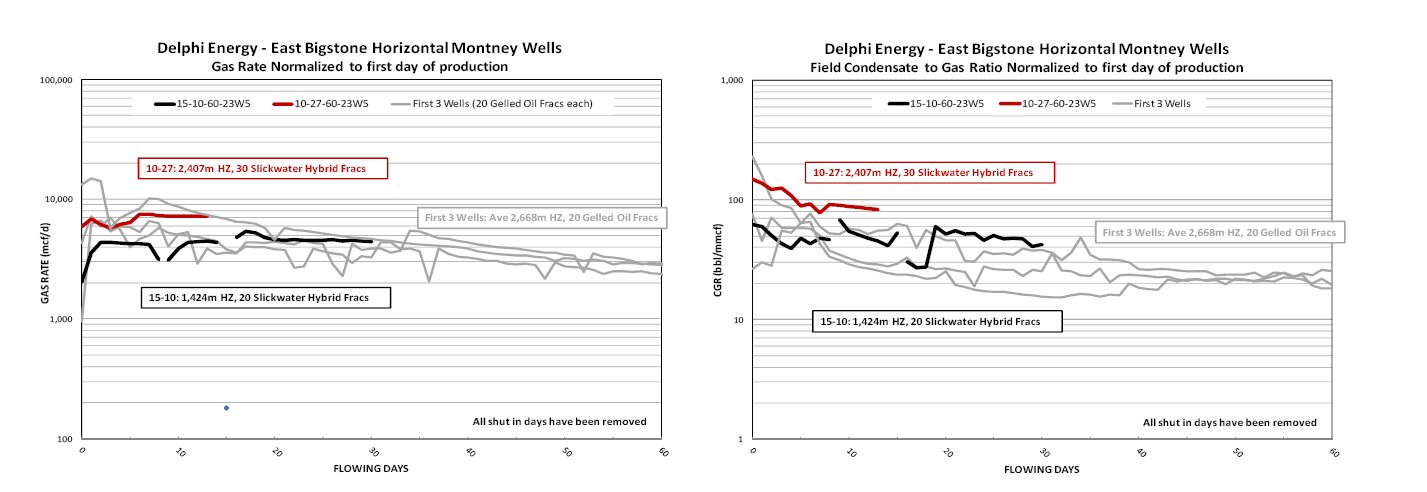

At East Bigstone, Delphi recently brought its fifth horizontal Montney well on production. The 10-27-60-23W5 well was drilled during the first quarter of 2013 to a total depth of 5,260 metres with a horizontal lateral length of 2,407 metres. The well was completed with a 30 stage (all of which were successful) slickwater hybrid completion. The well was brought on production on March 5, 2013 through the Company”s Montney compression and dehy facility and over the first 14 full days of production, averaged 6.8 million cubic feet per day (“mmcf/d”) of raw gas with associated field condensate production averaging 101 bbls/mmcf of raw gas. Including plant recovered liquids (estimated to be 35 bbls/mmcf raw gas), the average rate over this time period is estimated to be 1,917 boe/d. Total liquids production over this period contributed 921 bbls/d, 80 percent of which is field and plant recovered condensate. The well has recovered approximately 26 percent of the initial load frac water volumes to date. Current total production from the well is consistent with the 14 day average, with a current field produced condensate to gas ratio of 83 bbls/mmcf raw gas. The 10-27 well is expected to payout in less than one year.

The previously reported 15-10-60-23W5 well, completed with a 20 stage (all of which were successful) slickwater hybrid completion, has now been on production for 30 days and continues to outperform Company expectations. Over this period, the well averaged 4.2 mmcf/d of raw gas with associated field condensate production averaging 43 bbls/mmcf of raw gas. Including plant recovered natural gas liquids (estimated to be 35 bbls/mmcf raw gas), the average production over this time period is estimated to be 940 boe/d. Total liquids production over this period contributed 326 bbls/d, 65 percent of which is field and plant recovered condensate. The well has recovered approximately 38 percent of the initial load frac water volumes to date. Current production and field produced condensate to gas ratio is consistent with the 30 day average. This well was drilled with a shorter horizontal lateral length of 1,424 metres to assess the new completion liner and frac technique. Although it is the shortest horizontal well the Company has drilled, it is anticipated, based on initial production data, to outperform the first three horizontal Montney wells the Company drilled in East Bigstone, validating the new completion technique.

Initial results of both the 10-27 and 15-10 wells have surpassed the Company”s expectations. As a result of the new completion technique employed, both wells are exhibiting shallower initial declines than the Company”s first three wells drilled in East Bigstone (which were completed with gelled oil fracs). In addition, both wells are also producing at higher field condensate to gas ratios compared to the first three wells that average approximately 25 bbls/mmcf raw gas.

The following charts show the performance of the two new wells compared to the first three wells the Company drilled. Production data has been normalized and days during which the wells were shut-in have been removed from the plots to appropriately compare gas flow rates and field produced condensate to gas ratio.

To view the charts, please visit the following link: http://media3.marketwire.com/docs/320dee_graph.jpg

The Company is in the final stages of drilling operations at its third horizontal Montney well of the winter program at 16-23-60-23W5. The well was drilled to a final total depth of 5,753 meters with a horizontal lateral length of 2,809 meters making it the second longest horizontal well the Company has drilled. Completion operations are anticipated to commence after spring break-up and will consist of a 30 stage slickwater hybrid completion. The well has been tied-in to the Company”s Montney facility in order to bring the volumes to market as soon as completion operations conclude.

Outlook

The low natural gas price environment of 2012 had a significant effect on the Company”s natural gas revenues in 2012. Looking forward through 2013 and beyond, the Company is forecasting a steady gradual improvement in the natural gas price environment. With the Company”s growing condensate-rich Montney production combined with improved natural gas prices Delphi remains confident in achieving its long term growth targets.

The Company is taking a measured approach to its 2013 capital program with 2013 net capital expenditures estimated to be $50.0 – $55.0 million. Historically, Delphi executes a winter capital program in excess of first quarter cash flow followed by at least one quarter of minimal activity prior to returning to the field with an active fall program.

Delphi has hedged approximately 51 percent of its 2013 natural gas production at $3.27 per mcf to support funds from operations and the Company”s ability to pursue its planned capital program.

The Company”s recent success at East Bigstone has increased its current production capability to approximately 9,200 to 9,400 boe/d (28 percent NGL”s and light oil) with the final Montney horizontal well of the winter program not yet completed. Corporate production volumes for the first half of 2013 have been affected by two unscheduled outages in February and March related to the SemCams gathering system and the K3 processing plant and are anticipated to be affected again in May with a tentatively scheduled maintenance outage at the SemCams KA processing plant. The outages are partially offset by the Montney production performance significantly exceeding budget expectations. The Company will update its existing production guidance for the first half of 2013 as outage details are clarified and Montney well performance is evaluated over the next four to six weeks.

The recent results of the Montney program proves the robust economics of the play and with the large development inventory assembled, the Company is positioned with an asset capable of long term sustainable growth. The current field netbacks of the East Bigstone Montney production is estimated to be $28.00 – $30.00 per boe, more than twice the corporate field netback achieved in 2012.

In 2013 and beyond, we believe the Company will return to the low-cost reserve additions achieved over the previous three years with the major infrastructure build-out at East Bigstone in place and the production performance now being achieved. Our growing condensate and natural gas liquids production is providing a natural hedge against low natural gas prices.

On behalf of the Board of Directors and all the employees of Delphi, we would like to thank our shareholders for their continued support.

CONFERENCE CALL AND WEBCAST

A conference call and webcast to review 2012 results is scheduled for 9:00 a.m. Mountain Time (11:00 a.m. Eastern Time) on Thursday, March 21, 2013. The conference call number is 1-877-240-9772 or 416-340-8527. A brief presentation by David Reid, President and CEO and Brian Kohlhammer, Senior VP Finance & CFO, will be followed by a question and answer period. The conference call will also be broadcast live on the internet and may be accessed through the Delphi Energy website at www.delphienergy.ca

A taped rebroadcast will be available until 6:00 p.m. Mountain Time, Thursday, March 28, 2013. To access the rebroadcast, dial 1-800-408-3053 or 905-694-9451. The passcode is 6350938. Delphi”s annual and fourth quarter 2012 financial statements and management”s discussion and analysis are available on Delphi”s website at www.delphienergy.ca.

Delphi Energy is a Calgary-based company that explores, develops and produces oil and natural gas in Western Canada. The Company is managed by a proven technical team. Delphi trades on the Toronto Stock Exchange under the symbol DEE.

Forward-Looking Statements. This management discussion and analysis contains forward-looking statements and forward-looking information within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, may”, “will”, “should”, believe”, “intends”, “forecast”, “plans”, “guidance” and similar expressions are intended to identify forward-looking statements or information.

More particularly and without limitation, this management discussion and analysis contains forward looking statements and information relating to the Company”s risk management program, petroleum and natural gas production, future funds from operations, capital programs, commodity prices, costs and debt levels. The forward-looking statements and information are based on certain key expectations and assumptions made by Delphi, including expectations and assumptions relating to prevailing commodity prices and exchange rates, applicable royalty rates and tax laws, future well production rates, the performance of existing wells, the success of drilling new wells, the capital availability to undertake planned activities and the availability and cost of labour and services.

Although the Company believes that the expectations reflected in such forward-looking statements and information are reasonable, it can give no assurance that such expectations will prove to be correct. Since forward-looking statements and information address future events and conditions, by their very nature they involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated due to a number of factors and risks. These include, but are not limited to, the risks associated with the oil and gas industry in general such as operational risks in development, exploration and production, delays or changes in plans with respect to exploration or development projects or capital expenditures, the uncertainty of estimates and projections relating to production rates, costs and expenses, commodity price and exchange rate fluctuations, marketing and transportation, environmental risks, competition, the ability to access sufficient capital from internal and external sources and changes in tax, royalty and environmental legislation. Additional information on these and other factors that could affect the Company”s operations or financial results are included in reports on file with the applicable securities regulatory authorities and may be accessed through the SEDAR website (www.sedar.com). The forward-looking statements and information contained in this press release are made as of the date hereof for the purpose of providing the readers with the Company”s expectations for the coming year. The forward-looking statements and information may not be appropriate for other purposes. Delphi undertakes no obligation to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Basis of Presentation. For the purpose of reporting production information, reserves and calculating unit prices and costs, natural gas volumes have been converted to a barrel of oil equivalent (boe) using six thousand cubic feet equal to one barrel. A boe conversion ratio of 6:1 is based upon an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. This conversion conforms with the Canadian Securities Administrators” National Instrument 51-101 when boes are disclosed. Boes may be misleading, particularly if used in isolation.

Non-GAAP Measures. The MD&A contains the terms “funds from operations”, “funds from operations per share”, “net debt” and “netbacks” which are not recognized measures under Canadian generally accepted accounting principles. The Company uses these measures to help evaluate its performance. Management considers netbacks an important measure as it demonstrates its profitability relative to current commodity prices. Management uses funds from operations to analyze performance and considers it a key measure as it demonstrates the Company”s ability to generate the cash necessary to fund future capital investments and to repay debt. Funds from operations is a non-GAAP measure and has been defined by the Company as net earnings plus the addback of non-cash items (depletion, depreciation and accretion, stock-based compensation, future income taxes and unrealized gain/(loss) on risk management activities) and excludes the change in non-cash working capital related to operating activities and expenditures on asset retirement obligations and reclamation. The Company also presents funds from operations per share whereby amounts per share are calculated using weighted average shares outstanding consistent with the calculation of earnings per share. Delphi”s determination of funds from operations may not be comparable to that reported by other companies nor should it be viewed as an alternative to cash flow from operating activities, net earnings or other measures of financial performance calculated in accordance with Canadian GAAP. The Company has defined net debt as the sum of long term debt plus working capital excluding the current portion of future income taxes and risk management asset/liability. Net debt is used by management to monitor remaining availability under its credit facilities. Operating netbacks have been defined as revenue less royalties, transportation and operating costs. Cash flow netbacks have been defined as operating netbacks less interest and general and administrative costs. Netbacks are generally discussed and presented on a per boe basis.

For the calculation of finding and development cost and recycle ratio, refer to the Company”s press release of crude oil and natural gas reserves information dated February 29, 2012.

Delphi Energy Corp.

David J. Reid

President & CEO

(403) 265-6171

Delphi Energy Corp.

Brian P. Kohlhammer

Senior V.P. Finance & CFO

(403) 265-6171

(403) 265-6207

Delphi Energy Corp.

300, 500 – 4 Avenue S.W.

Calgary, Alberta

T2P 2V6

info@delphienergy.ca

www.delphienergy.ca

{kind=link}