CALGARY, ALBERTA–(Marketwired – May 31, 2013) – Diaz Resources Ltd. (TSX VENTURE:DZR) (“Diaz” or the “Company”) announces that it has filed its interim Financial Statements and MD&A for the three months ended March 31, 2013 on SEDAR.

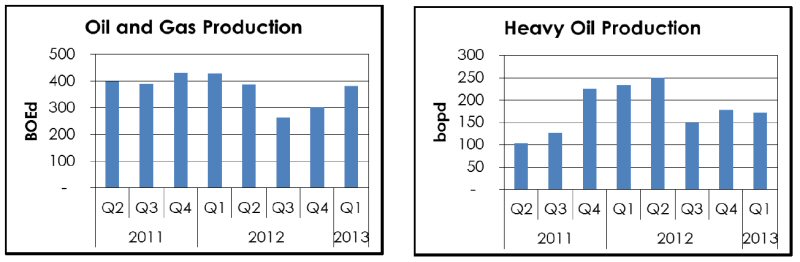

During the quarter, Diaz’s production increased to 382 BOEd from 302 BOEd in Q4 2012 due to the Company’s shut-in shallow natural gas wells being placed back on production. The Company did not participate in drilling any new wells during the quarter due to a lack of working capital to finance new development and the operator of the Macklin field did not propose any new wells as a result of lower heavy oil prices.

It is anticipated that further heavy oil development drilling at Macklin will be planned for the third quarter of 2013. A thorough review of the Company’s ability to raise additional capital or other financing methods to participate in this drilling resulted in few viable choices. Negative issues included: poor capital markets for junior energy companies in Canada, no ability to increase debt capacity, a poor environment for selling producing properties on acceptable terms, and a negative market in which to make farm-out deals on favorable terms. As a result of the foregoing, Management believes that the proposed merger with Tuscany Energy Ltd. described below is the most favorable route to preserve Diaz’s shareholders’ equity and allow the Diaz shareholder’s to benefit from ownership in a larger, more active entity.

Proposed Merger With Tuscany Energy Ltd.

On May 17, 2013, Tuscany Energy Ltd. (“Tuscany”) and Diaz announced that they had entered into an agreement whereby, subject to certain conditions including obtaining shareholder, court and all necessary regulatory approvals, Tuscany will acquire all of the common shares of Diaz (the “Transaction”). After the acquisition of Diaz, Tuscany plans to reorganize its capital structure by the consolidation of its shares on the basis of 1 new share for every 8 shares outstanding.

It is anticipated that Tuscany will issue 0.31 common shares for each outstanding Diaz common share. Following the Diaz acquisition it is expected that Tuscany, on a proforma basis, will have:

The above reserve information and net present value is based on the independent reserves reports of Diaz and Tuscany prepared by McDaniel & Associates Consultants effective December 31, 2012 in accordance with National Instrument 51-101 and the COGE Handbook. It should not be assumed that the estimate of the net present value of the future net revenue attributable to Diaz’s and Tuscany’s reserves represents the fair market value of the reserves. There can be no assurances that the assumptions contained in such estimate will be attained and variances could be material.

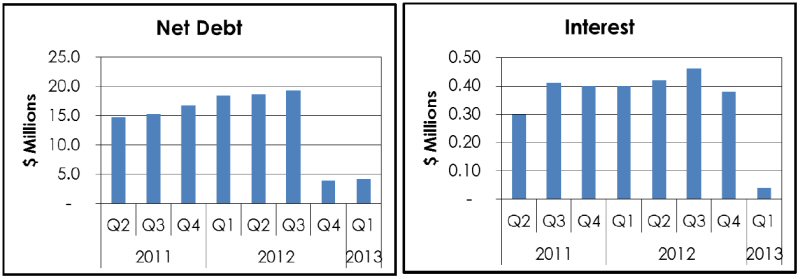

In accordance with the proposed Transaction Tuscany will effectively assume Diaz’s net debt, approximately $4.2 million at March 31, 2013.

Tuscany and Diaz have operated together through a joint operating agreement since 2010 and therefore they have common working interests in some heavy oil properties, including the Macklin pool, one of the properties that is expected to be a focus of the combined Tuscany’s 2013 development operations.

Tuscany anticipates that the acquisition will result in reduced overhead expenses per BOE and increase management’s efficiency and control over the timing of drilling operations.

The Transaction is expected to be completed by way of a Plan of Arrangement and closing is expected to occur by the end of July 2013, subject to satisfaction of certain conditions including standard stock exchange, court and regulatory approvals and the requisite two-thirds majority and majority of minority approval of Diaz’s shareholders and majority of minority approval of Tuscany’s shareholders. An information circular, prepared jointly by the parties, will be mailed to shareholders of both Tuscany and Diaz in connection with the shareholder meetings of each company expected to be held on July 15, 2013 to consider and approve the Transaction.

Operations

In response to strengthening natural gas prices since the beginning of the year, Diaz focused during the quarter on re-activating its shut-in natural gas properties. As a result, production volumes during the quarter rose to 382 BOEd compared with 302 BOEd in Q4 2012.

For the quarter, production revenues totaled $1.1 million, a decrease from $1.7 million in Q1 2012, resulting primarily from lower heavy oil prices. These lower prices also reduced cash flow from $362,000 to $23,000.

Fixed asset additions for the quarter were reduced to $287,000 from $1.8 million in the comparative quarter.

To view the charts associated with this press release, please visit the following link: http://media3.marketwire.com/docs/diaz_graph1.jpg

At quarter end, the Company had drawn $3.7 million of a $3.9 million bank line; however, net debt was $4.2 million, compared with $18.4 million at the end of Q1 2012. Interest costs were greatly reduced to $43,000 from $404,000 in Q1 2012.

To view the charts associated with this press release, please visit the following link: http://media3.marketwire.com/docs/diaz_graph2.jpg

Production

For the three months ended March 31, 2013, the Company’s average production increased to 382 BOEd from 302 BOEd in Q4 2012 but decreased compared with 427 BOEd in Q1 2012. The Company has increased its oil and gas production for the last two quarters as operational enhancements maintained heavy oil production and as shut-in natural gas wells were brought back into production.

Outlook

Management believes the decision to proceed with the Transaction between Tuscany and Diaz is the best available alternative to the Company as continued development drilling by Diaz has been stalled by lack of available funds. The acquisition by Tuscany of Diaz’s common shares is expected to facilitate the development of Diaz’s and Tuscany’s asset base at Macklin as Tuscany has the financial capability to develop those assets. Management believes this should result in increased value for the shareholders.

Diaz is an oil and gas exploration and production company based in Calgary, Alberta. Diaz’s current focus is on oil development and exploration in Alberta and Saskatchewan.

ADVISORY: Certain information in this news release, including the proposed Transaction with Tuscany, drilling plans and projected drilling, completion and equipping costs, and production rates from the Lloydminster and Macklin fields may constitute forward-looking statements under applicable securities laws and necessarily involve risks including, without limitation, risks associated with oil and gas exploration, development, exploitation, production, marketing and transportation, loss of markets, volatility of commodity prices, currency fluctuations, environmental risks, competition from other producers, inability to retain drilling rigs and other services, capital expenditure costs, including drilling, completion and facilities costs, delays resulting from or inability to obtain required regulatory approvals and ability to access sufficient capital from internal and external sources. As a consequence, actual results may differ materially from those anticipated in the forward-looking statements. Readers are cautioned that the foregoing list of factors is not exhaustive.

Where amounts are expressed on a barrel of oil equivalent (boe) basis, natural gas volumes have been converted to barrels of oil at six thousand cubic feet (mcf) per barrel (bbl). Boe figures may be misleading, particularly if used in isolation. A boe conversion of six thousand cubic feet per barrel is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. References to oil in this discussion include crude oil and natural gas liquids (NGLs).

The forward looking statements contained in this press release are made as of the date hereof and Diaz undertakes no obligations to update publicly or revise any forward looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THIS RELEASE.

DIAZ RESOURCES LTD.

Robert W. Lamond

Chairman & CEO

(403) 269-9889

(403) 269-9890 (FAX)

DIAZ RESOURCES LTD.

Donald K. Clark

Vice President Operations & COO

(403) 269-9889

(403) 269-9890 (FAX)

{kind=link}

{kind=link}