CALGARY, ALBERTA–(Marketwired – Feb. 6, 2014) – Baytex Energy Corp. (“Baytex”, the “Company” or “we”) (TSX:BTE)(NYSE:BTE) and Aurora Oil & Gas Limited (“Aurora”) (TSX:AEF)(ASX:AUT) today announced they have entered into an agreement whereby Baytex will acquire, through a scheme of arrangement under Australian law (the “Arrangement”), 100% of the shares of Aurora, on a fully diluted basis, for AU$4.10 (Australian dollars) cash per share (the “Acquisition”). The total consideration to be paid by Baytex is approximately $1.8 billion, plus assumed debt of approximately $744 million for a total transaction value of approximately $2.6 billion. All amounts are in Canadian dollars unless otherwise noted.

Commenting on the Acquisition, James Bowzer, President and Chief Executive Officer of Baytex, said, “Baytex will acquire premier acreage in the core of the Eagle Ford, one of the leading shale oil plays in the U.S. The Acquisition is an excellent fit with our existing business model and positions Baytex in another world-class oil resource play. The Acquisition will provide our shareholders with exposure to low-risk, repeatable, high-return projects with leading capital efficiencies.”

“This is a highly accretive transaction on a per share basis to reserves, production, and funds from operations,” said Bowzer. “The Eagle Ford play provides not only exposure to light oil, but also to Gulf Coast crude oil markets with established transportation systems. A portion of the produced crude oil benefits from Louisiana Light Sweet based pricing, which currently trades at a premium to WTI.”

At Baytex, we are committed to a growth-and-income model and its three fundamental principles: delivering organic production growth, paying a meaningful dividend and maintaining capital discipline. Through the combination of an expanded inventory of high capital efficiency projects and an improved outlook for heavy oil differentials, we remain confident in our business plan going forward. Consequently, Baytex has committed to increase the monthly dividend on its common shares by 9% to $0.24 from $0.22 per share, subject to the completion of the Acquisition. Based on the anticipated closing date of mid/late May 2014, the dividend increase is expected to take effect for the dividend payable on or about July 15, 2014.

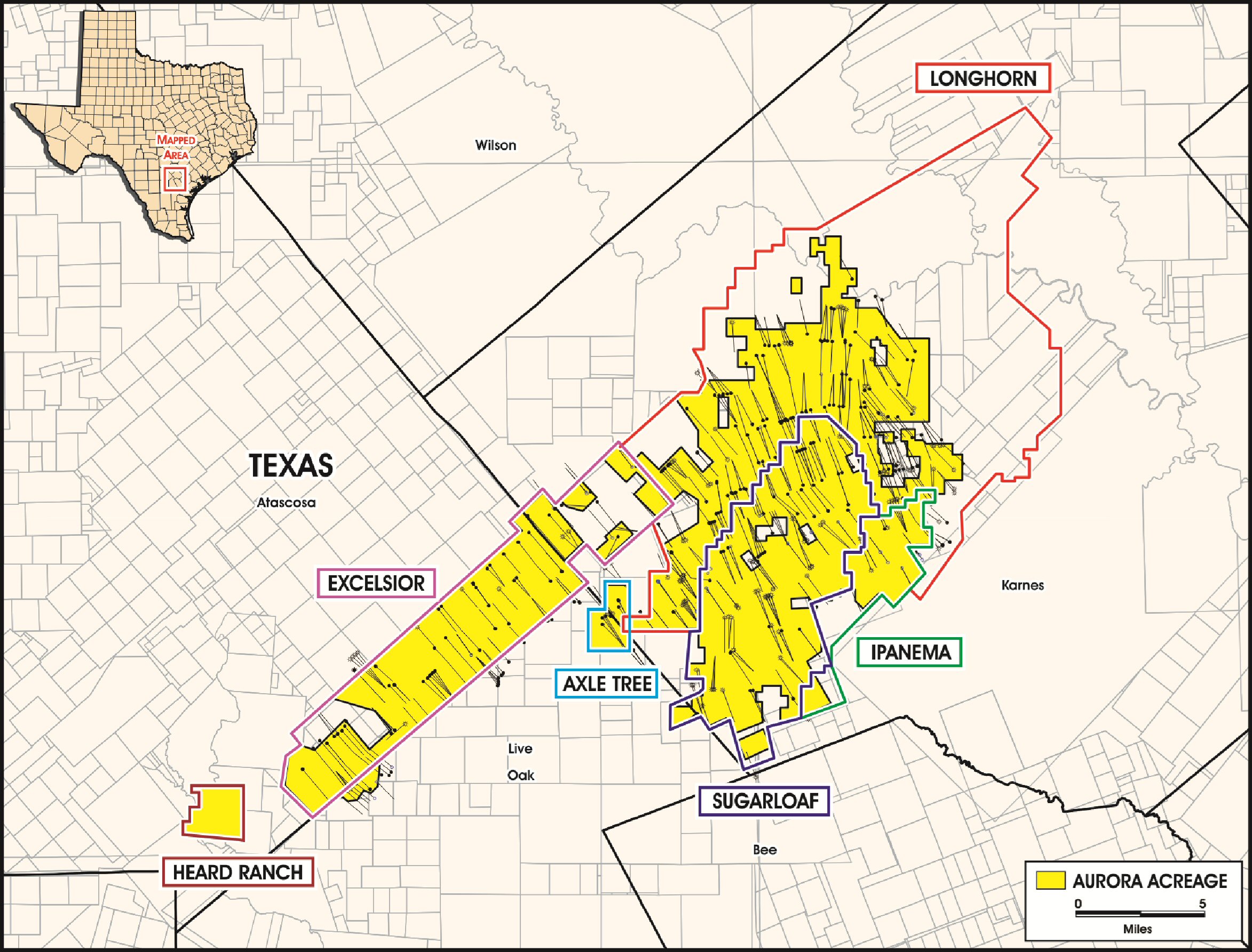

Aurora’s primary asset is 22,200 net contiguous acres in the prolific Sugarkane Field located in South Texas in the core of the liquids-rich Eagle Ford shale. Aurora’s Q4/2013 gross production was 24,678 boe/d (82% liquids) of predominantly light, high-quality crude oil. The Sugarkane Field has been largely delineated with infrastructure in place which is expected to facilitate low-risk future annual production growth. In addition, these assets have significant future reserves upside potential from well downspacing, improving completion techniques and new development targets in additional zones.

In conjunction with the Acquisition, Baytex has entered into a $1.3 billion bought deal subscription receipt financing (the “Equity Financing”) with a syndicate of underwriters co-led by Scotiabank and RBC Capital Markets, which is described in further detail below. The Equity Financing is subject to customary closing conditions including receipt of applicable regulatory approvals and is expected to close on or about February 24, 2014.

Strategic Rationale

The Acquisition enhances Baytex’s growth-and-income business model, delivers production and reserves per share growth and provides attractive capital efficiencies for future investment. The Acquisition is accretive to Baytex’s funds from operations while maintaining a strong balance sheet.

Notes:

| (1) | Reserves and reserve accretion based on Baytex reserves as at December 31, 2012 prepared by Sproule Associates Limited and Baytex’s internal estimate of Aurora reserves as at December 31, 2013, and prepared by a non-independent qualified reserve evaluator in accordance with National Instrument 51-101 (“NI 51-101”) and the Canadian Oil and Gas Evaluation Handbook (the “COGE Handbook”). Based on gross reserves. |

| (2) | Production and production per share accretion (boe/d per thousand shares) based on: (i) Aurora’s 2014 estimated gross production of 30,500 boe/d; (ii) Baytex’s 2014 estimated gross production of 61,000 boe/d; and (iii) Baytex’s weighted average common shares outstanding for 2014 of 127 million (before giving effect to the Equity Financing) and 162 million (after giving effect to the Equity Financing and prior to the over-allotment option). |

| (3) | Funds from operations accretion based on commodity prices of US$90/bbl for oil, US$4.00/Mcf for natural gas and US$27/bbl for NGLs. Baytex estimate based on expected 2014 gross production of 61,000 boe/d. Pro forma estimate based on 2014 gross production of 88,000 to 90,000 boe/d and as adjusted for the Equity Financing, estimated transaction costs, and incremental interest expense associated with the anticipated debt required to close. |

Key Attributes of Aurora

With the Acquisition, Baytex obtains a premier position in the high-value area of the core of the liquids-rich Eagle Ford resource play. These assets provide material production, long-term growth and high quality reserves with upside potential. This entry provides Baytex with a platform for further potential growth opportunities.

To view a map of the acquired Eagle Ford properties, please visit the following link:

http://media3.marketwire.com/docs/maplink02-06-2014.jpg.

Terms of the Arrangement

The Arrangement has been unanimously approved by the board of directors of Baytex. The board of directors of Aurora intends to recommend that Aurora shareholders vote in favour of the Arrangement, in the absence of a superior proposal and subject to an independent expert’s report concluding that the Arrangement is in the best interests of Aurora shareholders and that they intend to vote in favor of the Arrangement the Aurora shares controlled by them, which amount to approximately 5.5% of the issued and outstanding Aurora shares.

The Arrangement must be approved by the Aurora shareholders at a special meeting of shareholders expected to be held in late April/early May 2014. The Arrangement must be approved by (i) at least 75% of the votes cast and (ii) by a majority in number of the Aurora shareholders who cast votes.

The Arrangement is subject to certain customary conditions, including approval by the Australian court, the Australian Foreign Investment Review Board and under the U.S. Hart-Scott-Rodino Anti-Trust Improvements Act.

The disclosure booklet that will be prepared in connection with the special meeting of Aurora shareholders is expected to be mailed to shareholders in late March/early April 2014. The Acquisition is expected to close in mid/late May 2014. The Implementation Agreement will be filed by Baytex on SEDAR at www.sedar.com and EDGAR at www.sec.gov.

Financing of the Transaction

Baytex is financing the Acquisition through a combination of the Equity Financing ($1.3 billion bought-deal equity offering) and draws on its revolving and term credit facilities. Concurrent with the Acquisition, Baytex will increase its revolving credit facilities from $850 million to $1.0 billion and will add a $200 million term loan. Undrawn credit facilities on closing will be $400 to $600 million leaving significant available liquidity to continue to execute our ongoing business plans. It is expected that Baytex will put in place a US$300 million borrowing base facility at Aurora (or a subsidiary thereof) with a syndicate of banks concurrent with the closing of the Acquisition.

In connection with the Acquisition, Baytex has entered into an agreement, on a “bought-deal” basis, with a syndicate of underwriters (the “Underwriters”) co-led by Scotiabank and RBC Capital Markets and including CIBC World Markets Inc., TD Securities Inc., BMO Capital Markets and National Bank Financial Inc., for an offering of 33,420,000 subscription receipts (“Subscription Receipts”) at a price of $38.90 per Subscription Receipt with each Subscription Receipt entitling the holder thereof to receive, on closing of the Acquisition, one common share of the Company (“Common Share”) for aggregate gross proceeds of approximately $1.3 billion. The Company has granted the Underwriters an over-allotment option to purchase, on the same terms, up to an additional 5,013,000 Subscription Receipts. This option is exercisable by the Underwriters, in whole or in part, at any time for a period of 30 days following closing. The maximum gross proceeds raised under the Equity Financing will be approximately $1.5 billion should the over-allotment option be exercised in full. The Equity Financing is subject to customary closing conditions including receipt of applicable regulatory approvals and is expected to close on or about February 24, 2014.

The gross proceeds from the sale of Subscription Receipts will be held in escrow and will be released upon satisfaction of certain conditions to enable us to convert the funds to Australian dollars and complete the Acquisition. Upon closing of the Acquisition, the holders of the Subscription Receipts will be entitled to receive an amount per Subscription Receipt equal to dividends declared per common share that accrue from the date of closing of the financing to the date of closing of the Acquisition. In the event the Acquisition fails to close on or prior to June 30, 2014, the agreement for the Acquisition is terminated in accordance with its terms at any earlier time, or we have advised the Underwriters or announced to the public that we do not intend to proceed with the Acquisition, the purchase price plus each holder’s proportionate share of interest earned on funds held in escrow, net of any applicable withholding taxes, will be returned to each holder of Subscription Receipts.

The Equity Financing will be completed under the multi-jurisdictional disclosure system by way of short form prospectus filed with the securities regulatory authorities in each of the provinces of Canada and with the Securities and Exchange Commission in the United States.

2014 Guidance

Following closing of the Acquisition, Baytex will provide revised guidance for full-year 2014. The guidance will include a full update incorporating the Acquisition, Equity Financing, and any modifications to Baytex’s current asset plans.

Financial and Legal Advisors

Scotia Waterous acted as exclusive financial advisor to Baytex and Scotiabank provided bank financing in connection with the Acquisition. Baytex’s legal advisors are Burnet, Duckworth & Palmer LLP in Canada, Paul, Weiss, Rifkind, Wharton & Garrison LLP in the U.S. and Norton Rose Fulbright in Australia and the U.S.

| Conference Call Today

4:45 p.m. EST (2:45 p.m. MST) |

| A conference call will be held today, February 6, 2014, starting at 4:45pm EST (2:45pm MST). Please connect approximately 15 minutes prior to the beginning of the call to ensure participation. To participate, please dial 1-416-340-8527 or toll free in North America 1-800-565-0813 and toll free international 1-800-2787-2090. Alternatively, to listen to the conference call online, please enter http://www.gowebcasting.com/5253 in your web browser.

An investor presentation related to the Acquisition will be available shortly on our website at www.baytexenergy.com. |

[expand title=”Advisories & Contact”]Advisory Regarding Forward-Looking Statements

In the interest of providing shareholders and potential investors with information regarding Baytex and Aurora, including management’s assessment of future plans and operations, certain statements in this press release are “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of applicable Canadian securities legislation (collectively, “forward-looking statements”). In some cases, forward-looking statements can be identified by terminology such as “anticipate”, “believe”, “continue”, “could”, “estimate”, “expect”, “forecast”, “intend”, “may”, “objective”, “ongoing”, “outlook”, “potential”, “project”, “plan”, “should”, “target”, “would”, “will” or similar words suggesting future outcomes, events or performance. The forward-looking statements contained in this press release speak only as of the date thereof and are expressly qualified by this cautionary statement.

Specifically, this press release contains forward-looking statements relating to but not limited to: Baytex‘s plans to increase the dividend on its common shares upon completion of the Acquisition; the anticipated benefits from the Acquisition, including our beliefs that the Acquisition will be an excellent fit with our business model and will provide shareholders with exposure to low-risk, repeatable, high-return projects with capital efficiencies; our expectations that the Aurora assets have infrastructure in place that support low-risk future annual production and that such assets will provide material production, long-term growth and high quality reserves with upside potential; our expectations regarding the effect of well downspacing, improving completion techniques and new development targets on the reserves potential of the Aurora assets; anticipated effect of the Acquisition on Baytex, including our business model and our reserves, production and funds from operations; forecasted production and production mix following completion of the Acquisition; Aurora’s forecasted production and production growth for 2014; drilling plans; operating and financial metrics and the strategic rationale for the Acquisition; expectations regarding the Acquisition and the Equity Financing, including anticipated timing of mailing of the scheme booklet to Aurora shareholders; timing of completion of the Acquisition and the Equity Financing, and approvals required for the Arrangement and Equity Financing; the terms of the Subscription Receipts; the terms of the increase to our revolving credit facilities and the term loan and our expectations regarding the implementation of a borrowing base facility for Aurora following closing of the Acquisition; and payment of the purchase price, including the use of proceeds from the Equity Financing and our plans to draw on the revolving credit facilities and the term loan. In addition, information and statements relating to reserves are deemed to be forward-looking statements, as they involve implied assessment, based on certain estimates and assumptions, that the reserves described exist in quantities predicted or estimated, and that the reserves can be profitably produced in the future. Cash dividends on our common shares are paid at the discretion of our Board of Directors and can fluctuate. In establishing the level of cash dividends, the Board of Directors considers all factors that it deems relevant, including, without limitation, the outlook for commodity prices, our operational execution, the amount of funds from operations and capital expenditures and our prevailing financial circumstances at the time.

These forward-looking statements are based on certain key assumptions regarding, among other things: the receipt of regulatory, shareholder and other approvals for the Arrangement; our ability to execute and realize on the anticipated benefits of the Acquisition; timing of closing and receipt of regulatory approvals for the Equity Financing; petroleum and natural gas prices and pricing differentials between light, medium and heavy gravity crude oil; well production rates and reserve volumes; our ability to add production and reserves through our exploration and development activities; capital expenditure levels; the availability and cost of labour and other industry services; the amount of future cash dividends that we intend to pay; interest and foreign exchange rates; the continuance of existing and, in certain circumstances, proposed tax and royalty regimes; our ability to develop our crude oil and natural gas properties and the acquired assets in the manner currently contemplated; current or, where applicable, proposed assumed industry conditions, laws and regulations will continue in effect or as anticipated; and the estimates of our production and reserve volumes and Aurora’s production and reserve volumes and the assumptions related thereto (including commodity prices and development costs) are accurate in all material respects. Readers are cautioned that such assumptions, although considered reasonable by Baytex at the time of preparation, may prove to be incorrect.

Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Such factors include, but are not limited to: the Acquisition may not be completed on the terms contemplated or at all; failure to realize the anticipated benefits of the Acquisition; closing of the Equity Offering and/or the Acquisition could be delayed or not completed if we are not able to obtain the necessary stock exchange, shareholder and regulatory approvals or any other approvals required for completion or, unless waived, some other condition to closing is not satisfied; failure to put in place a borrowing base facility for Aurora following completion of the Acquisition; declines in oil and natural gas prices; risks related to the accessibility, availability, proximity and capacity of gathering, processing and pipeline systems; variations in interest rates and foreign exchange rates; risks associated with our hedging activities; uncertainties in the credit markets may restrict the availability of credit or increase the cost of borrowing; refinancing risk for existing debt and debt service costs; access to external sources of capital; third party credit risk; a downgrade of our credit ratings; risks associated with the exploitation of our properties and our ability to acquire reserves; increases in operating costs;

changes in government regulations that affect the oil and gas industry; changes to royalty or mineral/severance tax regimes; risks relating to hydraulic fracturing; changes in income tax or other laws or government incentive programs; uncertainties associated with estimating petroleum and natural gas reserves; risks associated with acquiring, developing and exploring for oil and natural gas and other aspects of our operations; risks associated with properties operated by third parties; risks associated with delays in business operations; risks associated with the marketing of our petroleum and natural gas production; risks associated with large projects or expansion of our activities; risks related to heavy oil projects; expansion of our operations; the failure to realize anticipated benefits of acquisitions and dispositions or to manage growth; changes in environmental, health and safety regulations; the implementation of strategies for reducing greenhouse gases; competition in the oil and gas industry for, among other things, acquisitions of reserves, undeveloped lands, skilled personnel and drilling and related equipment; the activities of our operating entities and their key personnel and information systems; depletion of our reserves; risks associated with securing and maintaining title to our properties; seasonal weather patterns; our permitted investments; access to technological advances; changes in the demand for oil and natural gas products; involvement in legal, regulatory and tax proceedings; the failure of third parties to comply with confidentiality agreements; risks associated with the ownership of our securities, including the discretionary nature of dividend payments and changes in market-based factors; risks for United States and other non-resident shareholders, including the ability to enforce civil remedies, differing practices for reporting reserves and production, additional taxation applicable to non-residents and foreign exchange risk; and other factors, many of which are beyond the control of Baytex. These risk factors are discussed in our Annual Information Form, Annual Report on Form 40-F and Management’s Discussion and Analysis for the year ended December 31, 2012, as filed with Canadian securities regulatory authorities and the U.S. Securities and Exchange Commission.

The above summary of assumptions and risks related to forward looking information in this press release has been provided in order to provide shareholders and potential investors with a more complete perspective on Baytex and Aurora‘s current and Baytex‘s future operations if the Acquisition is completed and such information may not be appropriate for other purposes. There is no representation by Baytex that actual results achieved during the forecast period will be the same in whole or in part as those forecast and Baytex does not undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities law.

Oil and Gas Advisory

All of the reserves information contained in this press release have been calculated and reported using assumptions and methodology guidelines outlined in accordance with the standards contained in the COGE Handbook, NI 51-101 and the reserve definitions contained in the Canadian Securities Administrators Staff Notice 51-324. The SEC definitions of proved, probable and possible reserves are different than NI 51-101; therefore, proved, probable and possible reserves disclosed herein may not be comparable to United States standards.

References herein to 30 day initial production rates and other short-term production rates are useful in confirming the presence of hydrocarbons, however such rates are not determinative of the rates at which such wells will commence production and decline thereafter and are not indicative of long term performance or of ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating aggregate production for us or the acquired assets. A pressure transient analysis or well-test interpretation has not been carried out in respect of all wells. Accordingly, we caution that the test results should be considered to be preliminary.

The term “boe” means a barrel of oil equivalent on the basis of 6 Mcf of natural gas to 1 Bbl of oil. Boe’s may be misleading, particularly if used in isolation. A boe conversation ratio of 6 Mcf: 1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6 Mcf: 1Bbl, utilizing a conversion ratio at 6 Mcf: 1 Bbl may be misleading as an indication of value.

Financial Measures

We disclose in this press release several financial measures that do not have any standardized meaning prescribed under International Financial Reporting Standards (“IFRS“). These financial measures include funds from operations. Management believes that these financial measures are useful supplemental information to analyze operating performance and provide an indication of the anticipated metrics and benefits of the Acquisition. Investors should be cautioned that these measures should not be construed as an alternative to net income, cash provided by operating activities or other measures of financial performance as determined in accordance with IFRS. Our method of calculating these measures may differ from other companies, and accordingly, they may not be comparable to similar measures used by other companies.

Funds from operations is not a measurement based on GAAP in Canada, but is a financial term commonly used in the oil and gas industry. Funds from operations represents cash generated from operating activities adjusted for financing costs, changes in non-cash operating working capital and other operating items. Baytex’s determination of funds from operations may not be comparable with the calculation of similar measures for other entities. Baytex considers funds from operations a key measure of performance as it demonstrates its ability to generate the cash flow necessary to fund future dividends to shareholders and capital investments. The most directly comparable measures calculated in accordance with GAAP are cash flow from operating activities and net income.

All amounts are in Canadian dollars unless otherwise noted.

This news release does not constitute an offer to sell securities, nor is it a solicitation of an offer to buy securities, in any jurisdiction. Any sales will be made through registered securities dealers in jurisdictions where the offering has been qualified for distribution.

Baytex Energy Corp.

Baytex Energy Corp. is a dividend-paying oil and gas corporation based in Calgary, Alberta. The company is engaged in the acquisition, development and production of crude oil and natural gas in the Western Canadian Sedimentary Basin and in the Williston Basin in the United States. Approximately 89% of Baytex’s production is weighted toward crude oil. Baytex pays a monthly dividend on its common shares which are traded on the Toronto Stock Exchange and the New York Stock Exchange under the symbol BTE.

For further information about Baytex, please visit our website at www.baytexenergy.com.

Baytex Energy Corp.

Brian Ector

Vice President, Investor Relations

Toll Free Number: 1-800-524-5521

investor@baytexenergy.com

www.baytexenergy.com

[/expand]

{kind=link}