CALGARY, ALBERTA–(Marketwired – April 30, 2014) – Canadian Oil Sands Limited (TSX:COS)(OTCQX:COSWF) –

All financial figures are unaudited and in Canadian dollars unless otherwise noted.

“Higher production and crude oil prices contributed to a 30 per cent increase in cash flow from operations in the first quarter of 2014 compared with last year’s first quarter,” said Ryan Kubik, President and Chief Executive Officer. “Syncrude has also made significant progress on our major projects. Our Mildred Lake Mine Train Replacement project reached 85 per cent completion and our estimated cost has come down by $300 million gross to Syncrude. The project is well on track to be in service by the end of the year.”

Highlights for the three months ended March 31, 2014:

| Highlights | ||||||

| Three Months Ended March 31 | ||||||

| 2014 | 2013 | |||||

| Cash flow from operations1 ($ millions) | $ | 357 | $ | 275 | ||

| Per Share1 ($/Share) | $ | 0.74 | $ | 0.57 | ||

| Net income ($ millions) | $ | 172 | $ | 177 | ||

| Per Share, Basic and Diluted ($/Share) | $ | 0.35 | $ | 0.37 | ||

| Sales volumes2 | ||||||

| Total (mmbbls) | 9.5 | 8.6 | ||||

| Daily average (bbls) | 105,283 | 95,683 | ||||

| Realized SCO selling price ($/bbl) | $ | 105.73 | $ | 96.11 | ||

| West Texas Intermediate (“WTI”) (average $US/bbl) | $ | 98.61 | $ | 94.36 | ||

| SCO premium (discount) to WTI (weighted average $/bbl) | $ | (2.93 | ) | $ | 1.00 | |

| Average foreign exchange rate ($US/$Cdn) | $ | 0.91 | $ | 0.99 | ||

| Operating expenses ($ millions) | $ | 445 | $ | 355 | ||

| Per barrel ($/bbl) | $ | 46.91 | $ | 41.20 | ||

| Capital expenditures ($ millions) | $ | 217 | $ | 268 | ||

| Dividends ($ millions) | $ | 170 | $ | 170 | ||

| Per Share ($/Share) | $ | 0.35 | $ | 0.35 | ||

| 1 Cash flow from operations and cash flow from operations per Share are additional GAAP financial measures and are defined in the “Additional GAAP Financial Measures” section of our Management’s Discussion and Analysis (“MD&A”). | ||||||

| 2 The Corporation’s sales volumes differ from its production volumes due to changes in inventory, which are primarily in-transit pipeline volumes. Sales volumes are net of purchases. | ||||||

2014 Outlook

Canadian Oil Sands provides the following key estimates and assumptions for 2014:

More information on the outlook is provided in our MD&A and the April 30, 2014 guidance document, which is available on our web site at www.cdnoilsands.com under “Investor Centre”.

The 2014 Outlook contains forward-looking information and users are cautioned that the actual amounts may vary from the estimates disclosed. Please refer to the “Forward-Looking Information Advisory” in the MD&A section of this report for the risks and assumptions underlying this forward-looking information.

Annual General Meeting

COS will hold its Annual General Meeting of Shareholders today, April 30, 2014 at 2:30 p.m. (MDT) in the Ballroom of the Metropolitan Conference Centre, located at 333 Fourth Avenue SW, Calgary, Alberta. A live audio webcast of the meeting can be accessed on COS’ website at www.cdnoilsands.com. An archived version of the webcast and presentation material will be available shortly after the meeting from the website and archived for 90 days.

Management’s Discussion and Analysis

The following Management’s Discussion and Analysis (“MD&A”) was prepared as of April 30, 2014 and should be read in conjunction with the unaudited consolidated financial statements and notes thereto of Canadian Oil Sands Limited (the “Corporation”) for the three months ended March 31, 2014 and March 31, 2013, the audited consolidated financial statements and MD&A of the Corporation for the year ended December 31, 2013 and the Corporation’s Annual Information Form (“AIF”) dated February 20, 2014. Additional information on the Corporation, including its AIF, is available on SEDAR at www.sedar.com or on the Corporation’s website at www.cdnoilsands.com. References to “Canadian Oil Sands”, “COS” or “we” include the Corporation, its subsidiaries and partnerships. The financial results of Canadian Oil Sands have been prepared in accordance with Canadian Generally Accepted Accounting Principles (“GAAP”) and are reported in Canadian dollars, unless otherwise noted.

Table of Contents

Advisories

Forward Looking Information

In the interest of providing the Corporation’s shareholders and potential investors with information regarding the Corporation, including management’s assessment of the Corporation’s future production and cost estimates, plans and operations, certain statements throughout this MD&A and the related press release contain “forward-looking information” under applicable securities law. Forward-looking statements are typically identified by words such as “anticipate”, “expect”, “believe”, “plan”, “intend” or similar words suggesting future outcomes.

Forward-looking statements in this MD&A and the related press release include, but are not limited to, statements with respect to: the expectations regarding the 2014 annual Syncrude forecasted production range of 95 million barrels to 105 million barrels and the single-point Syncrude production estimate of 100 million barrels (36.7 million barrels net to the Corporation); the timing and duration of the Coker 8-1 maintenance; the timing and duration of the Coker 8-2 turnaround; the intention to fund the Syncrude major projects primarily with cash flow from operations and existing cash balances; the establishment of future dividend levels with the intent of absorbing short-term market volatility over several quarters; the expected sales, operating expenses, purchased energy costs, development expenses, Crown royalties, capital expenditures and cash flow from operations for 2014; the plan to use existing cash balances to fund capital expenditures and dividends; the anticipated amount of current taxes in 2014; expectations regarding the Corporation’s cash levels for 2014; the expected price for crude oil and natural gas in 2014; the expected foreign exchange rates in 2014; the expected realized selling price, which includes the anticipated differential to West Texas Intermediate (“WTI”) to be received in 2014 for the Corporation’s product; the expectations regarding net debt; the anticipated impact of increases or decreases in oil prices, production, operating expenses, foreign exchange rates and natural gas prices on the Corporation’s cash flow from operations; the belief that fluctuations in the Corporation’s realized selling prices, U.S. to Canadian dollar exchange rate fluctuations and planned and unplanned maintenance activities may impact the Corporation’s financial results in the future; the belief that capital expenditures and capital deductions for Crown royalties will decline after 2014 in connection with the substantial completion of the major projects; the expected amount of total major project costs, anticipated target in-service dates and estimated completion percentages for the Mildred Lake mine train replacements and the centrifuge plant at the Mildred Lake mine; the cost estimates for 2014 and 2015 major project spending; and the estimate that regular maintenance capital costs for the next few years should be similar to 2014.

You are cautioned not to place undue reliance on forward-looking statements, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. By their nature, forward-looking statements involve numerous assumptions, known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts, projections and other forward-looking statements will not occur. Although the Corporation believes that the expectations represented by such forward-looking statements are reasonable and reflect the current views of the Corporation with respect to future events, there can be no assurance that such assumptions and expectations will prove to be correct.

The factors or assumptions on which the forward-looking information is based include, but are not limited to: the assumptions outlined in the Corporation’s guidance document as posted on the Corporation’s website at www.cdnoilsands.com as of April 30, 2014 and as subsequently amended or replaced from time to time, including without limitation, the assumptions as to production, operating expenses and oil prices; the successful and timely implementation of capital projects; Syncrude’s major project spending plans; the ability to obtain regulatory and Syncrude joint venture owner approval; our ability to either generate sufficient cash flow from operations to meet our current and future obligations or obtain external sources of debt and equity capital; the continuation of assumed tax, royalty and regulatory regimes and the accuracy of the estimates of our reserves and resources volumes.

Some of the risks and other factors which could cause actual results or events to differ materially from current expectations expressed in the forward-looking statements contained in this MD&A and the related press release include, but are not limited to: volatility of crude oil prices; volatility of the synthetic crude oil (“SCO”) to WTI differential; the impact that pipeline capacity and apportionment and refinery demand have on prices for SCO; the impacts of regulatory changes especially those which relate to royalties, taxation, tailings, water and the environment; the impact of new technologies on the cost of oil sands mining; the impacts of rising costs associated with tailings and water management; the inability of Syncrude to obtain required consents, permits or approvals, including without limitation, the inability of Syncrude to obtain approval to release water from its operations; the impact of Syncrude being unable to meet the conditions of its approval for its tailings management plan under Directive 074; various events which could disrupt operations including fires, equipment failures and severe weather; unsuccessful or untimely implementation of capital or maintenance projects; the impact of technology on operations and processes and how new complex technology may not perform as expected; the obtaining of required owner approvals from the Syncrude owners for expansions, operational issues and contractual issues; labour turnover and shortages and the productivity achieved from labour in the Fort McMurray area; uncertainty of estimates with respect to reserves and resources; the supply and demand metrics for oil and natural gas; currency and interest rate fluctuations; volatility of natural gas prices; the Corporation’s ability to either generate sufficient cash flow from operations to meet its current and future obligations or obtain external sources of debt and equity capital; the inability of the Corporation to continue to meet the listing requirements of the Toronto Stock Exchange; general economic, business and market conditions and such other risks and uncertainties described in the Corporation’s AIF dated February 20, 2014 and in the reports and filings made with securities regulatory authorities from time to time by the Corporation which are available on the Corporation’s profile on SEDAR at www.sedar.com and on the Corporation’s website at www.cdnoilsands.com.

You are cautioned that the foregoing list of important factors is not exhaustive. Furthermore, the forward-looking statements contained in this MD&A and the related press release are made as of April 30, 2014, and unless required by law, the Corporation does not undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise. The forward-looking statements contained in this MD&A and the related press release are expressly qualified by this cautionary statement.

Additional GAAP Financial Measures

In this MD&A and the related press release, we refer to additional GAAP financial measures that do not have any standardized meaning as prescribed by Canadian GAAP. Additional GAAP financial measures are line items, headings or subtotals in addition to those required under Canadian GAAP, and financial measures disclosed in the notes to the financial statements which are relevant to an understanding of the financial statements and are not presented elsewhere in the financial statements. These measures have been described and presented in order to provide shareholders and potential investors with additional measures for analyzing our ability to generate funds to finance our operations and information regarding our liquidity. Users are cautioned that additional GAAP financial measures presented by the Corporation may not be comparable with measures provided by other entities.

Additional GAAP financial measures include: cash flow from operations, cash flow from operations per Share, net debt, total net capitalization, total capitalization, net debt-to-total net capitalization and long-term debt-to-total capitalization.

Cash flow from operations is calculated as cash from operating activities before changes in non-cash working capital. Cash flow from operations per Share is calculated as cash flow from operations divided by the weighted-average number of Shares outstanding in the period. Because cash flow from operations and cash flow from operations per Share are not impacted by fluctuations in non-cash working capital balances, we believe these measures are more indicative of operational performance than cash from operating activities. With the exception of current taxes, liabilities for Crown royalties and the current portion of our asset retirement obligation, our non-cash working capital is liquid and typically settles within 30 days.

Cash flow from operations is reconciled to cash from operating activities as follows:

| Three Months Ended March 31 | |||||

| ($ millions) | 2014 | 2013 | |||

| Cash flow from operations1 | $ | 357 | $ | 275 | |

| Change in non-cash working capital1 | (479 | ) | 54 | ||

| Cash from (used in) operating activities1 | $ | (122 | ) | $ | 329 |

| 1 As reported in the Consolidated Statements of Cash Flows. | |||||

Net debt, total net capitalization, total capitalization, net debt-to-total net capitalization and long-term debt-to-total capitalization are used by the Corporation to analyze liquidity and manage capital, as discussed in the “Liquidity and Capital Resources” section of this MD&A and in Note 12 to the unaudited consolidated financial statements for the three months ended March 31, 2014.

Overview

Canadian Oil Sands generated higher-than-forecast cash flow from operations in the first quarter of 2014 as stable production from the Syncrude Joint Venture (“Syncrude”) and a strong realized selling price for our Synthetic crude oil (“SCO”) more than offset the impact of high natural gas prices. Syncrude production totalled 26.3 million barrels, or 292,500 barrels per day, and COS realized a $106 per barrel average selling price, 20 per cent higher than the $88 per barrel forecast in our January 2014 Outlook.

Operating expenses totalled $445 million, or $46.91 per barrel, reflecting higher-than-forecast natural gas prices as well as planned maintenance, tailings management and drilling activities. With the exception of natural gas prices, the increased operating expenses were anticipated and in line with budget expectations.

Capital expenditures on the Mildred Lake Mine Train Replacement project are trending below budget and the project remains on schedule for completion in the fourth quarter of this year. Accordingly, we have reduced our total cost estimate from $4.2 billion to $3.9 billion (gross to Syncrude), tightened the range around this estimate, and reduced total forecast capital expenditures for 2014. The Centrifuge Tailings Management project continues to track to budget and remains on schedule for completion in the first half of 2015.

Net debt rose to $1.4 billion at March 31, 2014, as cash balances were used to settle approximately $500 million of existing liabilities for Crown royalties and taxes while a weakening Canadian dollar increased the carrying value of our long-term debt. Cash flow from operations of $357 million was almost sufficient to fund first quarter capital expenditures of $217 million and dividends of $170 million.

On April 24, Syncrude commenced maintenance work on Coker 8-1 following an interruption in the unit’s operation in order to repair a valve leak. The maintenance work is expected to overlap the Coker 8-2 turnaround scheduled for the second quarter.

We have revised our 2014 Outlook to reflect lower estimated annual Syncrude production ranging from 95 to 105 million barrels with a single-point estimate of 100 million barrels (274,000 barrels per day). Estimated sales, net of crude oil purchases and transportation expense, have risen to $3,528 million, reflecting a higher $96 per barrel annual realized selling price and the revised production estimate. We are also estimating: increased operating expenses, reflecting a higher natural gas price assumption and actual results incurred in the first quarter of the year; and, lower capital expenditures, reflecting the reduction in the Mildred Lake Mine Train Replacement cost estimate and adjustments to spending on regular maintenance capital projects. As a result of these revisions, estimated 2014 cash flow from operations has increased $36 million to approximately $1.2 billion and estimated capital expenditures have fallen to approximately $0.9 billion. Given the assumptions in our Outlook, we expect net debt levels to be within our targeted range of $1 billion to $2 billion at year end.

| Highlights | ||||||

| Three Months Ended March 31 | ||||||

| 2014 | 2013 | |||||

| Cash flow from operations1 ($ millions) | $ | 357 | $ | 275 | ||

| Per Share1 ($/Share) | $ | 0.74 | $ | 0.57 | ||

| Net income ($ millions) | $ | 172 | $ | 177 | ||

| Per Share, Basic and Diluted ($/Share) | $ | 0.35 | $ | 0.37 | ||

| Sales volumes2 | ||||||

| Total (mmbbls) | 9.5 | 8.6 | ||||

| Daily average (bbls) | 105,283 | 95,683 | ||||

| Realized SCO selling price ($/bbl) | $ | 105.73 | $ | 96.11 | ||

| West Texas Intermediate (“WTI”) (average $US/bbl) | $ | 98.61 | $ | 94.36 | ||

| SCO premium (discount) to WTI (weighted average $/bbl) | $ | (2.93 | ) | $ | 1.00 | |

| Average foreign exchange rate ($US/$Cdn) | $ | 0.91 | $ | 0.99 | ||

| Operating expenses ($ millions) | $ | 445 | $ | 355 | ||

| Per barrel ($/bbl) | $ | 46.91 | $ | 41.20 | ||

| Capital expenditures ($ millions) | $ | 217 | $ | 268 | ||

| Dividends ($ millions) | $ | 170 | $ | 170 | ||

| Per Share ($/Share) | $ | 0.35 | $ | 0.35 | ||

| 1 Cash flow from operations and cash flow from operations per Share are additional GAAP financial measures and are defined in the “Additional GAAP Financial Measures” section of this MD&A. | ||||||

| 2 The Corporation’s sales volumes differ from its production volumes due to changes in inventory, which are primarily in-transit pipeline volumes. Sales volumes are net of purchases. | ||||||

Review of Financial Results

Cash Flow from Operations

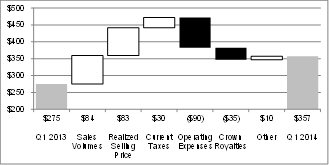

Q1 2014 versus Q1 2013 ($ millions)

To view graph comparison, visit the following link: http://media3.marketwire.com/docs/COSg.jpg

Cash flow from operations increased to $357 million, or $0.74 per Share, in the first quarter of 2014 from $275 million, or $0.57 per Share, in the first quarter of 2013 as higher sales volumes, a higher realized selling price and lower current taxes more than offset the impact of higher operating expenses and Crown royalties.

Syncrude production in the 2014 first quarter totalled 26.3 million barrels, or 292,500 barrels per day, a 12 per cent increase over the 23.4 million barrels, or 260,400 barrels per day, produced in the 2013 first quarter when volumes were impacted by unplanned outages in extraction and secondary upgrading units. Net to the Corporation, sales volumes increased to 9.5 million barrels, or 105,300 barrels per day, in the first quarter of 2014 from 8.6 million barrels, or 95,700 barrels per day, in the comparative 2013 quarter.

The average realized selling price increased to $105.73 per barrel in the first quarter of 2014 from $96.11 per barrel in the same quarter of 2013, primarily due to a weaker Canadian dollar as higher WTI oil prices offset a deterioration in the SCO differential to WTI.

Operating expenses in the 2014 quarter increased $90 million to $46.91 per barrel, reflecting higher natural gas prices, the timing of planned maintenance and tailings management activities, and increased drilling relative to the comparative 2013 quarter.

The changes in the components of cash flow from operations are discussed in greater detail later in this MD&A.

Net Income

Canadian Oil Sands reported net income of $172 million, or $0.35 per Share, in the first quarter of 2014 compared with $177 million, or $0.37 per Share, in the first quarter of 2013. The factors which produced an $82 million increase in cash flow from operations also impacted net income; however, these were offset by a $37 million increase in deferred tax expense and a $26 million larger unrealized foreign exchange loss on long-term debt in 2014. The changes in the components of net income are discussed in greater detail later in this MD&A.

The following table shows the net income components per barrel of SCO:

| Three Months Ended March 31 | |||||||||

| ($ per barrel)1 | 2014 | 2013 | Change | ||||||

| Sales net of crude oil purchases and transportation expense | $ | 105.06 | $ | 96.16 | $ | 8.90 | |||

| Operating expense | (46.91 | ) | (41.20 | ) | (5.71 | ) | |||

| Crown royalties | (6.13 | ) | (2.69 | ) | (3.44 | ) | |||

| $ | 52.02 | $ | 52.27 | $ | (0.25 | ) | |||

| Development expense | $ | (3.42 | ) | $ | (2.97 | ) | $ | (0.45 | ) |

| Administration and insurance expenses | (1.74 | ) | (1.78 | ) | 0.04 | ||||

| Depreciation and depletion expense | (13.58 | ) | (14.19 | ) | 0.61 | ||||

| Net finance expense | (1.44 | ) | (1.58 | ) | 0.14 | ||||

| Foreign exchange loss | (5.77 | ) | (3.21 | ) | (2.56 | ) | |||

| Tax expense | (7.94 | ) | (7.95 | ) | 0.01 | ||||

| (33.89 | ) | (31.68 | ) | (2.21 | ) | ||||

| Net income per barrel | $ | 18.13 | $ | 20.59 | $ | (2.46 | ) | ||

| Sales volumes (mmbbls)2 | 9.5 | 8.6 | 0.9 | ||||||

| 1 Per barrel measures derived by dividing the relevant item by sales volumes in the period. | |||||||||

| 2 Sales volumes, net of purchased crude oil volumes. | |||||||||

| Sales Net of Crude Oil Purchases and Transportation Expense | ||||||||||

| Three Months Ended March 31 | ||||||||||

| ($ millions, except where otherwise noted) | 2014 | 2013 | Change | |||||||

| Sales1 | $ | 1,114 | $ | 961 | $ | 153 | ||||

| Crude oil purchases | (105 | ) | (124 | ) | 19 | |||||

| Transportation expense | (14 | ) | (9 | ) | (5 | ) | ||||

| $ | 995 | $ | 828 | $ | 167 | |||||

| Sales volumes2 | ||||||||||

| Total (mmbbls) | 9.5 | 8.6 | 0.9 | |||||||

| Daily average (bbls) | 105,283 | 95,683 | 9,600 | |||||||

| Realized SCO selling price (average $Cdn/bbl)3 | $ | 105.73 | $ | 96.11 | $ | 9.62 | ||||

| West Texas Intermediate (“WTI”) (average $US/bbl) | $ | 98.61 | $ | 94.36 | $ | 4.25 | ||||

| SCO premium (discount) to WTI (weighted-average $Cdn/bbl) | $ | (2.93 | ) | $ | 1.00 | $ | (3.93 | ) | ||

| Average foreign exchange rate ($US/$Cdn) | $ | 0.91 | $ | 0.99 | $ | (0.08 | ) | |||

| 1 Sales include sales of purchased crude oil and sulphur. | ||||||||||

| 2 Sales volumes, net of purchased crude oil volumes. | ||||||||||

| 3 Sales net of crude oil purchases and transportation expense divided by sales volumes. | ||||||||||

The $167 million, or 20 per cent, increase in first quarter 2014 sales, net of crude oil purchases and transportation expense, reflects increased sales volumes and a higher realized selling price relative to the 2013 first quarter.

The Corporation purchases crude oil from third parties to fulfill sales commitments with customers when there are shortfalls

in Syncrude’s production and to facilitate certain transportation arrangements. Sales include the sale of purchased crude oil while the cost of these purchases is included in crude oil purchases and transportation expense. Lower crude oil purchases in the first quarter 2014 reflect more stable production than 2013.

Operating Expenses

The following table shows the major components of operating expenses in total dollars and per barrel of SCO:

| Three Months Ended March 31 | ||||||||

| 2014 | 2013 | |||||||

| $ millions | $ per bbl | $ millions | $ per bbl | |||||

| Production and maintenance1 | $ | 332 | $ | 35.04 | $ | 282 | $ | 32.70 |

| Natural gas and diesel purchases2 | 71 | 7.52 | 44 | 5.12 | ||||

| Syncrude pension and incentive compensation | 30 | 3.12 | 21 | 2.50 | ||||

| Other3 | 12 | 1.23 | 8 | 0.88 | ||||

| Total operating expenses | $ | 445 | $ | 46.91 | $ | 355 | $ | 41.20 |

| 1 Includes non-major turnaround costs. Major turnaround costs are capitalized as property, plant and equipment. | ||||||||

| 2 Includes costs to purchase natural gas used to produce energy and hydrogen and diesel consumed as fuel. | ||||||||

| 3 Includes fees for management services provided by Imperial Oil Resources, insurance premiums, and greenhouse gas emissions levies. | ||||||||

The increase in operating expenses in the first quarter of 2014 reflects the timing of planned maintenance and tailings management activities as well as increased drilling activity. In addition, a $2.48 per GJ increase in natural gas prices to $5.43 per GJ raised natural gas purchases.

Variances in per-barrel operating expenses also reflect changes in sales volumes, which were higher in the first quarter of 2014.

The following table shows operating expenses per barrel of bitumen and SCO. Costs are allocated to bitumen production and upgrading on the basis used to determine Crown royalties.

| Three Months Ended March 31 | ||||||||||

| 2014 | 20133 | |||||||||

| ($ per barrel) | Bitumen | SCO | Bitumen | SCO | ||||||

| Bitumen production | $ | 29.79 | $ | 35.41 | $ | 26.43 | $ | 32.36 | ||

| Internal fuel allocation1 | 3.10 | 3.69 | 2.65 | 3.25 | ||||||

| Total bitumen production expenses | $ | 32.89 | $ | 39.10 | $ | 29.08 | $ | 35.61 | ||

| Upgrading2 | $ | 11.50 | $ | 8.84 | ||||||

| Less: internal fuel allocation1 | (3.69 | ) | (3.25 | ) | ||||||

| Total upgrading expenses | $ | 7.81 | $ | 5.59 | ||||||

| Total operating expenses | $ | 46.91 | $ | 41.20 | ||||||

| (thousands of barrels per day) | ||||||||||

| Syncrude production volumes | 348 | 293 | 319 | 260 | ||||||

| Canadian Oil Sands sales volumes | 105 | 96 | ||||||||

| 1 Reflects energy generated by the upgrader that is used in the bitumen production process and is valued by reference to natural gas and diesel prices. Natural gas prices averaged $5.43 per GJ and $2.95 per GJ in the three months ended March 31, 2014 and March 31, 2013, respectively. Diesel prices averaged $1.08 per litre and $0.90 per litre in the three months ended March 31, 2014 and March 31, 2013, respectively. | ||||||||||

| 2 Upgrading expenses include the production and maintenance expenses associated with processing and upgrading bitumen to SCO. | ||||||||||

| 3 Certain 2013 comparative amounts have been restated to conform to the current year presentation. | ||||||||||

Crown Royalties

Crown royalties increased to $58 million in the first quarter of 2014 from $23 million in the first quarter of 2013, reflecting an increase in the deemed bitumen price used to calculate Crown royalties and higher bitumen production volumes in 2014.

| Net Finance Expense | ||||||

| Three Months Ended March 31 | ||||||

| ($ millions) | 2014 | 2013 | ||||

| Interest costs on long-term debt | $ | 30 | $ | 31 | ||

| Less capitalized interest on long-term debt | (24 | ) | (23 | ) | ||

| Interest expense on long-term debt | $ | 6 | $ | 8 | ||

| Interest expense on employee future benefits | 3 | 4 | ||||

| Accretion of asset retirement obligation | 7 | 6 | ||||

| Interest income | (2 | ) | (5 | ) | ||

| Net finance expense | $ | 14 | $ | 13 | ||

Interest costs on the Corporation’s U.S. dollar-denominated long-term debt reflect lower average outstanding debt levels in the first quarter of 2014 due to a U.S. $300 million debt repayment in August, 2013, offset by a weaker Canadian dollar relative to the first quarter of 2013.

| Foreign Exchange (Gain) Loss | ||||||

| Three Months Ended March 31 | ||||||

| ($ millions) | 2014 | 2013 | ||||

| Foreign exchange loss – long-term debt | $ | 63 | $ | 37 | ||

| Foreign exchange gain – other | (9 | ) | (9 | ) | ||

| Total foreign exchange loss | $ | 54 | $ | 28 | ||

Foreign exchange gains and losses are the result of revaluations of the Corporation’s U.S. dollar-denominated long-term debt, accounts receivable and cash into Canadian dollars.

The foreign exchange losses reflect a weakening Canadian dollar in the first quarter of 2014 (from U.S. $0.94 at December 31, 2013 to U.S. $0.90 at March 31, 2014) and 2013 (from U.S. $1.01 at December 31, 2012 to U.S. $0.98 at March 31, 2013).

| Tax Expense | |||||

| Three Months Ended March 31 | |||||

| ($ millions) | 2014 | 2013 | |||

| Current tax expense | $ | 60 | $ | 90 | |

| Deferred tax expense (recovery) | 15 | (22 | ) | ||

| Total tax expense | $ | 75 | $ | 68 | |

Taxes on a portion of the income generated in the Corporation’s partnership in 2012 were deferred to 2013 and, to a lesser extent, to 2014. As a result, current taxes decreased $30 million in 2014 and deferred taxes increased $37 million.

| Asset Retirement Obligation | ||||||

| Three Months | Year | |||||

| Ended | Ended | |||||

| March 31 | December 31 | |||||

| ($ millions) | 2014 | 2013 | ||||

| Asset retirement obligation, beginning of period | $ | 896 | $ | 1,102 | ||

| (Increase) decrease in risk-free interest rate | 50 | (217 | ) | |||

| Reclamation expenditures | (17 | ) | (42 | ) | ||

| Increase (decrease) in estimated reclamation and closure expenditures | (14 | ) | 27 | |||

| Accretion expense | 7 | 26 | ||||

| Asset retirement obligation, end of period | $ | 922 | $ | 896 | ||

| Less current portion | (28 | ) | (28 | ) | ||

| Non-current portion | $ | 894 | $ | 868 | ||

Canadian Oil Sands’ asset retirement obligation increased from $896 million at December 31, 2013 to $922 million at March 31, 2014 primarily due to a decrease in the interest rate used to discount future reclamation and closure expenditures from 3.25 per cent at December 31, 2013 to 3.0 per cent at March 31, 2014.

| Pension and Other Post-Employment Benefit Plans | |||||||

| Three Months | Year | ||||||

| Ended | Ended | ||||||

| March 31 | December 31 | ||||||

| ($ millions) | 2014 | 2013 | |||||

| Accrued benefit liability, beginning of period | $ | 308 | $ | 438 | |||

| Current service cost | 11 | 45 | |||||

| Interest expense | 3 | 16 | |||||

| Contributions | (28 | ) | (109 | ) | |||

| Re-measurement (gains) losses: | |||||||

| Actual return on plan assets in excess of estimated return1 | (33 | ) | (46 | ) | |||

| Increase in discount rate | – | (91 | ) | ||||

| Other2 | – | 55 | |||||

| Accrued benefit liability, end of period | $ | 261 | $ | 308 | |||

| Less current portion | (42 | ) | (82 | ) | |||

| Non-current portion | $ | 219 | $ | 226 | |||

| 1 Estimated return is based on prescribed 4.5 per cent annualized rate. | |||||||

| 2 The other re-measurement loss in 2013 reflects an increase in the estimated average lifespan of the plans’ beneficiaries as a result of new actuarial standards. | |||||||

The Corporation’s obligation for Syncrude Canada Ltd.’s (“Syncrude Canada”) pension and other post-employment benefits in excess of the fair value of the assets held in the benefit plans (the “accrued benefit liability”) decreased to $261 million at March 31, 2014 from $308 million at December 31, 2013 as actual returns on plan assets were higher than expected and contributions to the plans exceeded current period expenses.

| Summary of Quarterly Results | |||||||||||||||||||||

| 2014 | 2013 | 20126 | |||||||||||||||||||

| Q1 | Q4 | Q3 | Q2 | Q1 | Q4 | Q3 | Q2 | ||||||||||||||

| Sales1 ($ millions) | $ | 995 | $ | 945 | $ | 871 | $ | 921 | $ | 828 | $ | 929 | $ | 941 | $ | 740 | |||||

| Net income ($ millions) | $ | 172 | $ | 192 | $ | 246 | $ | 219 | $ | 177 | $ | 218 | $ | 336 | $ | 101 | |||||

| Per Share, Basic & Diluted | $ | 0.35 | $ | 0.40 | $ | 0.51 | $ | 0.45 | $ | 0.37 | $ | 0.45 | $ | 0.69 | $ | 0.21 | |||||

| Cash flow from operations2 ($ millions) | $ | 357 | $ | 392 | $ | 339 | $ | 343 | $ | 275 | $ | 418 | $ | 470 | $ | 245 | |||||

| Per Share2 | $ | 0.74 | $ | 0.81 | $ | 0.70 | $ | 0.71 | $ | 0.57 | $ | 0.86 | $ | 0.97 | $ | 0.51 | |||||

| Dividends ($ millions) | $ | 170 | $ | 169 | $ | 170 | $ | 169 | $ | 170 | $ | 169 | $ | 170 | $ | 170 | |||||

| Per Share | $ | 0.35 | $ | 0.35 | $ | 0.35 | $ | 0.35 | $ | 0.35 | $ | 0.35 | $ | 0.35 | $ | 0.35 | |||||

| Daily average sales volumes3 (bbls) | 105,283 | 112,092 | 84,250 | 100,094 | 95,683 | 111,669 | 113,331 | 89,460 | |||||||||||||

| Realized SCO selling price ($/bbl) | $ | 105.73 | $ | 91.47 | $ | 112.55 | $ | 100.90 | $ | 96.11 | $ | 89.99 | $ | 89.89 | $ | 90.59 | |||||

| WTI4 (average $US/bbl) | $ | 98.61 | $ | 97.61 | $ | 105.81 | $ | 94.17 | $ | 94.36 | $ | 88.23 | $ | 92.20 | $ | 93.35 | |||||

| SCO premium (discount) to WTI | $ | (2.93 | ) | $ | (10.84 | ) | $ | 2.63 | $ | 4.79 | $ | 1.00 | $ | 2.52 | $ | (2.00 | ) | $ | (5.20 | ) | |

| (weighted-average $/bbl) | |||||||||||||||||||||

| Operating expenses5 ($/bbl) | $ | 46.91 | $ | 37.60 | $ | 46.15 | $ | 43.23 | $ | 41.20 | $ | 38.76 | $ | 36.07 | $ | 50.25 | |||||

| Purchased natural gas price ($/GJ) | $ | 5.43 | $ | 3.28 | $ | 2.59 | $ | 3.41 | $ | 2.95 | $ | 3.02 | $ | 2.23 | $ | 1.79 | |||||

| Foreign exchange rates ($US/$Cdn) | |||||||||||||||||||||

| Average | $ | 0.91 | $ | 0.95 | $ | 0.96 | $ | 0.98 | $ | 0.99 | $ | 1.01 | $ | 1.00 | $ | 0.99 | |||||

| Quarter-end | $ | 0.90 | $ | 0.94 | $ | 0.97 | $ | 0.95 | $ | 0.98 | $ | 1.01 | $ | 1.02 | $ | 0.98 | |||||

| 1 Sales after crude oil purchases and transportation expense. | |||||||||||||||||||||

| 2 Cash flow from operations and cash flow from operations per Share are additional GAAP financial measures and are defined in the “Additional GAAP Financial Measures” section of this MD&A. | |||||||||||||||||||||

| 3 Daily average sales volumes net of crude oil purchases. | |||||||||||||||||||||

| 4 Pricing obtained from Bloomberg. | |||||||||||||||||||||

| 5 Derived from operating expenses, as reported on the Consolidated Statements of Income and Comprehensive Income, divided by sales volumes during the period. | |||||||||||||||||||||

| 6 Net income and operating expenses in 2012 have been adjusted to reflect amendments to International Accounting Standard (“IAS”) 19, Employee Benefits. | |||||||||||||||||||||

During the last eight quarters, the following items have had a significant impact on the Corporation’s financial results and may impact the financial results in the future:

Increased spending on capital projects to replace or relocate Syncrude mine trains and to support tailings management plans has increased capital expenditures and reduced Crown royalties over the past eight quarters. These projects are expected to be substantially complete by the end of 2014, reducing capital deductions for Crown royalties as project risk declines.

| Capital Expenditures | |||||

| Three Months Ended March 31 | |||||

| ($ millions) | 2014 | 2013 | |||

| Major Projects | |||||

| Mildred Lake Mine Train Replacements | $ | 88 | $ | 113 | |

| Centrifuge Tailings Management | 73 | 37 | |||

| Aurora North Mine Train Relocations | – | 31 | |||

| Aurora North Tailings Management | – | 13 | |||

| Capital expenditures on major projects | $ | 161 | $ | 194 | |

| Regular maintenance | |||||

| Capitalized turnaround costs | 3 | 2 | |||

| Other | 29 | 49 | |||

| Capital expenditures on regular maintenance | $ | 32 | $ | 51 | |

| Capitalized interest | $ | 24 | $ | 23 | |

| Total capital expenditures | $ | 217 | $ | 268 | |

Capital expenditures decreased to $217 million in the first quarter of 2014 reflecting lower spending on the major projects with the completion of the Aurora North Mine Train Relocation and Aurora North Tailings Management projects in 2013. As well, regular maintenance capital expenditures, primarily projects to relocate some of Syncrude’s tailings facilities, were lower compared with the first quarter of 2013. More information on the major projects is provided in the “Outlook” section of this MD&A.

Contractual Obligations and Commitments

Canadian Oil Sands’ contractual obligations and commitments are summarized in the 2013 annual MD&A and include future cash payments that the Corporation is required to make under existing contractual arrangements entered into directly or as a 36.74 per cent owner in Syncrude. During 2014, Canadian Oil Sands assumed $75 million in new funding commitments relating to capital projects while the Corporation’s share of payments prescribed by regulations on Syncrude Canada’s registered pension plans decreased by approximately $200 million as a result of an actuarial valuation completed in April, 2014.

Dividends

On April 30, 2014, the Corporation declared a quarterly dividend of $0.35 per Share for a total dividend of approximately $170 million. The dividend will be paid on May 30, 2014 to shareholders of record on May 23, 2014. The Corporation paid dividends to shareholders totalling $170 million, or $0.35 per Share, in the first quarter of 2014.

Dividend payments are set quarterly by the Board of Directors in the context of current and expected crude oil prices, economic conditions, Syncrude’s operating performance, and the Corporation’s capacity to finance operating and investing obligations. Dividend amounts are established with the intent of absorbing short-term market volatility over several quarters and recognize our intention to fund the current major projects primarily with cash flow from operations and existing cash balances, while maintaining a strong balance sheet to reduce exposure to potential oil price declines, cost increases or major operational upsets.

| Liquidity and Capital Resources | ||||||

| March 31 | December 31 | |||||

| As at ($ millions, except % amounts) | 2014 | 2013 | ||||

| Long-term debt1 | $ | 1,665 | $ | 1,602 | ||

| Cash and cash equivalents1 | (292 | ) | (806 | ) | ||

| Net debt2,3 | $ | 1,373 | $ | 796 | ||

| Shareholders’ equity1 | $ | 4,759 | $ | 4,732 | ||

| Total net capitalization2,4 | $ | 6,132 | $ | 5,528 | ||

| Total capitalization2,5 | $ | 6,424 | $ | 6,334 | ||

| Net debt-to-total net capitalization2,6 (%) | 22 | 14 | ||||

| Long-term debt-to-total capitalization2,7 (%) | 26 | 25 | ||||

| 1 As reported in the Consolidated Balance Sheets. | ||||||

| 2 Additional GAAP financial measure. | ||||||

| 3 Long-term debt less cash and cash equivalents. | ||||||

| 4 Net debt plus Shareholders’ equity. | ||||||

| 5 Long-term debt plus Shareholders’ equity. | ||||||

| 6 Net debt divided by total net capitalization. | ||||||

| 7 Long-term debt divided by total capitalization. | ||||||

Net debt, which is comprised of long-term debt less cash and cash equivalents, rose $577 million to $1,373 million at March 31, 2014 as cash balances were used to settle existing liabilities of approximately $500 million for Crown royalties and taxes, while a weakening Canadian dollar increased the carrying value of our long-term debt by $63 million. Cash flow from operations was almost sufficient to fund first quarter capital expenditures of $217 million and dividends of $170 million. As a result, net debt-to-total net capitalization increased to 22 per cent at March 31, 2014 from 14 per cent at December 31, 2013.

We plan to use existing cash to fund capital expenditures and dividends. Based on the assumptions in our 2014 Outlook, we expect net debt to be within our targeted range of $1 billion to $2 billion at year end, coincident with the substantial completion of our major projects.

Shareholders’ equity increased to $4,759 million at March 31, 2014 from $4,732 million at December 31, 2013, as comprehensive income exceeded dividends in the first quarter of 2014.

Canadian Oil Sands has a $1,500 million operating credit facility which expires June 1, 2017 and a $40 million extendible revolving term credit facility which expires June 30, 2015. No amounts were drawn against these facilities at March 31, 2014 or December 31, 2013.

The Senior Notes indentures and credit facility agreements contain certain covenants that restrict Canadian Oil Sands’ ability to sell all or substantially all of its assets or change the nature of its business, and limit long-term debt-to-total capitalization to 55 per cent. Canadian Oil Sands is in compliance with its debt covenants, and with a long-term debt-to-total capitalization of 26 per cent at March 31, 2014, a significant increase in debt or decrease in equity would be required to negatively impact the Corporation’s financial flexibility.

Shareholders’ Capital and Trading Activity

The Corporation’s shares trade on the Toronto Stock Exchange under the symbol COS. On March 31, 2014, the Corporation had a market capitalization of approximately $11.2 billion with 484.6 million shares outstanding and a closing price of $23.19 per Share. The following table summarizes the trading activity for the first quarter of 2014.

| Canadian Oil Sands Limited – Trading Activity | |||||||||

| First | |||||||||

| Quarter | January | February | March | ||||||

| 2014 | 2014 | 2014 | 2014 | ||||||

| Share price | |||||||||

| High | $ | 23.39 | $ | 20.59 | $ | 21.59 | $ | 23.39 | |

| Low | $ | 19.64 | $ | 19.64 | $ | 19.78 | $ | 21.02 | |

| Close | $ | 23.19 | $ | 20.02 | $ | 21.11 | $ | 23.19 | |

| Volume of Shares traded (millions) | 87.7 | 25.2 | 32.8 | 29.7 | |||||

| Weighted average Shares outstanding (millions) | 484.6 | 484.6 | 484.6 | 484.6 | |||||

| 2014 Outlook | ||||||

| (millions of Canadian dollars, except volume and per barrel amounts) | ||||||

| As of | As of | |||||

| April 30 | January 30 | |||||

| 2014 | 2014 | |||||

| Operating assumptions | ||||||

| Syncrude production (mmbbls) | 100 | 105 | ||||

| Canadian Oil Sands sales (mmbbls) | 36.7 | 38.6 | ||||

| Sales, net of crude oil purchases and transportation | $ | 3,528 | $ | 3,386 | ||

| Realized SCO selling price ($/bbl) | $ | 96.02 | $ | 87.77 | ||

| Operating expenses | $ | 1,693 | $ | 1,600 | ||

| Operating expenses per barrel | $ | 46.08 | $ | 41.48 | ||

| Development expenses | $ | 176 | $ | 181 | ||

| Crown royalties | $ | 160 | $ | 128 | ||

| Current taxes | $ | 200 | $ | 200 | ||

| Cash flow from operations1 | $ | 1,194 | $ | 1,158 | ||

| Capital expenditure assumptions | ||||||

| Major projects | $ | 575 | $ | 653 | ||

| Regular maintenance | $ | 267 | $ | 361 | ||

| Capitalized interest | $ | 86 | $ | 83 | ||

| Total capital expenditures | $ | 928 | $ | 1,097 | ||

| Business environment assumptions | ||||||

| West Texas Intermediate (U.S.$/bbl) | $ | 92.00 | $ | 90.00 | ||

| Discount to average Cdn$ WTI prices (Cdn$/bbl) | $ | (4.00 | ) | $ | (5.00 | ) |

| Foreign exchange rate (U.S.$/Cdn$) | $ | 0.92 | $ | 0.97 | ||

| AECO natural gas (Cdn$/GJ) | $ | 4.50 | $ | 3.50 | ||

| 1 Cash flow from operations is an additional GAAP financial measure and is defined in the “Additional GAAP Financial Measures” section of this MD&A. | ||||||

We have lowered our 2014 Syncrude production estimate to range between 95 and 105 million barrels, with a single-point estimate of 100 million barrels (274,000 barrels per day). Net to Canadian Oil Sands, the single-point estimate is equivalent to 36.7 million barrels (100,700 barrels per day). This change reflects an unplanned Coker 8-1 outage to remove coke deposits following a valve leak repair. The revised estimate incorporates the additional complexity resulting from the overlap with our planned Coker 8-2 turnaround and continues to reflect the successful startup of the new Mildred Lake mine trains in the fourth quarter.

Estimated 2014 sales, net of crude oil purchases and transportation expense, have risen to $3,528 million, reflecting an increase in the forecast realized selling price and the revised production estimate.

The forecast selling price has increased $8 per barrel to $96 per barrel and assumes a U.S. $92 per barrel WTI oil price, a $4 per barrel SCO discount to Canadian dollar WTI and a foreign exchange rate of $0.92 U.S./Cdn.

We have increased forecast 2014 operating expenses to $1,693 million to reflect a higher $4.50 per gigajoule (“GJ”) natural gas price assumption and actual results incurred in the first quarter of the year. Based on our revised single-point production estimate, this translates to $46.08 per barrel.

Estimated Crown royalties have increased to $160 million, reflecting an increase in deemed bitumen prices and lower capital deductions, partially offset by lower bitumen production.

Estimated capital expenditures have decreased to $928 million, reflecting a reduction in the Mildred Lake Mine Train Replacement project cost estimate and adjustments to spending on regular maintenance capital projects.

Based on these assumptions, estimated 2014 cash flow from operations has risen to $1,194 million, or $2.46 per Share.

We plan to use existing cash to help fund capital expenditures and dividends. Based on the assumptions in our 2014 Outlook, we expect net debt to be within our targeted range of $1 billion to $2 billion at year end, coincident with the substantial completion of our major projects.

Changes in certain factors and market conditions could potentially impact Canadian Oil Sands’ Outlook. The following table provides a sensitivity analysis of the key factors affecting the Corporation’s performance.

| Outlook Sensitivity Analysis (April 30, 2014) | |||||

| Cash Flow from Operations | |||||

| Increase | |||||

| Variable | Annual Sensitivity | $ millions 1,2 |

$ / Share 1,2 |

||

| Syncrude operating expense decrease | Cdn$1.00/bbl | $ | 22 | $ | 0.05 |

| Syncrude operating expense decrease | Cdn$50 million | $ | 11 | $ | 0.02 |

| WTI crude oil price increase | U.S.$1.00/bbl | $ | 25 | $ | 0.05 |

| Syncrude production increase | 2 million bbls | $ | 44 | $ | 0.09 |

| Canadian dollar weakening | U.S.$0.01/Cdn$ | $ | 25 | $ | 0.05 |

| AECO natural gas price decrease | Cdn$0.50/GJ | $ | 14 | $ | 0.03 |

| 1 These sensitivities are after the impact of taxes. | |||||

| 2 These sensitivities assume Canadian Oil Sands pays Crown royalties based on 25 per cent of net bitumen revenues in 2014. Lower bitumen revenues or higher deductible bitumen-related costs may result in minimum Crown royalties based on 1 per cent of gross revenues which will change the sensitivities to these variables. | |||||

The 2014 Outlook contains forward-looking information and users are cautioned that the actual amounts may vary from the estimates disclosed. Please refer to the “Forward-Looking Information Advisory” section of this MD&A for the risks and assumptions underlying this forward-looking information.

Major Projects

The following tables provide cost and schedule estimates for Syncrude’s major projects. Regular maintenance capital expenditures for years after 2014 will be provided on an annual basis when we disclose the budgets for those years.

| Major Projects – Total Project Cost and Schedule Estimates1 | ||||||

| Total Cost Estimate ($ billions) |

Total Cost Estimate Accuracy (%) |

Estimated % Complete at March 31, 20142 |

Target In-Service Date |

|||

| Mildred Lake Mine Train Replacement | Syncrude | $ | 3.9 | +5% / -10% | 85% | Q4 2014 |

| COS share | 1.4 | |||||

| Centrifuge Tailings Management | Syncrude | $ | 1.9 | +15% / -15% | 75% | H1 2015 |

| COS share | 0.7 | |||||

| Major Projects – Annual Spending Profile1 | ||||||||

| Spent to | ||||||||

| ($ billions) | December 31, 2013 | 2014 | 2015 | Total | ||||

| Syncrude | $ | 3.6 | $ | 1.8 | $ | 0.4 | $ | 5.8 |

| Canadian Oil Sands share | $ | 1.3 | $ | 0.7 | $ | 0.1 | $ | 2.1 |

| 1 Major projects costs include capital expenditures, excluding capitalized interest, and certain development expenses. | ||||||||

| 2 The estimated percentage complete is based on hours spent as a percentage of total forecasted hours to project completion. | ||||||||

Capital expenditures on the Mildred Lake Mine Train Replacement project are trending below budget and the project remains on schedule for completion in the fourth quarter of this year. Accordingly, we have reduced our total cost estimate from $4.2 billion to $3.9 billion (gross to Syncrude) and tightened the range around this estimate. The Centrifuge Tailings Management project continues to track to budget and remains on schedule for completion in the first half of 2015.

The major projects tables contain forward-looking information and users of this information are cautioned that the actual yearly and total major project costs and the actual in-service dates for the major projects may vary from the plans disclosed. The major project cost estimates and major project target in-service dates are based on current spending plans. Please refer to the “Forward-Looking Information Advisory” section of this MD&A for the risks and assumptions underlying this forward-looking information. For a list of additional risk factors that could cause the actual amount of the major project costs and the major project target in-service dates to differ materially, please refer to the Corporation’s Annual Information Form dated February 20, 2014 which is available on the Corporation’s profile on SEDAR at www.sedar.com and on the Corporation’s website at www.cdnoilsands.com.

| Consolidated Statements of Income and Comprehensive Income | ||||||||

| (unaudited) | ||||||||

| (millions of Canadian dollars, except per Share and Share volume amounts) | ||||||||

| Three Months Ended March 31 | ||||||||

| 2014 | 2013 | |||||||

| Sales | $ | 1,114 | $ | 961 | ||||

| Crown royalties | (58 | ) | (23 | ) | ||||

| Revenues | $ | 1,056 | $ | 938 | ||||

| Expenses | ||||||||

| Operating | $ | 445 | $ | 355 | ||||

| Development | 32 | 26 | ||||||

| Crude oil purchases and transportation | 119 | 133 | ||||||

| Administration | 10 | 10 | ||||||

| Insurance | 6 | 6 | ||||||

| Depreciation and depletion | 129 | 122 | ||||||

| $ | 741 | $ | 652 | |||||

| Earnings from operating activities | $ | 315 | $ | 286 | ||||

| Foreign exchange loss (Note 9) | 54 | 28 | ||||||

| Net finance expense (Note 10) | 14 | 13 | ||||||

| Earnings before taxes | $ | 247 | $ | 245 | ||||

| Tax expense (Note 11) | 75 | 68 | ||||||

| Net income | $ | 172 | $ | 177 | ||||

| Other comprehensive income (loss), net of taxes | ||||||||

| Items not reclassified to net income: | ||||||||

| Re-measurements of employee future benefit plans (Note 6) | 24 | 14 | ||||||

| Items reclassified to net income: | ||||||||

| Derivative gains | (1 | ) | (1 | ) | ||||

| Comprehensive income | $ | 195 | $ | 190 | ||||

| Weighted average Shares (millions) | 485 | 485 | ||||||

| Shares, end of period (millions) | 485 | 485 | ||||||

| Net income per Share | ||||||||

| Basic and diluted | $ | 0.35 | $ | 0.37 | ||||

| See Notes to Unaudited Consolidated Financial Statements | ||||||||

| Consolidated Statements of Shareholders’ Equity | |||||||

| (unaudited) | |||||||

| Three Months Ended March 31 | |||||||

| (millions of Canadian dollars) | 2014 | 2013 | |||||

| Retained earnings | |||||||

| Balance, beginning of period | $ | 2,040 | $ | 1,823 | |||

| Net income | 172 | 177 | |||||

| Re-measurements of employee future benefit plans | 24 | 14 | |||||

| Dividends | (170 | ) | (170 | ) | |||

| Balance, end of period | $ | 2,066 | $ | 1,844 | |||

| Accumulated other comprehensive income | |||||||

| Balance, beginning of period | $ | 6 | $ | 9 | |||

| Reclassification of derivative gains to net income | (1 | ) | (1 | ) | |||

| Balance, end of period | $ | 5 | $ | 8 | |||

| Shareholders’ capital | |||||||

| Balance, beginning of period | $ | 2,674 | $ | 2,673 | |||

| Issuance of shares | 1 | 1 | |||||

| Balance, end of period | $ | 2,675 | $ | 2,674 | |||

| Contributed surplus | |||||||

| Balance, beginning of period | $ | 12 | $ | 10 | |||

| Share-based compensation | 1 | 1 | |||||

| Balance, end of period | 13 | 11 | |||||

| Total Shareholders’ equity | $ | 4,759 | $ | 4,537 | |||

| See Notes to Unaudited Consolidated Financial Statements | |||||||

| Consolidated Balance Sheets | |||||

| (unaudited) | |||||

| March 31 | December 31 | ||||

| As at (millions of Canadian dollars) | 2014 | 2013 | |||

| Assets | |||||

| Current assets | |||||

| Cash and cash equivalents | $ | 292 | $ | 806 | |

| Accounts receivable | 423 | 369 | |||

| Inventories | 173 | 163 | |||

| Prepaid expenses | 5 | 8 | |||

| $ | 893 | $ | 1,346 | ||

| Property, plant and equipment, net (Note 4) | 8,836 | 8,712 | |||

| Exploration and evaluation | 54 | 54 | |||

| Reclamation trust | 81 | 78 | |||

| $ | 9,864 | $ | 10,190 | ||

| Liabilities and Shareholders’ Equity | |||||

| Current liabilities | |||||

| Accounts payable and accrued liabilities (Note 5) | $ | 644 | $ | 786 | |

| Current portion of employee future benefits (Note 6) | 42 | 82 | |||

| Current taxes | – | 259 | |||

| $ | 686 | $ | 1,127 | ||

| Long-term debt | 1,665 | 1,602 | |||

| Deferred taxes | 1,559 | 1,535 | |||

| Employee future benefits (Note 6) | 219 | 226 | |||

| Asset retirement obligation (Note 7) | 894 | 868 | |||

| Other liabilities (Note 8) | 82 | 100 | |||

| $ | 5,105 | $ | 5,458 | ||

| Shareholders’ equity | 4,759 | 4,732 | |||

| $ | 9,864 | $ | 10,190 | ||

| Commitments (Note 14) | |||||

| See Notes to Unaudited Consolidated Financial Statements | |||||

| Consolidated Statements of Cash Flows | |||||||

| (unaudited) | |||||||

| Three Months Ended March 31 | |||||||

| (millions of Canadian dollars) | 2014 | 2013 | |||||

| Cash from (used in) operating activities | |||||||

| Net income | $ | 172 | $ | 177 | |||

| Adjustments to reconcile net income to cash flow from operations: | |||||||

| Depreciation and depletion | 129 | 122 | |||||

| Accretion of asset retirement obligation (Note 7) | 7 | 6 | |||||

| Foreign exchange loss on long-term debt (Note 9) | 63 | 37 | |||||

| Deferred taxes (Note 11) | 15 | (22 | ) | ||||

| Share-based compensation | 4 | 2 | |||||

| Reclamation expenditures (Note 7) | (17 | ) | (33 | ) | |||

| Change in employee future benefits and other | (16 | ) | (14 | ) | |||

| Cash flow from operations | $ | 357 | $ | 275 | |||

| Change in non-cash working capital (Note 15) | (479 | ) | 54 | ||||

| Cash from (used in) operating activities | $ | (122 | ) | $ | 329 | ||

| Cash from (used in) financing activities | |||||||

| Issuance of shares | $ | 1 | $ | – | |||

| Dividends | (170 | ) | (170 | ) | |||

| Cash used in financing activities | $ | (169 | ) | $ | (170 | ) | |

| Cash from (used in) investing activities | |||||||

| Capital expenditures (Note 4) | $ | (217 | ) | $ | (268 | ) | |

| Reclamation trust funding | (3 | ) | (2 | ) | |||

| Change in non-cash working capital (Note 15) | (3 | ) | 23 | ||||

| Cash used in investing activities | $ | (223 | ) | $ | (247 | ) | |

| Foreign exchange gain on cash and cash | |||||||

| equivalents held in foreign currency | $ | – | $ | 6 | |||

| Decrease in cash and cash equivalents | $ | (514 | ) | $ | (82 | ) | |

| Cash and cash equivalents, beginning of period | 806 | 1,553 | |||||

| Cash and cash equivalents, end of period | $ | 292 | $ | 1,471 | |||

| Cash and cash equivalents consist of: | |||||||

| Cash | $ | 170 | $ | 758 | |||

| Short-term investments | 122 | 713 | |||||

| $ | 292 | $ | 1,471 | ||||

| Supplementary Information (Note 15) | |||||||

| See Notes to Unaudited Consolidated Financial Statements | |||||||

Notes to Unaudited Consolidated Financial Statements

For the Three Months Ended March 31, 2014

(Tabular amounts expressed in millions of Canadian dollars, except where otherwise noted)

1) Nature of Operations

Canadian Oil Sands Limited (“Canadian Oil Sands” or the “Corporation”) is incorporated under the laws of the Province of Alberta, Canada. The Corporation indirectly owns a 36.74 per cent interest (“Working Interest”) in the Syncrude Joint Venture (“Syncrude”). Syncrude is involved in the mining and upgrading of bitumen from oil sands near Fort McMurray in northern Alberta. The Syncrude Project is comprised of open-pit oil sands mines, utilities plants, bitumen extraction plants and an upgrading complex that processes bitumen into Synthetic Crude Oil (“SCO”). Syncrude is jointly controlled by seven owners and each owner takes its proportionate share of production in kind, and funds its share of Syncrude’s operating, development and capital costs on a daily basis. The Corporation also indirectly owns 36.74 per cent of the issued and outstanding shares of Syncrude Canada Ltd. (“Syncrude Canada”). Syncrude Canada operates Syncrude on behalf of the owners and is responsible for selecting, compensating, directing and controlling Syncrude’s employees, and for administering all related employment benefits and obligations. The Corporation’s investment in Syncrude and Syncrude Canada represents its only producing asset.

The Corporation’s office is located at the following address: 2000 First Canadian Centre, 350 – 7th Avenue S.W., Calgary, Alberta, Canada T2P 3N9.

2) Basis of Presentation

These unaudited interim consolidated financial statements are prepared and reported in Canadian dollars in accordance with Canadian generally accepted accounting principles as set out in Part 1 of the Chartered Professional Accountants of Canada Handbook and in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and effective on April 30, 2014.

Certain disclosures that are normally required to be included in the notes to the annual audited consolidated financial statements have been condensed or omitted as permitted by International Accounting Standard (“IAS”) 34, Interim Financial Reporting. These unaudited interim consolidated financial statements should be read in conjunction with the Corporation’s audited consolidated financial statements and notes thereto for the year ended December 31, 2013.

3) Accounting Policies

The same accounting policies and methods of computation are followed in these unaudited interim consolidated financial statements as compared with the most recent audited annual consolidated financial statements for the year ended December 31, 2013 except as follows:

Taxes

Current taxes in interim periods are accrued based on our best estimate of the annual effective tax rate applied to year-to-date earnings. Current taxes accrued in one interim period may be adjusted prospectively in a subsequent interim period if the estimate of the annual effective tax rate changes.

Impairment

In January 2013, the IASB issued amendments to IAS 36, Impairment of Assets, which removed fair value guidance from the standard to ensure consistency with the enhanced fair value measurement and disclosure requirements provided under IFRS 13, Fair Value Measurements. Canadian Oil Sands has applied these amendments effective January 1, 2014 in accordance with the applicable transitional provisions, with no impact on the financial statements or disclosures.

Levies

In May 2013, the IASB issued International Financial Reporting Interpretations Committee (“IFRIC”) Interpretation 21, Levies, which provides guidance on when to recognize a liability for levies imposed by governments. Canadian Oil Sands has applied this interpretation effective January 1, 2014, in accordance with the applicable transitional provisions, with no impact on the financial statements or disclosures.

4) Property, Plant and Equipment, Net

| Three Months Ended March 31, 2014 | |||||||||||||||||||||||

| Upgrading | Vehicles | Asset | Major | ||||||||||||||||||||

| and | Mining | and | Retirement | Turnaround | Construction | Mine | |||||||||||||||||

| ($ millions) | Extracting | Equipment | Equipment | Buildings | Costs | Costs | in Progress | Development | Total | ||||||||||||||

| Cost | |||||||||||||||||||||||

| Balance at January 1, 2014 | $ | 5,508 | $ | 1,941 | $ | 695 | $ | 345 | $ | 851 | $ | 174 | $ | 1,647 | $ | 678 | $ | 11,839 | |||||

| Additions | – | – | 9 | – | – | 3 | 205 | – | 217 | ||||||||||||||

| Change in asset retirement costs | – | – | – | – | 36 | – | – | – | 36 | ||||||||||||||

| Retirements | (4 | ) | (16 | ) | (23 | ) | – | – | – | – | – | (43 | ) | ||||||||||

| Reclassifications1 | 16 | 6 | – | – | – | – | (22 | ) | – | – | |||||||||||||

| Balance at March 31, 2014 | $ | 5,520 | $ | 1,931 | $ | 681 | $ | 345 | $ | 887 | $ | 177 | $ | 1,830 | $ | 678 | $ | 12,049 | |||||

| Accumulated depreciation | |||||||||||||||||||||||

| Balance at January 1, 2014 | $ | 1,626 | $ | 601 | $ | 349 | $ | 115 | $ | 223 | $ | 86 | $ | – | $ | 127 | $ | 3,127 | |||||

| Depreciation | 49 | 33 | 14 | 2 | 11 | 17 | – | 3 | 129 | ||||||||||||||

| Retirements | (4 | ) | (16 | ) | (23 | ) | – | – | – | – | – | (43 | ) | ||||||||||

| Reclassifications1 | – | – | – | – | – | – | – | – | – | ||||||||||||||

| Balance at March 31, 2014 | $ | 1,671 | $ | 618 | $ | 340 | $ | 117 | $ | 234 | $ | 103 | $ | – | $ | 130 | $ | 3,213 | |||||

| Net book value at | |||||||||||||||||||||||

| March 31, 2014 | $ | 3,849 | $ | 1,313 | $ | 341 | $ | 228 | $ | 653 | $ | 74 | $ | 1,830 | $ | 548 | $ | 8,836 | |||||

| 1 Reclassifications are primarily transfers from construction in progress to other categories of property, plant and equipment when construction is completed and assets are available for use. | |||||||||||||||||||||||

For the three months ended March 31, 2014, interest costs of $24 million were capitalized and included in property, plant and equipment (three months ended March 31, 2013 – $23 million) based on an interest capitalization rate of 6.6 per cent for the three months ended March 31, 2014 (6.5 per cent for the three months ended March 31, 2013).

5) Accounts Payable and Accrued Liabilities

| March 31 | December 31 | |||||

| ($ millions) | 2014 | 2013 | ||||

| Trade payables | $ | 528 | $ | 491 | ||

| Crown royalties | 137 | 334 | ||||

| Current portion of asset retirement obligation | 28 | 28 | ||||

| Interest payable | 18 | 23 | ||||

| $ | 711 | $ | 876 | |||

| Less non-current portion of Crown royalties | (67 | ) | (90 | ) | ||

| Accounts payable and accrued liabilities | $ | 644 | $ | 786 | ||

6) Employee Future Benefits

The Corporation’s 36.74 per cent share of Syncrude Canada’s obligation for pension and other post-employment benefits in excess of the fair value of the assets held in the benefit plans (the “accrued benefit liability”) is as follows:

| Three Months | Year | |||||

| Ended | Ended | |||||

| March 31 | December 31 | |||||

| ($ millions) | 2014 | 2013 | ||||

| Accrued benefit liability, beginning of period | $ | 308 | $ | 438 | ||

| Current service cost1 | 11 | 45 | ||||

| Interest expense2 | 3 | 16 | ||||

| Contributions | (28 | ) | (109 | ) | ||

| Re-measurement (gains) losses3: | ||||||

| Actual return on plan assets in excess of estimated return4 | (33 | ) | (46 | ) | ||

| Increase in discount rate | – | (91 | ) | |||

| Other5 | – | 55 | ||||

| Accrued benefit liability, end of period | $ | 261 | $ | 308 | ||

| Less current portion | (42 | ) | (82 | ) | ||

| Non-current portion | $ | 219 | $ | 226 | ||

| 1 Current service cost is recognized in net income as operating expense. | ||||||

| 2 Interest expense is net of estimated return on plan assets and is recognized in net income as net finance expense. | ||||||

| 3 Re-measurement (gains) losses are recognized, net of taxes, in other comprehensive income (loss). | ||||||

| 4 Estimated return is based on prescribed 4.5 per cent annualized rate. | ||||||

| 5 The other re-measurement loss in 2013 reflects an increase in the estimated average lifespan of the plans’ beneficiaries as a result of new actuarial standards. | ||||||

7) Asset Retirement Obligation

The Corporation and each of the other Syncrude owners are liable for their share of ongoing obligations related to the reclamation and closure of the Syncrude properties on abandonment. The Corporation estimates reclamation and closure expenditures on disturbed mines and existing facilities will be made progressively over the next 70 years and has applied a risk-free interest rate of 3.0 per cent at March 31, 2014 (December 31, 2013 – 3.25 per cent) in deriving the asset retirement obligation.

| Three Months | Year | |||||

| Ended | Ended | |||||

| March 31 | December 31 | |||||

| ($ millions) | 2014 | 2013 | ||||

| Asset retirement obligation, beginning of period | $ | 896 | $ | 1,102 | ||

| (Increase) decrease in risk-free interest rate | 50 | (217 | ) | |||

| Reclamation expenditures | (17 | ) | (42 | ) | ||

| Increase (decrease) in estimated reclamation and closure expenditures | (14 | ) | 27 | |||

| Accretion expense | 7 | 26 | ||||

| Asset retirement obligation, end of period | $ | 922 | $ | 896 | ||

| Less current portion | (28 | ) | (28 | ) | ||

| Non-current portion | $ | 894 | $ | 868 | ||

8) Other Liabilities

| March 31 | December 31 | |||

| ($ millions) | 2014 | 2013 | ||

| Non-current portion of Crown royalties1 | $ | 67 | $ | 90 |

| Other | 15 | 10 | ||

| Other liabilities | $ | 82 | $ | 100 |

| 1 Transition royalties due under Syncrude’s Royalty Amending Agreement. | ||||

9) Foreign Exchange

| Three Months Ended March 31 | ||||||

| ($ millions) | 2014 | 2013 | ||||

| Foreign exchange loss – long-term debt | $ | 63 | $ | 37 | ||

| Foreign exchange gain – other | (9 | ) | (9 | ) | ||

| Total foreign exchange loss | $ | 54 | $ | 28 | ||

10) Net Finance Expense

| Three Months Ended March 31 | |||||||

| ($ millions) | 2014 | 2013 | |||||

| Interest costs on long-term debt | $ | 30 | $ | 31 | |||

| Less capitalized interest on long-term debt | (24 | ) | (23 | ) | |||

| Interest expense on long-term debt | $ | 6 | $ | 8 | |||

| Interest expense on employee future benefits | 3 | 4 | |||||

| Accretion of asset retirement obligation | 7 | 6 | |||||

| Interest income | (2 | ) | (5 | ) | |||

| Net finance expense | $ | 14 | $ | 13 | |||

11) Tax Expense

| Three Months Ended March 31 | |||||

| ($ millions) | 2014 | 2013 | |||

| Current tax expense | $ | 60 | $ | 90 | |

| Deferred tax expense (recovery) | 15 | (22 | ) | ||

| Total tax expense | $ | 75 | $ | 68 | |

12) Capital Management

The Corporation’s capital consists of cash and cash equivalents, debt and Shareholders’ equity. The balance of each of these items at March 31, 2014 and December 31, 2013 was as follows:

| March 31 | December 31 | |||||

| As at ($ millions, except % amounts) | 2014 | 2013 | ||||

| Long-term debt1 | $ | 1,665 | $ | 1,602 | ||

| Cash and cash equivalents1 | (292 | ) | (806 | ) | ||

| Net debt2,3 | $ | 1,373 | $ | 796 | ||

| Shareholders’ equity1 | $ | 4,759 | $ | 4,732 | ||

| Total net capitalization2,4 | $ | 6,132 | $ | 5,528 | ||

| Total capitalization2,5 | $ | 6,424 | $ | 6,334 | ||

| Net debt-to-total net capitalization2,6 (%) | 22 | 14 | ||||

| Long-term debt-to-total capitalization2,7 (%) | 26 | 25 | ||||

| 1 As reported in the Consolidated Balance Sheets. | ||||||

| 2 Additional GAAP financial measure. | ||||||

| 3 Long-term debt less cash and cash equivalents. | ||||||

| 4 Net debt plus Shareholders’ equity. | ||||||

| 5 Long-term debt plus Shareholders’ equity. | ||||||

| 6 Net debt divided by total net capitalization. | ||||||

| 7 Long-term debt divided by total capitalization. | ||||||

Net debt, which is comprised of long-term debt less cash and cash equivalents, rose $577 million to $1,373 million at March 31, 2014 as cash balances were used to settle existing liabilities of approximately $500 million for Crown royalties and taxes, while a weakening Canadian dollar increased the carrying value of our long-term debt by $63 million. Cash flow from operations was almost sufficient to fund first quarter capital expenditures of $217 million and dividends of $170 million. As a result, net debt-to-total net capitalization increased to 22 per cent at March 31, 2014 from 14 per cent at December 31, 2013.

Shareholders’ equity increased to $4,759 million at March 31, 2014 from $4,732 million at December 31, 2013, as comprehensive income exceeded dividends in the first quarter of 2014.

The Corporation’s senior notes indentures and credit facility agreements contain certain covenants which restrict Canadian Oil Sands’ ability to sell all or substantially all of its assets or change the nature of its business, and limit long-term debt-to-total capitalization to 55 per cent. Canadian Oil Sands is in compliance with its debt covenants, and with a long-term debt-to-total capitalization of 26 per cent at March 31, 2014, a significant increase in debt or decrease in equity would be required to negatively impact the Corporation’s financial flexibility.

13) Financial Instruments

The Corporation’s financial instruments include cash and cash equivalents, accounts receivable, investments held in

a reclamation trust, accounts payable and accrued liabilities, and current and non-current portions of long-term debt. The nature, the Corporation’s use of, and the risks associated with these instruments are unchanged from December 31, 2013.

Offsetting Financial Assets and Financial Liabilities

The carrying values of accounts receivable and accounts payable and accrued liabilities have each been reduced by $74 million ($49 million at December 31, 2013) as a result of netting agreements with counterparties.

Fair Values

The fair values of cash and cash equivalents, accounts receivable, reclamation trust investments and accounts payable and accrued liabilities approximate their carrying values due to the short-term nature of those instruments. The following fair values of long-term debt are based on Level 2 inputs to fair value measurement, which represent indicative bids or spreads for a round lot transaction within the relevant market:

| March 31 | December 31 | |||

| As at ($ millions) | 2014 | 2013 | ||

| 8.2% Senior Notes due April 1, 2027 (U.S. $73.95 million) | $ | 103 | $ | 95 |

| 7.9% Senior Notes due September 1, 2021 (U.S. $250 million) | 341 | 321 | ||

| 6.0% Senior Notes due April 1, 2042 (U.S. $300 million) | 369 | 323 | ||

| 4.5% Senior Notes due April 1, 2022 (U.S. $400 million) | 455 | 425 | ||

| 7.75% Senior Notes due May 15, 2019 (U.S. $500 million) | 670 | 636 | ||

| $ | 1,938 | $ | 1,800 | |

14) Commitments

Canadian Oil Sands’ commitments are summarized in the 2013 annual consolidated financial statements and include future cash payments under contractual arrangements that it has entered into either directly or as a 36.74 per cent owner in Syncrude. During 2014, Canadian Oil Sands assumed $75 million in new funding commitments relating to capital projects while the Corporation’s share of payments prescribed by regulations on Syncrude Canada’s registered pension plans decreased by approximately $200 million as a result of an actuarial valuation completed in April, 2014.

15) Supplementary Information

a) Change in Non-Cash Working Capital

| Three Months Ended March 31 | |||||||

| ($ millions) | 2014 | 2013 | |||||

| Operating activities: | |||||||

| Accounts receivable | $ | (54 | ) | $ | (4 | ) | |

| Inventories | (10 | ) | (23 | ) | |||

| Prepaid expenses | 3 | 3 | |||||

| Accounts payable and accrued liabilities (“AP”) | (142 | ) | 55 | ||||

| Current taxes | (259 | ) | 46 | ||||

| Other | (20 | ) | – | ||||

| AP changes reclassified to investing activities | 3 | (23 | ) | ||||

| Change in operating non-cash working capital | $ | (479 | ) | $ | 54 | ||

| Investing activities: | |||||||

| Accounts payable and accrued liabilities | $ | (3 | ) | $ | 23 | ||

| Change in investing non-cash working capital | $ | (3 | ) | $ | 23 | ||

| Change in total non-cash working capital | $ | (482 | ) | $ | 77 | ||

b) Income Taxes and Interest Paid

| Three Months Ended March 31 | ||||

| ($ millions) | 2014 | 2013 | ||

| Income taxes paid | $ | 338 | $ | 44 |

| Interest paid | $ | 35 | $ | 20 |

Income taxes paid and the portion of interest costs that is expensed are included within cash from operating activities on the Consolidated Statements of Cash Flows. The portion of interest costs that is capitalized as property, plant and equipment is included within cash used in investing activities on the Consolidated Statements of Cash Flows.

c) Cash Flow from Operations per Share

| Three Months Ended March 31 | ||||

| ($ millions) | 2014 | 2013 | ||

| Cash Flow From Operations Per Share, basic and diluted | $ | 0.74 | $ | 0.57 |

Cash flow from operations per Share is calculated as cash flow from operations, which is cash from operating activities before changes in non-cash working capital, divided by the weighted-average number of outstanding Shares in the period.

Canadian Oil Sands Limited

Ryan Kubik, President & Chief Executive Officer

Shares Listed – Symbol: COS Toronto Stock Exchange

Canadian Oil Sands Limited

Siren Fisekci

Vice President, Investor & Corporation Relations

(403) 218-6228

Canadian Oil Sands Limited

Scott Arnold

Director, Sustainability & External Relations

(403) 218-6206

Canadian Oil Sands Limited

2000 First Canadian Centre

350 – 7 Avenue S.W., Calgary, Alberta T2P 3N9

(403) 218-6200

(403) 218-6201 (FAX)

invest@cdnoilsands.com

www.cdnoilsands.com

{kind=link}