In January 2016 the Alberta Government adopted the recommendations proposed by the Royalty Review Advisory Panel in their report entitled “Alberta at a Crossroads”. This report is the basis of the Modernized Royalty Framework (“MRF”). Understanding it is critical for production companies, investors and creditors, as royalties are a key component in the determination of value for year-end reserves, acquisitions and divestitures.

As an independent reserves certification specialist, Sproule provided a summary of the new framework in January and with the updates this April, specifically on the royalty formulas, Sproule is again outlining the changes in an easy to understand manner.

It is critical for Sproule to understand the new royalty costs associated with hydrocarbon development in Alberta, as it will impact the values estimated by Sproule for year-end reporting effective December 31, 2016, and for anyone else valuing potential investment opportunities from this point forward. The April 21, 2016 update provided insight into the formulas used for calculating royalties under the MRF, however, it does not contain all of the information necessary to fully derive royalties payable. Additional information is set to be released May 31, 2016 and Sproule is already working to roll out sensitivity analyses to better understand implications.

Summary of Formulas

MRF for Oil and Natural Gas Wells

For all wells spudded prior to January 1, 2017 the existing royalty framework will continue to apply, including incentives from the Natural Gas Deep Drilling Program. Royalties payable on these wells will be based on the existing royalty structure until January 1, 2027, at which time they will convert to the MRF.

All wells spudded after the implementation date of January 1, 2017 (“MRF Wells”) will be subject to royalties determined under the MRF. There will be one royalty structure for all wells regardless of whether they are considered an oil well or a gas well.

The MRF is designed to implement unique royalty formulas for three distinct phases of production life. In general, the MRF is designed to provide a low royalty until payout, followed by a sharing of profits after payout, followed by a lessening of royalties at lower production levels to promote the extended life of wells. The current royalty system provides incentive programs with a low royalty until the incentives payout. The MRF retains the concept of low royalties in the early life of a well, but with an alternative program. The time to payout under the old system relative to the time to payout under the MRF is a comparative we are investigating. Preliminary research indicates a shift to shorter payout times under the MRF.

Early Life (Pre-C*) – Flat royalty rate of 5%

The flat rate of 5% will remain in place until cumulative revenue generated from the well exceeds the “Drilling and Completion Cost Allowance – C*.” This is called a Revenue Minus Cost (RMC) model. Operating costs are not included as a cost component, nor are equipping or gathering system costs.

C* (pronounced “C-star”) is determined based on a formula that considers the depth and length of the well drilled as well as the amount of proppant used in completing the well. C* will be unique for each well and will not change once the well is drilled and placed on production. It is recommended that the coefficients used in the determination of C* be calibrated every three to five years. Further, it is recommended that an Alberta Capital Cost Index (ACCI) be established and maintained to allow C* to float on an annual basis as industry costs change, with annual changes limited to plus or minus 5%. The ACCI would be announced on March 31 of each year for application effective April 1 of the same year. Companies will be obliged to report actual capital costs, along with other mandatory well information, to the AER to be used as statistical inputs to calculate the ACCI.

The formula for C* has been released as follows:

For wells with TVD less than or equal to 2000m:

C*($) = 1170*(TVD-249) + 800*(TLL) + 0.6*(TVD*TPP)

For wells with TVD greater than 2000m:

C*($) = 1170*(TVD-249) + 3120*(TVD-2000) + 800*(TLL) + 0.6*(TVD*TPP)

Where:

The Release states “Revenue from the well will be determined by multiplying volumes of the various hydrocarbons by their respective par prices published by Alberta Energy. For conventional oil this is produced volumes and for natural gas and by-products this is allocated volumes”. Sproule interprets this as meaning oil volumes will be taken as the volume publicly reported, while the raw gas volumes will be split into natural gas (methane), ethane, propane, butane, and pentane based on gas analyses. The details of how this is going to be done have not been released. Additionally, the Release does not make any mention of how Alberta Energy will be determining its par prices for each product.

At this time, there is no mention of a C* being assigned for recompletions, reactivations, or enhanced recovery schemes.

The MRF will apply to all conventional oil and natural gas wells outside the designated oil sands areas. Treatment for oil sands wells that pay royalties based on conventional oil formulas will be available on May 31, 2016.

Post-C* and Post-C* Mature

Royalty rates post-C* are determined using the formula:

R% = Price Component (rp) + Quantity Adjustment (rq)

The price component is based on par prices determined by Alberta Energy for the various hydrocarbon streams and is independent of production rates. The quantity adjustment only kicks in when hydrocarbon production drops below a certain rate, deemed the “Maturity Threshold”, at which time the royalty rate will be adjusted downward as production rates decline. The price component is determined for each hydrocarbon stream individually and adjusted (if the well has reached its Maturity Threshold) based on total oil equivalent production. The total royalty payable for a well is the sum of the royalty payable for each individual hydrocarbon stream.

A minimum royalty rate of 5% applies to all hydrocarbon products.

Conventional Oil, Pentanes Plus (Extracted and In-stream Component) and Field Condensate

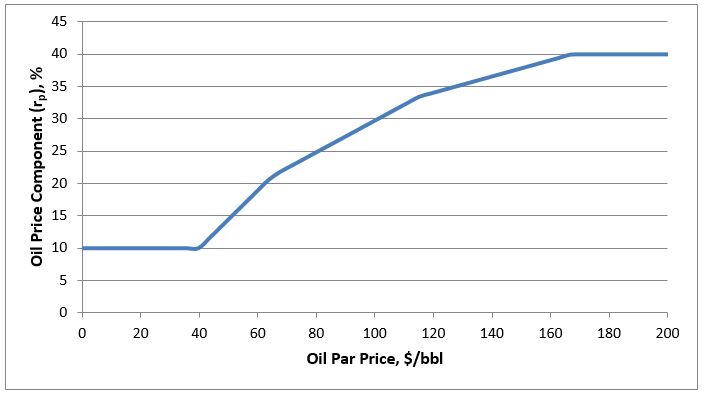

The price component of the conventional oil, pentanes plus and field condensate royalty has a minimum of 10% and a maximum of 40%. Actual formulas have been released on the Alberta Government’s website, but the price component versus par price is shown below.

Post-C* Relationship between Oil Royalty Price Component and Oil Price

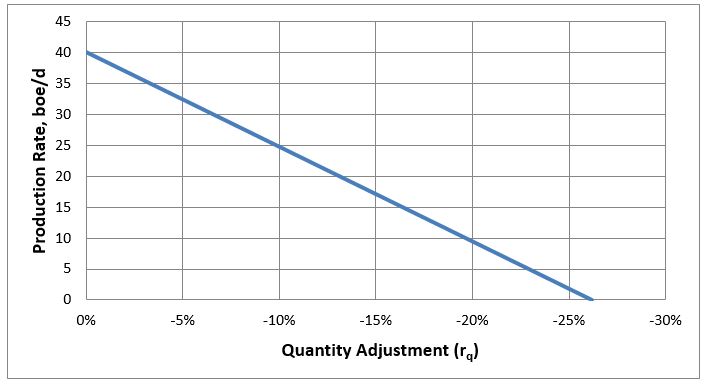

The quantity adjustment begins to apply at the Maturity Threshold of 40 boe/d (194 m3e/month), based on the following formula:

rp = (Q-194.0)*0.1350%

Where:

As the wells production continues to decline, the quantity adjustment increases, as shown in the graph below. The quantity adjustment can only reduce the royalty rate to the minimum royalty rate of 5%.

A few details are not yet clear with regards to this formula:

Post-C* Relationship between Quantity Adjustment and Production Rate

Natural Gas (Methane) and Ethane

The price component of the natural gas (methane) and ethane royalty has a minimum of 5% and a maximum of 36%. Actual formulas have been released on the Alberta Government’s website, but the price component versus par price is shown below.

Post-C* Relationship between Gas Royalty Price Component and Gas Price

The Release states “the treatment of the maturity threshold and quantity adjustment for natural gas will be similar to that for oil. Details are being finalized and will be available in the coming weeks”. Sproule interprets this to mean that the boe ratio (6:1, 10:1, or other) and the allocation of raw natural gas into its in-stream components have not yet been finalized.

Butane

The price component of the butane royalty has a minimum of 10% and a maximum of 36%. Actual formulas have been released on the Alberta Government’s website, but the price component versus par price is shown below.

Post-C* Relationship between Butane Royalty Price Component and Butane Price

The treatment of the maturity threshold is discussed above under Conventional Oil.

Propane

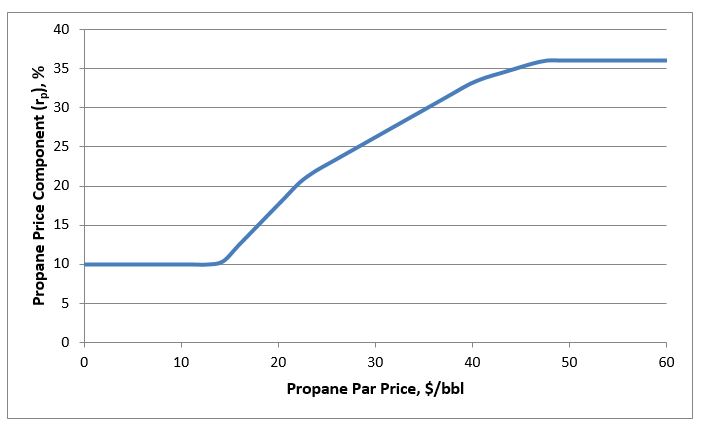

The price component of the propane royalty has a minimum of 10% and a maximum of 36%. Actual formulas have been released on the Alberta Government’s website, but the price component versus par price is shown below.

Post-C* Relationship between Propane Royalty Price Component and Propane Price

The treatment of the maturity threshold is discussed above under Conventional Oil.

Strategic Programs for Oil and Natural Gas Development

No additional information has been released since January 29, 2016. Additional information is set to be released on May 31, 2016.

Conclusions

Both the existing royalty framework and the MRF are extremely complicated systems, each with many variables used to calculate the royalty rate. In both systems, a pre-payout period exists with low royalty rates, followed by a post payout period, where the royalty rate is a function of prices, production rates, and hydrocarbon split. It continues to be necessary to look at each opportunity under specific price scenarios in order to determine the effect the MRF has on overall value.

While there are still uncertainties regarding the MRF formulas, we now have a better idea as to the formulas used. With these details, Sproule is able to estimate the impact the MRF will have on the value of opportunities, enabling more informed decisions around investment opportunities. There are still some unanswered questions: How will Alberta Energy determine its par prices? What boe ratio will be applied to gas volumes? How will the in-stream components be determined? How will oil sands wells that pay conventional oil royalties be treated? And, What new strategic programs will be announced?

Steven Golko is Vice President of Field Development & Capital Strategies at Sproule. He has been a partner since 2010 and has extensive experience in the Western Canadian Sedimentary Basin, offshore East Coast Canada, and the Eagleford and Williston basins in the United States. Steven leads a team responsible for helping clients with field development plans and capital strategies.

Contact Steven Golko at steven.golko@sproule.com or LinkedIn.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}