Despite the risk of sounding like an anti-shale lunatic, it’s important to counter the fan-boy mentality that’s gripped the media and swept away the common sense of analysts and commentators who might possibly know better. Any discussion about potential future global production shortfalls is dismissed with a hand wave and the ubiquitous “shale production will fill the void” nonsense. The same phenomenon existed 25 years ago with the “call on OPEC”, where it was universal knowledge that OPEC could produce whatever it wanted whenever it wanted. That wasn’t true, and neither is the perception that shale resources are wiping out OPEC or whatever gibberish you come across.

It is worth stating that shale reservoirs are wonderful reservoirs, and have indeed been hugely significant in global oil and gas production. New technology has unlocked a lot of hydrocarbons that weren’t on the production radar 20 years ago. A resource that can double US production in 5-7 years is certainly notable.

But shale resources are, from a global perspective, just one of many important sources that has had a moment in the spotlight. At some stage of development, every major field in the world has been touted as the Next Big Thing – Kazakhstan, Brazil, Canadian oil sands, the North Sea, Iraq post-Saddam, etc. Ordinarily I’d say who cares, because what the pundits think should be of little concern. But people believe the hype, and run out to trade in hybrids for Escalades, and no one is prepared for a world of potentially higher prices. To even acknowledge that is possible is like showing your membership card for the Flat Earth Society. I recently had an unfortunate conversation with a media market analyst who explained how prices wouldn’t rise much above $60/barrel for the foreseeable future because “capital markets have short memories” and capital will flood back in, and shale output will cover any global shortfall. But it won’t. Output will surely increase, but shale products aren’t going to save the world for a few reasons, neither of which is overly complicated.

First is scale. The world needs to add 4.5 million b/d to replace natural declines at a 5 percent decline rate, and with no development capital presently available the decline rate is probably more like 10 percent or 9 million barrels per day. The entire US shale revolution added less than 5 million barrels per day, over 6 years and at a cost of something like $500 billion, and much of this capital is being written off as we speak. So after years of drilling up sweet spots and half a trillion dollars, how easily will the US add another 5 million b/d, particularly when US output is in freefall now? How much capital would be required to keep production flat and double production?

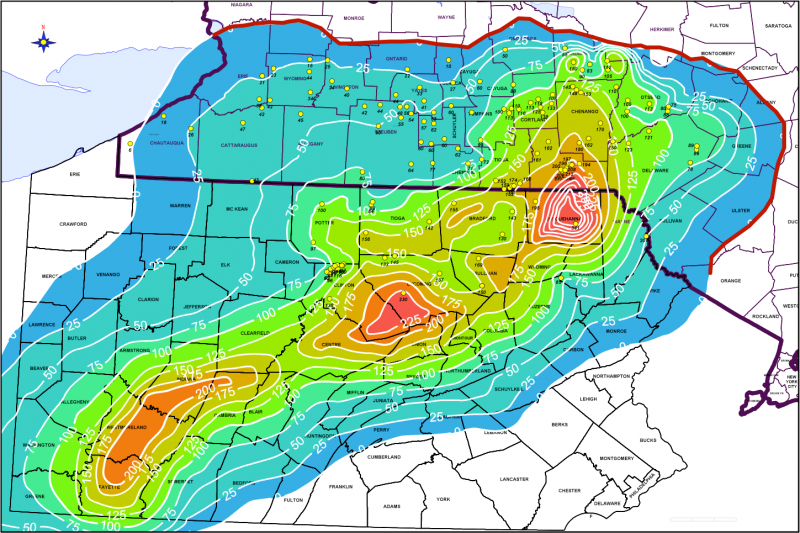

And speaking of sweet spots… Here’s where the prevalent simple-minded group-think totally misses a very big point. Shale regions (like most formations) are far from homogenous. There is tremendous variability in quality, thickness, porosity, permeability, etc. Producers find this out eventually, and development happens in the best spots, where economics are best. Sometimes the hinterlands become economic with new technology, but mostly they only get there through much higher prices. Here are a few maps showing development of the Marcellus region (I know this is gas, but the same phenomenon happens for oil and these maps were prettier).

This chart is from 2011:

And here is an update from 2015:

A look at the estimated thickness of the shale zone shows what producers are after, and where the good stuff is and is not:

Does this look like the key building block that will make the US “the New Epicenter of Energy in the World“? It’s huge, but let’s be realistic. As the play developed, tests were conducted all over, and eventually almost all activity shifted to the sweet spots. This isn’t unique to shale, it happens in every play, oil or gas, as it develops. The point is then that the resource is not infinite, not remotely close, and the results (and mania) achieved thus far won’t be sustained indefinitely. The next time someone talks about the potential of the Marcellus, keep these pictures in mind. There may still be a lot of drilling to go in the sweet spots, and some are still not fully understood, but the best spots are obviously pretty well mapped out. Future development will have to be outside these sweet spots at some point, with far less spectacular results. Almost all oil and gas formations exhibit similar development patterns.

Perhaps more critically, shale sweet spots are being developed with a scorched earth strategy. Actually “strategy” is exactly the wrong word because there is none. Ultra long horizontal wells (a company called Eclipse Energy recently drilled a well with a 3.5 mile lateral) are a one-shot, money-grab attempt to suck as much hydrocarbons out of the reservoir as fast as possible (next week’s post will examine two contrasting methodologies).

Would global oil output ever drop by 10 percent? It sounds crazy but not when we add up the trouble spots. Natural declines at the best of times (with plentiful capital) are maybe 3 percent or about 2.7 million b/d. With drilling capital being close to nonexistent (never mind zero exploratory capital), that rate could easily be 5-6 percent (4.5-5.5 million b/d) or more. Venezuela (2.7 million b/d) is about to implode; Nigeria, Libya and Iraq are in disarray; no major projects are being initiated, rig usage is at all time lows, and US production is falling by >100,000 b/d per month. Add all that up, and subtract the number of new discoveries being made (i.e., zero) and a massive shortfall should seem like a fairly reasonable expectation.

It’s possible to imagine a miracle where hundreds of billions flowed into shale production again, or any other hot new play, which might increase production substantially. But a doubling of shale production would take half a decade and countless billions, if even possible, and even then would barely offset a year of global natural declines. So when you read a story about how any recovery in oil prices will bring on a glut of shale oil and drive down production, which isn’t hard to find, before you take it seriously read through it and determine if the evidence is thorough and thoughtful, or just the latest round of group-think hyperbole.

Read more insightful analysis from Terry Etam here

{kind=link}

{kind=link}

{kind=link}

{kind=link}