Each week, XI Technologies scans its unique combination of enhanced industry data to provide trends and insights that have value for professionals doing business in the WCSB. If you’d like to receive our Wednesday Word to the Wise in your inbox, subscribe here.

When it comes to ESG reporting, most producers know to factor in their Asset Retirement Obligations (ARO) work. ARO touches on all three aspects of ESG, from the Environmental improvements of reclaiming land to the Social aspects of improved relations with landowners, indigenous communities, and government agencies, to the Governance matters associated with planning and reporting on ARO activities.

This is particularly true with the release of the new Directive 088 in Alberta. Much of the new required metrics on closure of inactive sites and performance are indicative of the critical role ARO plays in Governance. But when it comes to managing and proving performance on one’s potential liability, you can’t manage what you can’t measure.

When it comes to ARO and ESG, investors want to see a plan. They want to understand a company’s long-term liability management plan and receive credible, standardized information to support long-term risk assessments. And just as important as having a plan is the need to have a way to communicate your plan that gives investors the right information in the right format.

Evaluation of ARO components that could affect an ESG assessment of your company might include:

When reporting on ARO in an ESG report, it’s important to consider the metrics stakeholders, investors, and regulators desire – both what has been done and what will be done. To have a plan that meets the demands of ESG investors, look at what metrics you have, what you are measuring, what gaps you might need to fill, and how easily these measures can be reported to various stakeholders.

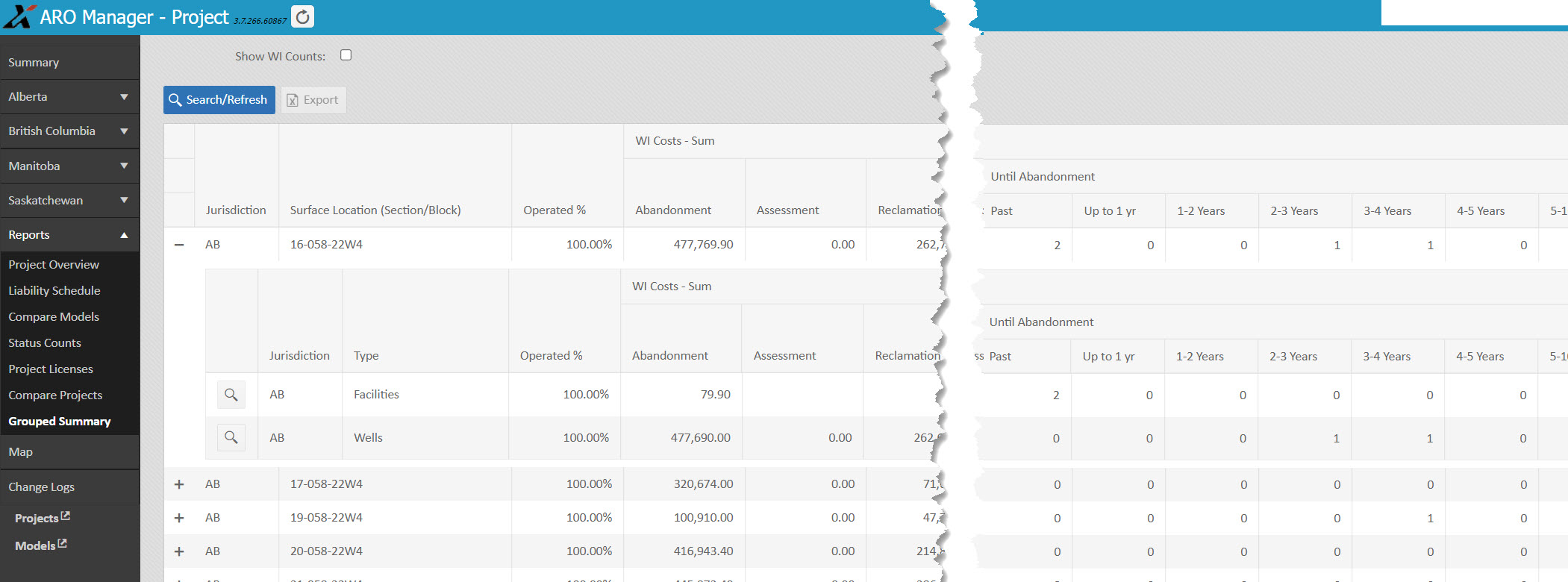

To learn how XI’s ARO Manager can help with the planning and reporting of liability management, visit our website or contact us for a demo. You can also read a case study on how ARO Manager helped a bank assess the potential liability impact of an acquisition for a client by reading our case study.

{kind=link}

{kind=link}