In Western Canada’s oil and gas sector, joint ventures are a common operating model. Multiple partners share ownership of wells, facilities, and infrastructure, with one party responsible for operating the asset and allocating costs to the remaining partners.

This partnership enables efficient development and risk sharing, but it also introduces a critical challenge: ensuring that joint venture accounting and cost allocations align with the contractual agreements.

For non-operating partners, this is not simply an administrative task, production accounting and joint interest billings (JIB’s) directly impact cash flow, profitability, and financial reporting. Even small discrepancies, when repeated over time, can accumulate meaningful financial impacts for an asset.

In practice, these billings are complex. Joint venture agreements, joint operating agreements, and land contracts define how costs should be shared, but interpretation and implementation by the operator are not always consistent. As a result, companies may unknowingly be paying costs that are not fully aligned with contractual obligations.

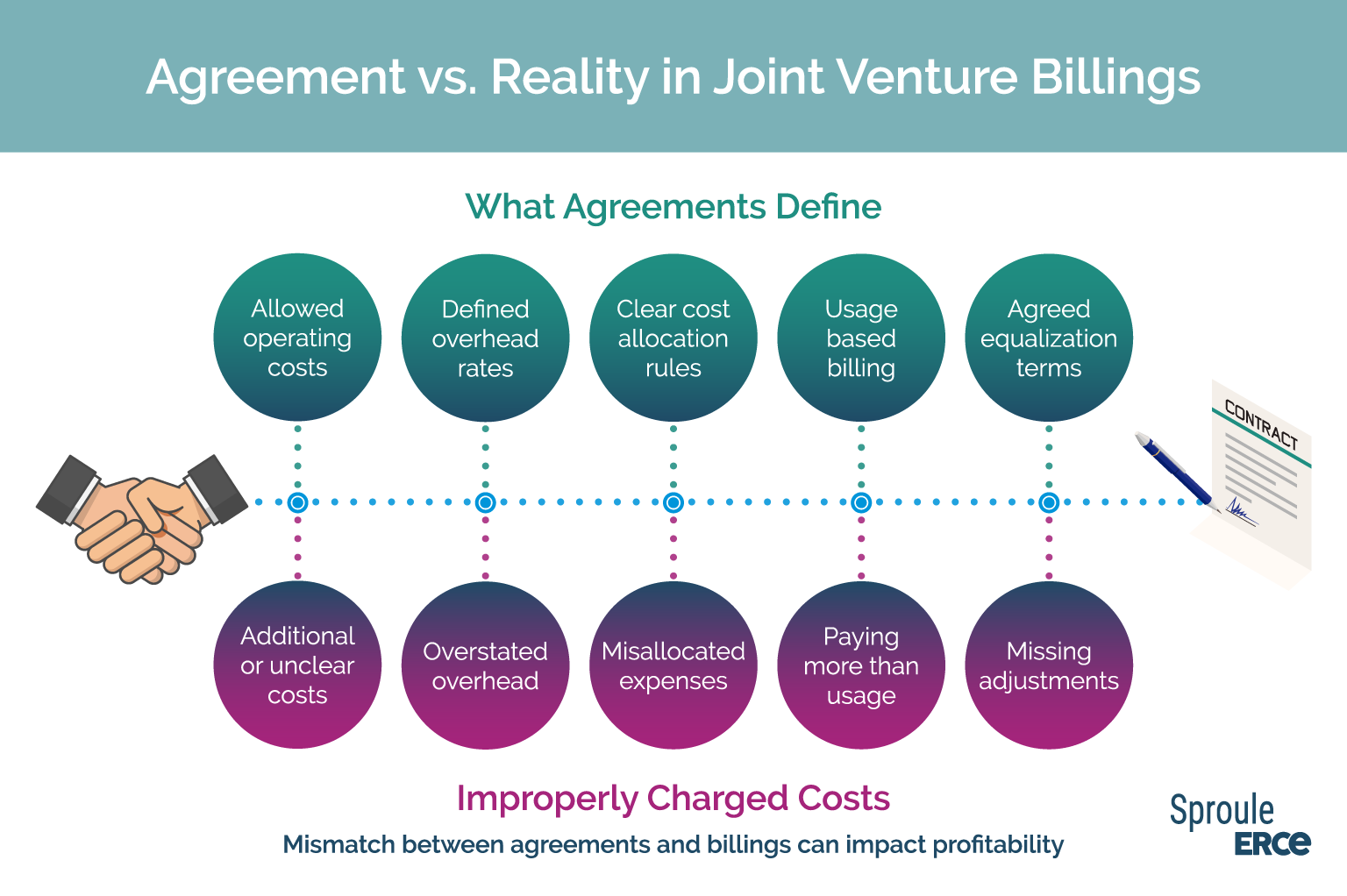

What Charges Are Contractually Allowed?

At the core of joint venture accounting is a simple principle: Partners should only be charged costs that are explicitly allowed under the governing agreements. However, applying this principle is rarely straightforward. A structured review begins with two key questions:

- What do the contractual agreements allow?

- What is actually being charged?

Differences between these two will reveal billing discrepancies, allocation errors, or misinterpretations that can impact profitability. Common areas where structured joint venture billing errors occur include:

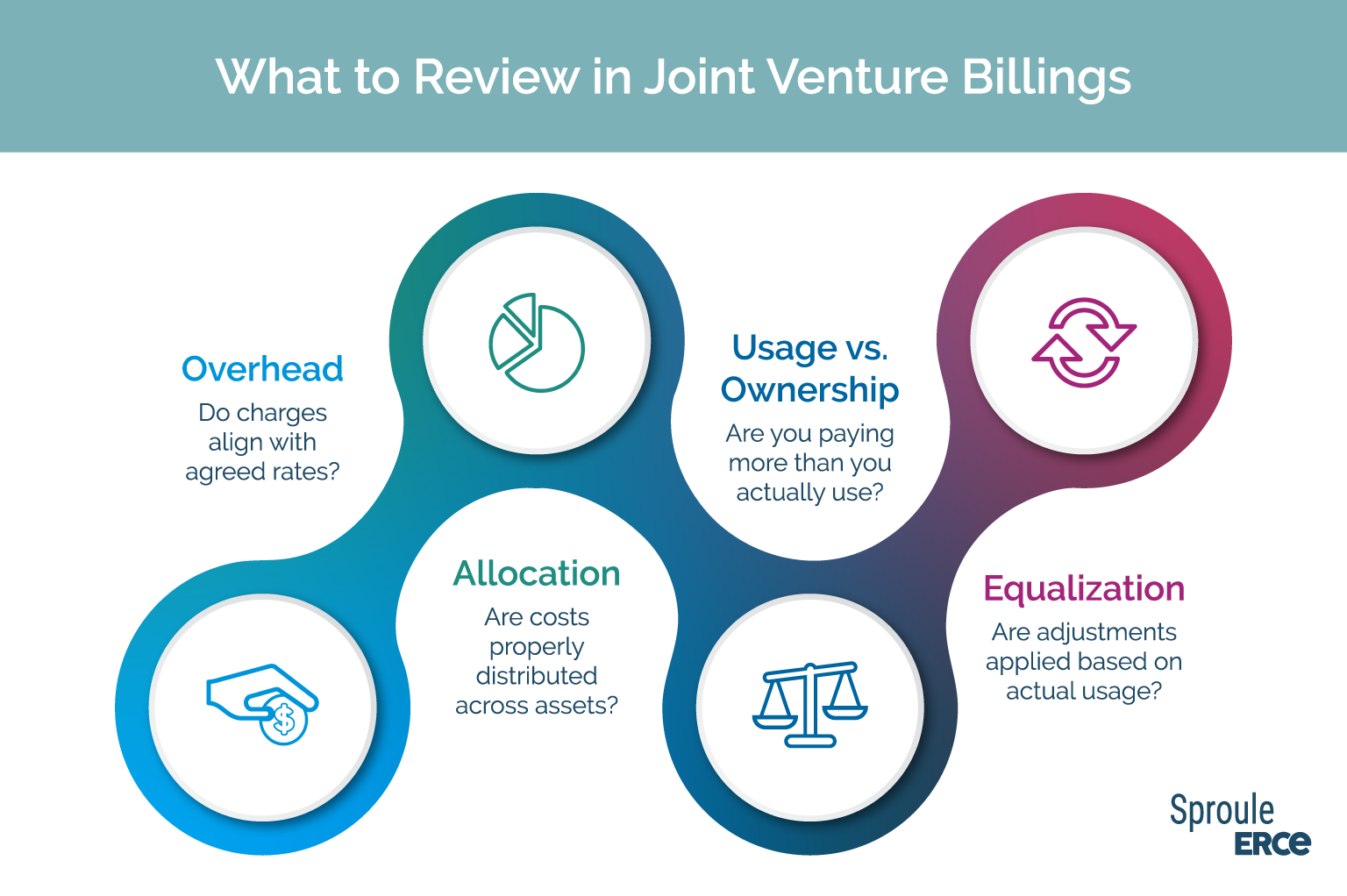

- Overhead and Administrative Charges: Joint venture agreements typically define how overhead is calculated. Inconsistencies in interpretation or application can result in charges that exceed what is permitted.

- Cost Allocation Across Assets or Fields: Operators allocate shared costs across wells, facilities, or operating areas. These allocations must reflect actual usage and operational activity. Misalignment can lead to disproportionate charges.

- Usage vs. Ownership Differences: Ownership percentages are often used to allocate costs, even when actual usage differs. For example, a partner may own 50% of a facility but only use a portion of its capacity. Without adjustment for throughput, this may result in inappropriate cost sharing.

Equalization and Thirteen-Month Adjustments

Many agreements include provisions to correct imbalances over time. If equalization processes are not applied consistently, discrepancies can accumulate. These processes can be complex, with some operators applying internal processes, instead of industry standards.

Evaluating What Matters

Not every discrepancy justifies detailed investigation. An effective review will prioritize material financial impact, frequency of the issue and cost-benefit of further analysis. This ensures that efforts are focused on areas that meaningfully affect the bottom line, rather than immaterial differences.

Sproule ERCE Perspective

A detailed review of joint venture accounting requires more than financial analysis. It requires an integrated team and understanding of operations, engineering, agreements, and accounting processes.

Sproule ERCE applies this integrated approach to evaluate the accuracy and completeness of production accounting data and joint interest billings in relation to contractual terms. A typical review includes:

- Analyzing applicable agreements including joint venture, land, and processing;

- Reviewing production accounting data and JIB’s;

- Reconciling charges to the contracts; and

- Identifying inconsistencies in allocation methodologies and billing practices.

This approach reflects real-world workflows where accounting outcomes are directly tied to operational and contractual obligations.

Efficiency Through Experience

Sproule ERCE brings multifunctional expertise across production and revenue accounting; joint venture structures and agreements; engineering and field operations; and regulatory and compliance. Our in-house team approach enables rapid identification of potential issues, starting with high-level screening and focusing on areas with the highest value impact.

Supporting Better Decision-Making

Beyond identifying discrepancies, the goal is to improve cost transparency, alignment with agreements, confidence in financial reporting and communication between partners. This allows non-operating partners to validate what they are being charged, understand how costs are allocated, and take informed action where necessary.

Conclusion

Joint venture accounting is inherently complex. It requires alignment between agreements, operational activity, and accounting processes. This alignment is not always achieved in practice. For non-operating partners, this creates both risk and opportunity. Risk, because inappropriate or misinterpreted charges can erode profitability over time and opportunity, because structured reviews can uncover inefficiencies and improve cost control.

The key takeaway is simple: Companies may be paying for costs they are not obligated to pay, and without proper review, those costs often go unnoticed. By applying a disciplined approach to joint venture accounting and billing validation, companies can protect cash flow, improve accuracy, limit liability, and strengthen financial performance.

In many cases, value is not lost through a single large issue, but through multiple small inconsistencies in billing and allocation practices accumulating over time.

Sproule ERCE Asset Management supports clients by providing the expertise needed to identify discrepancies, validate costs, resolve disputes and protect asset value.

This article is sponsored content, written and paid for by the advertiser. We do not endorse or take responsibility for the accuracy of the information presented. It has not been reviewed by our editorial team, and the opinions expressed are solely those of the sponsor.