Constructive dialogue is a necessary component for any discussion taking place on important issues. Be it the economy, an election, or foreign affairs: each warrants informed discussion at both the local and national level. The same can be said about Canada’s energy sector. With the oil and gas industry being such a fundamental player to the overall Canadian economy, the importance of said dialogue cannot be understated. That said, it should come as no surprise that the key to constructive dialogue taking place, is to start with a strong knowledge base.

CBC’s senior business correspondent, Amanda Lang, is one of the few people on television who’s job is to inform the general public of the economy and, as such, the oil and gas industry. There are very few people on TV who understand the oil and gas industry and the markets which drive it, and after discovering a comment from Amanda Lang on the price of a crude oil futures contract, it has become clear that she is not one of them.

Let me first start by explaining what a commodity (in this case crude oil) futures contract is: it is an agreement between two parties where one party agrees to buy a standardized amount of crude oil (1,000 barrels in this case) from another party for a specified price at a standardized date in the future.

So let’s say I sell one June 2016 crude oil futures contract at $45.00. What I am in effect doing is entering a contract whereby I will deliver 1,000 barrels of oil to the counterparty of the contract for $45 per barrel in June 2016. An important aspect of this agreement is that if, prior to June 2016, I buy one June 2016 futures contract, it will offset the contract that I had sold earlier, and my net position will return to zero (this is by far the most common scenario, very few futures contracts ever actually transition into deliveries).

So on the New York Mercantile Exchange, there are many crude oil futures contracts you can buy. In fact, there are multiple delivery months available to trade going out to around the year 2030. You can buy crude oil for delivery in October or November 2015 or in December 2020. The thing is, not a lot of people are trying to buy oil for delivery in 2020; most traders desire liquidity and will therefore trade the nearest few delivery months available. So when you look at the volume contracts traded on a futures delivery month, there typically isn’t a lot of exchanging going on…until the delivery time for that contract gets closer to the current date. Then lots of trades start happening!

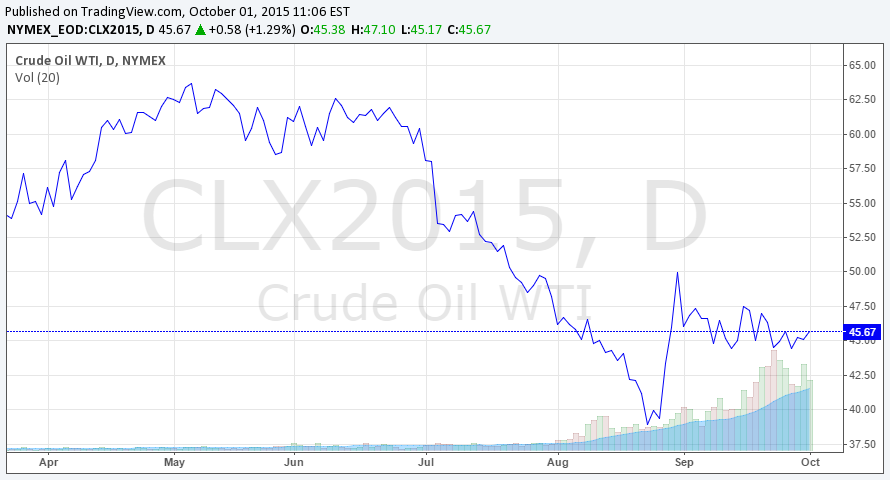

Have a look at this chart:

Notice the bars at the bottom of the chart. That’s the volume of contracts traded. The closer to the delivery date, the higher the volume. All commodity contracts follow this pattern, with almost no exceptions. In fact, it would be quite a story if the volumes of any particular contract did not follow this trend!

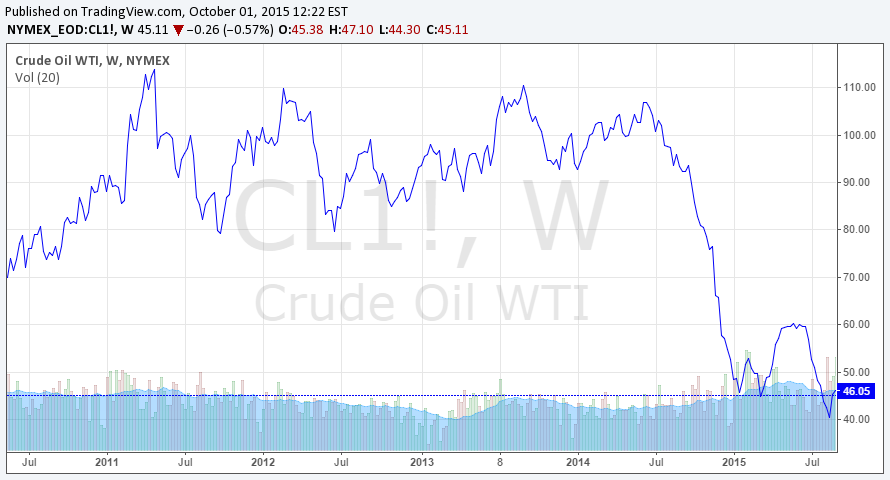

Now, sometimes you might notice charts like this…

…where you see lots of trades all the time. That is because it is a chart of the nearest month contract. The chart automatically changes the delivery month being plotted on the chart over time to display whatever the near-term contract is at any particular point in time.

Now that we have the basic knowledge of what a futures contract is, let’s have a look at what CBC’s top financial expert Amanda Lang tweeted a short while back:

She took the futures chart of one delivery month to analyze the volume of the historical volume that crude oil trades. As you’ll notice there is literally no volume until near the date of delivery. A proper analysis would be to look at the rolling chart of the nearest month I highlighted earlier.

So this demonstrates she has absolutely no clue what a futures contract is because she based the volume of crude oil trading on a single contract, which didn’t show anything of value in terms of volume at all.

Now you could say this was an innocent mistake…perhaps she accidentally pulled the wrong chart? Well, as you can see from the above chart of the rolling contract, there is very little change in crude oil trading volume in the past 5 years. It has not ‘soared’.

It’s troubling, to say the least, that a person with such a platform lacks the most basic understanding of the commodity markets. Especially when that person’s job is to inform a public whom is largely unfamiliar with the oil industry.