In the second quarter of 2016, a substantial recovery in crude prices has taken place, with both Brent and WTI prices rising from the mid-30s to the high 40s. It’s difficult to attribute this streak to any single reason, but we can certainly identify some of the contributing factors.

First, US Dollar weakness has boosted nearly all commodity prices worldwide, including energy prices. While it has recovered from its early-May low, the US Dollar has fallen about 4 percent against a basket of other global currencies since January. It was recently lower still but has been bolstered by “Brexit” and the associated uncertainty afflicting the Pound and Euro. For energy benchmarks denominated in non-USD currencies, price recoveries have tended to be slightly less pronounced due to the absence of similar currency tailwinds.

On the supply side, there have been significant disruptions around the world. Here in Alberta, the May wildfires in the Fort McMurray region led to a drop in crude production of over 1 MMbopd. In Nigeria, output is at the lowest level in decades due to terrorism and militancy in the Niger Delta, and is only operating at an estimated 50% of capability. Libya has experienced attacks at loading terminals, driving exports down, with production around a quarter of what it was just a few years ago. In Venezuela, pressure from the economic crisis has contributed to a modest drop in crude output as well, with some fearing the worst: if the crisis turns into a full meltdown, production could drop from nearly 3 MMbopd to almost zero. Despite the rocky quarter, supply disruptions appear to be easing somewhat, indicating we may be due for a minor near term price correction, but the significance of these disruptions in carrying crude prices up from last quarter’s lows is clear.

On the demand side, appetite from China and India has been healthier than many expected over the last quarter. Global refinery capacity is anticipated to exceed 100 MMbopd within a few months, pushing feedstock demand higher, although ample stockpiles around the world are expected to be able to fulfill this demand without much trouble in the near term. US crude stocks have been falling, but gasoline and distillate stocks have been rising, leaving question marks about whether spot price gains can continue at their recent pace.

US crude production is expected to average 8.6 MMbopd in 2016, according to the EIA. This would represent a drop of 0.8 MMbopd from average 2015 output. In fact, estimated May 2016 output, 8.7 MMbopd, is now a full million barrels per day below last April’s 9.7 MMbopd. It remains to be seen how shale producers will respond to the substantial price recovery we’ve had since February and whether some of the drilled but uncompleted wells (DUCs) will begin to be brought on-stream.

In Canada, Loonie’s appreciation continued slowly into Q2, but has retreated in recent days following “Brexit”, resulting in a similar crude price recovery when compared to the US since March. Light, sweet crude in Alberta has traded between 2 and 5 USD/bbl below WTI. Edmonton condensate has averaged a couple dollars below WTI, and the WCS discount to WTI has been relatively stable, and slightly tighter than historical norms, at 12-14 USD/bbl.

Despite some rather extreme volatility in Canadian natural gas prices, recent price movement in North American natural gas prices suggests the past quarter will be remembered as a positive one on the gas price front. Henry Hub prices have improved from well under 2.00 USD/MMBtu to over 2.50 USD/MMBtu on the back of lower than expected recent supply builds and warm weather driving cooling demand. AECO prices in Alberta for August delivery are back above 2.00 CAD/MMBtu at the time of writing, which, while not exactly exciting, are welcome when compared to the sub-1.00 to 1.50 CAD/MMBtu range they occupied for most of the past few months. Already-weak AECO prices were exacerbated in May by oil sands outages due to the recent Alberta wildfires. The differential between AECO and Henry Hub has also finally begun to narrow, thanks in part to the NEB’s recommendation to approve the NOVA system expansion in northern Alberta.

Outside North America, natural gas prices have continued their decline since last quarter, but are showing signs of life with a bounce off recent lows. UK NBP gas prices are down significantly from last year, but have shown strength in the past couple months on slightly healthier demand, relative currency valuations and higher global energy prices in general. Japanese spot LNG prices spent some time at 4.30 USD/MMBtu in May, which is down a few dollars from last quarter and down from over 16 USD/MMBtu in 2014. Since then, LNG prices have recovered somewhat on hotter temperatures and an upswing in near term power demand around the world, but the IEA’s recent outlook suggests the current global LNG glut is likely to last until at least 2019. While international gas prices remain substantially higher than those in North America, it is certainly a more challenging environment for LNG export economics than it was a few years ago.

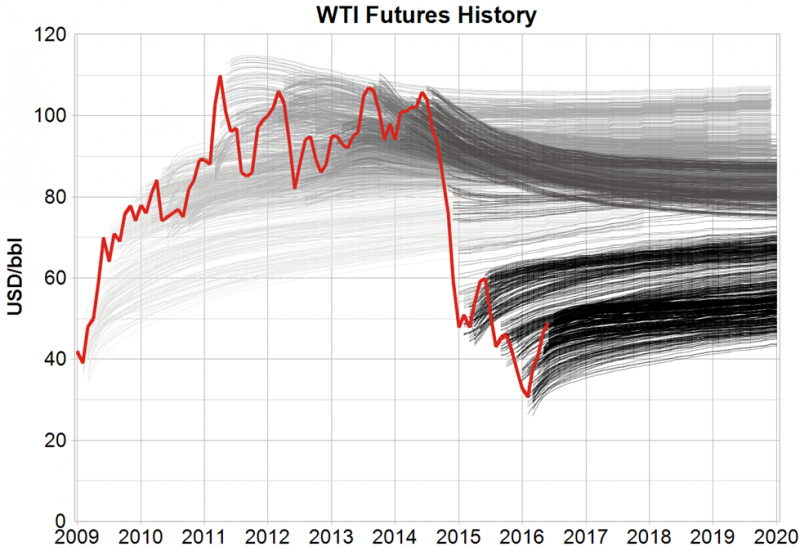

Finally, the plot shows the ebbs and flows of the daily WTI forward curves plotted against the historical prompt month WTI prices. While there has been a huge amount of movement in both the prompt month prices and forward curves, one thing that becomes apparent in recent years is a tendency of the longer end of the forward curves to exhibit some mean reversion. While forward curves are not true price forecasts, it certainly seems like those willing to hedge (or speculate) more than a couple years out are more comfortable with prices below 100 USD/bbl and above 40 USD/bbl.

Tyler Schlosser is GLJ’s Director of Commodities Research, focusing on economic modeling, risk analysis, commodity pricing and business development. Tyler is responsible for generating GLJ’s commodity price forecasts and modeling fiscal regimes across a broad range of international jurisdictions.

{kind=link}