In this article, I will attempt to de-mystify the difference between Canadian Crude and WTI (West Texas Intermediate) as we at Auspice Capital Advisors believe global investors may find a more clear way to gain crude oil exposure with an edge beyond WTI.

Historically, this opportunity was only available to wholesale energy traders. As a result, the Canadian Crude market is something that is not well understood. However, given this is the largest foreign supply to the US (greater than Saudi Arabia) the reality is that its importance and influence is undeniable and it represents an opportunity for a range of global investors.

Canadian Oil Facts

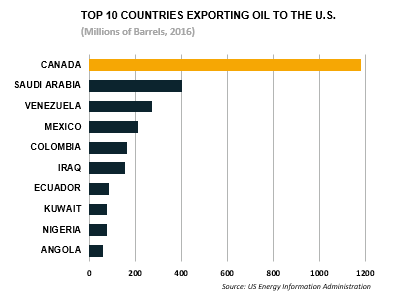

Canada is the largest foreign supplier of oil to the US at over 40% of all US imports. This is more than all OPEC producers combined and roughly 3 times what Saudi Arabia itself supplies. Almost all Canadian oil production goes to the US. See below.

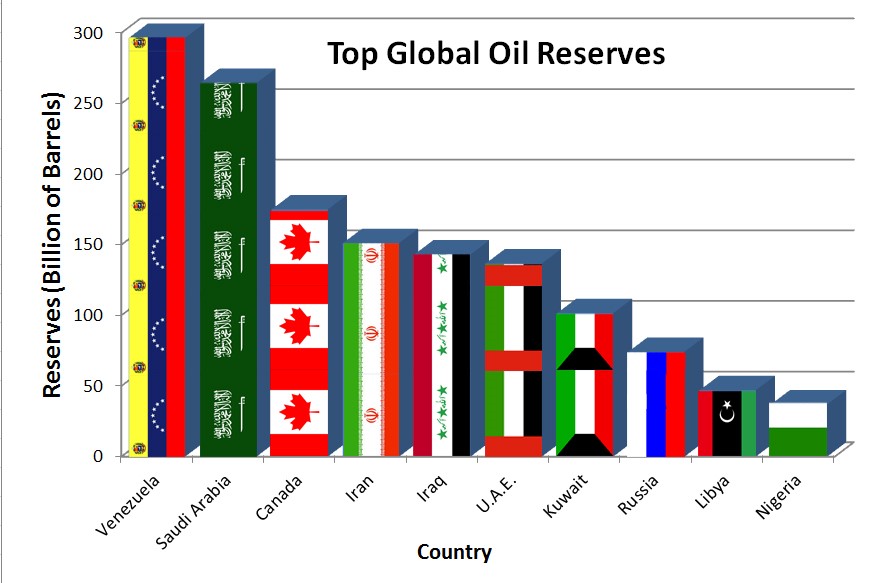

75% of Americans think the majority of their oil imports are from the middle-east. Canada has the 3rd largest oil reserves in the world only behind Venezuela and Saudi Arabia. Some argue and we believe that at modern recovery factors, Canada actually has the largest reserves, more than the top two combined.

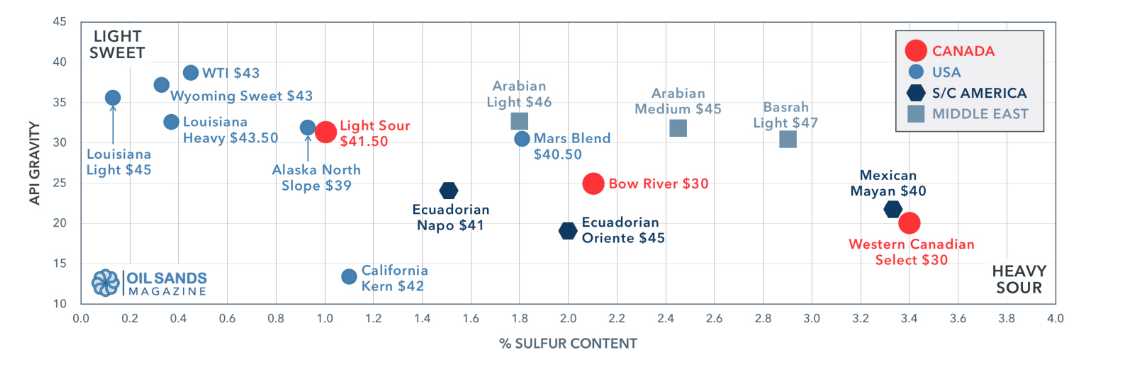

Canada ranks as the most socially progressive country of the top global oil producing nations. While Canada produces many types (grades) of crude, the “Heavy-Sour” grade is the dominant grade. Most Canadian producers, which are some of the largest in the world, have heavy oil production linked to WCS.

Reasons for the discount

Given WTI is considered “light-sweet” and Canadian Crude is predominantly “heavy-sour”, this is often the source of confusion that causes both controversy, misunderstanding and opportunity. As implied by the name, “heavy-sour”, one cannot help but to think in negative terms and thus justify the lower price. However, Canadian Crude is discounted primarily due to transportation constraints and costs not the grade. Other global heavy grades trade much closer to WTI. See below.

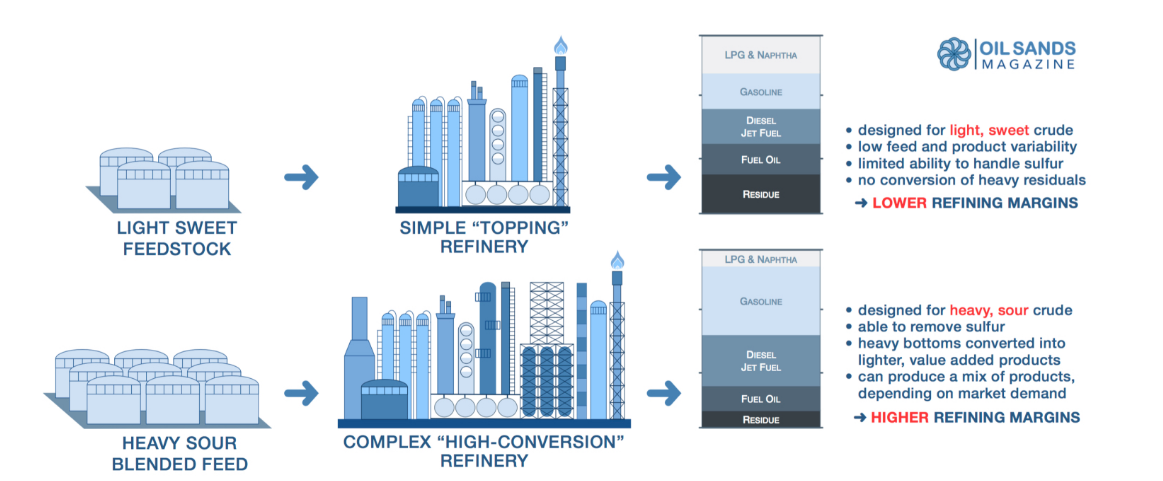

There is huge global demand for heavy crude for refining. According to the Canadian Association of Petroleum Producers, the US Gulf is now the world’s largest heavy oil refining cluster and refineries on the Gulf and mid-west have been purpose built or retooled for heavy crude. In a report from IHS Markit, by 2020 Canada could supply a full one-third of its refining market. As a result, since 2008 US imports of light-sweet have dropped to almost zero. Refineries get better margins from heavy-sour crude and refinery demand is increasing. Per the graphic below, refineries are now able to manage sulfur content and producer a wider range of products targeting higher margins.

Alternative global sources of heavy-sour imports are facing supply constraints (e.g. Venezuela). Per a JP Morgan Global Commodities Research February 2018 Report, “Canadian Crude is extremely important for the refineries in the Gulf Coast of the US. With the declining supplies from Mexico and Venezuelan heavy crude…the need for Canadian Crude will only increase further.” Oil is moved from Canada to the US by pipeline or rail at significant cost ($8-$21 per barrel) while the cheapest method of oil transport is by oil tanker at only a few dollars per barrel. This is something Canada is getting closer to which may change the balance of global oil supply and movement. The result may be substantially higher prices for crude oil from Canada.

Benchmark for Canadian Oil

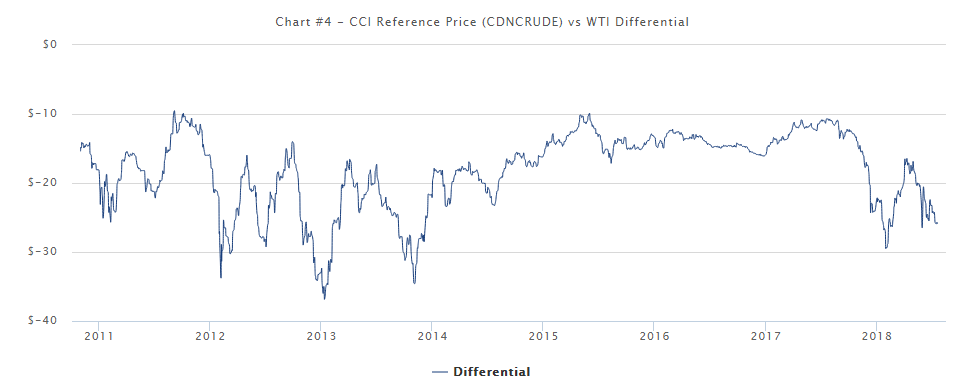

While most people have heard of WTI, this is not the benchmark for the bulk of oil produced in Canada and sent to the US. The largest commercial oil stream in Canada is WCS, which is a heavy oil blend. Western Canadian Select combines a number of types of oil and is used by producers for pricing as a discount, or deduction from WTI. As such – we reference a more simple benchmark that accurately reflects the commodity price, risk and volatility of Canadian oil. The CCI or Canadian Crude Index was created to compare the price of Canadian heavy crude to that of WTI in US dollars per barrel. Given the discount and the importance, and the ease of observing and tracking it through the CCI, this benchmark creates transparency and makes understanding the opportunities more obvious.

CCI Details

The CCI represents a simple and liquid benchmark for heavy-sour oil that is produced in Canada. The CCI was created to give investors and traders simple transparency and access to one of the world’s most important oil grades and progressive markets – heavy-sour oil from Canada. Discount – given Canadian Crude trades at a discount to WTI, this differential, called WCS, is what we have subtracted from WTI to illustrate a price in USD per bbl. The index is a 3 month exposure thus reducing the effect of rolling contracts and the dreaded contango that is often a criticism of commodity investments. Why does this benchmark matter? When you trade Canadian crude you are arguably trading the barrel that balances the US market, is most competitively priced, and the most important for setting prices for all other North American crude grades.

Opportunities

Given the US dependency on Canadian crude supply and the massive demand, Canadian crude is extremely important to the pricing of crude oil in North America and has an important influence on the price of WTI. Canadian crude is a leading indicator of price movement as refineries chase this important and cheap feedstock. Think what happens when there is a supply disruption in Canada – prices such as WTI react quickly. While highly correlated to WTI, the discounted price leads to an outperformance in price movements. For example, if you are bullish oil, a $10 move is 20% from a $50 CCI versus only 14% from a $70 WTI price. Volatility is higher in Canadian Crude and normalized returns are greater (both up and down – so buyer beware). This can create greater tactical trading opportunities for investors. The discount over time: Recently the Canadian heavy oil price has been discounted deeply, below the -$14 to -15 average we have seen in recent years. With additional storage, pipeline optimization and rail capacity coming, deep discounts may be good entry points. See below.

Canada with global access (beyond the US) changes a lot in world oil supply and demand economics. Refineries in Asia are also tooled for heavy-sour crude and pipeline transportation costs to tidewater by pipeline are only a few dollars. As Canadian producers and marketers find creative ways to get this oil shipped out of Canada, we believe the differential may change substantially. Moreover, added pipeline capacity to the US and export capability to Asia may also narrow this spread. Pipelines are being added including Keystone XL to the US, expansion of Enbridge (Line 3), TransMountain as purchased by the Canadian Government from Kinder Morgan. There is only one investment product in the world with access to heavy-crude, the Canadian Crude Index ETF (CCX on Toronto), including a forthcoming US dollar version.

If you are looking for an edge in oil, consider the following: Canada is the largest supplier of oil to the US, more than 3 times Saudi Arabia and all of OPEC combined. Oil from Canada is critical to US Energy security and in setting the price of all crude in North America. The discount for Canadian heavy oil is primarily because of transportation costs to US refineries. Heavy oil is demanded globally because refineries can make greater margins on the value-added products. Until the launch of the CCX ETF, trading heavy oil was only available to wholesale (producers and banks) energy traders. While highly correlated to WTI, the discounted price means material outperformance and more volatility in bull and bear markets. Since the oil lows in January of 2016, Canadian Crude ETF products have outperformed WTI based ETF products. This is an opportunity for market speculators and investors.

Tim Pickering is the Chief Investment Officer and Founder of Auspice Capital Advisors