Canada’s oil patch has been the victim of bad PR for the past several years. Canadian crude has been labelled dirty, heavy, sour, and environmentally unfriendly. Canada hasn’t been able to make any progress on new pipelines, and the United States remains the only viable export market. Energy executives are openly wondering whether it makes sense to invest in this country. In addition to that negative sentiment, Canadian crude sells for about 60 per cent less than its American counterpart, West Texas Intermediate (WTI). Many people incorrectly blame the discount on this negative perception. Up until May 21, when Kinder Morgan sold the Trans Mountain pipeline to the Federal government, Canadian crude was significantly outperforming WTI – it was up 40 per cent compared to a 20 per cent gain for WTI.

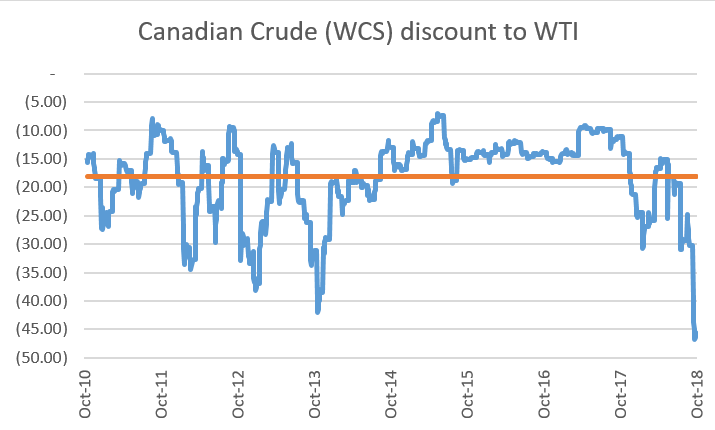

However, that announcement and the further delays to the project caused the per barrel discount to widen to over $40, well below the average of $18 since 2011. As a result, the CCI (Canadian Crude Index – ticker CDNCRUDE) is down 30 percent year-to-date, now significantly lagging WTI gaining 10 per cent. The wide differential between Canadian crude and WTI is bad for Canadian oil companies and bad for the revenue streams of Provincial and Federal governments. But it could represent a tremendous opportunity for investors.

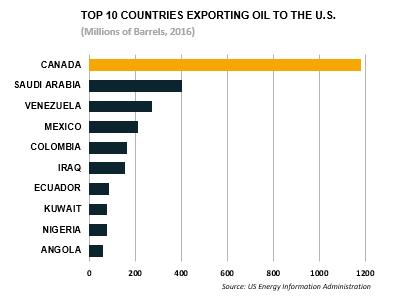

Despite the bad press, there are a lot of reasons to be optimistic about the Canadian energy industry. Canada supplies about 40% of all U.S. oil imports, more than any other country. Canada sends more oil to the U.S. than all OPEC producers combined and about three times more than Saudi Arabia. And when you account for modern recovery methods, some analysts believe Canada has the largest oil reserves in the world – more than Venezuela and Saudi Arabia combined.

We also need to dispel the myth that Canadian oil is undesirable because it’s heavy. Canada produces many grades of crude with the dominant type being heavy-sour. There is huge global demand for heavy crude, with U.S. refineries in the Gulf and Midwest being retooled or purpose-built to process heavy-sour. Refineries earn better margins on heavy-sour crude, so they are looking to increase the amount they process. As refineries search for the cheapest inputs, Canadian crude is their top choice. Asia also wants access to this supply.

Clearly, the fact that Canada produces heavy crude is not the reason for the large differential between CCI and WTI. Other global heavy crudes trade much more closely to WTI. The reasons for the discount are obvious: transportation costs and constraints, a lack of pipeline capacity, and an inability to reach buyers other than the U.S.

This is where the opportunity comes in for investors. Canadian oil, which is highly correlated to WTI, is currently on sale. As such, if you’re bullish oil, the discounted price of Canadian crude means it could materially outperform WTI as prices rise like they did at the beginning of 2018. By simple example, a $10 gain on CCI at the current $30 US/bbl is a 33% return while the same $10 gain is only 14% for WTI at $70. If and when Canada makes progress on the Trans Mountain extension or other pipeline projects such as Enbridge Line 3 or Keystone XL as well as add storage and rail capacity, that could mean even more upside for Canadian crude prices from these historically deep discount levels.

Regardless of long-term views on fossil fuels and alternative energy sources, there are many reasons to be bullish oil prices over the next few years. Global demand is strong, the developing world is growing its need for fuel, and there are brewing supply deficit issues among large producers like Canada, Venezuela and even Saudi Arabia.

There are several ways investors can get exposure to Canadian oil prices. They can buy shares of individual energy companies, or an ETF that holds a large swath of the TSX energy stock index. For more direct exposure to Canadian oil prices, investors can simply use the Canadian Crude Index ETF (ticker CCX), which tracks the CCI.

Canada’s opportunity is rare: a stable, socially progressive producer, with massive reserves of an in-demand grade of oil and direct access to the world’s largest consumer. Canada’s well-publicized issues have put it’s oil on sale, but if you’re bullish energy, Canadian crude could mean big returns for your portfolio without the stock market risk. It is a little-known edge for investors and traders.

Tim Pickering is the CIO and Founder of Auspice Capital Advisors