The Duvernay formation in Canada represents over 200 MBOE/d of production, including more than 87 Mbbl/d of oil and condensate (including pentane). A play that saw strong growth up until the end of 2019, it has mostly flat-lined in terms of overall production since then, although has been showing signs of picking up again recently. Figure 1 below shows the production history for all wells currently producing from the Duvernay.

All of the charts and data provided below come from public data sources BOE Intel and Petro Ninja. To get access to these tools for yourself and your company, contact us here.

Figure 1

Five months ago, Chevron let it be known that it was going to be putting its Duvernay assets up for sale. While public disclosure since then has been minimal, we figured it was probably worth checking in on what’s happening in terms of public data production results and what we can see for production in the various different parts of the play.

CHEVRON UPDATE

While we wait for any potential updates on the Chevron potential asset sale, we can use BOE Intel to take a peek and what the public data says about the company’s gross licensed production (Figure 2). After some major forest fire related downtime last summer, monthly gross volumes got almost as high as 69 MBOE/d in November 2023, while the most recent month of production suggested volumes were just shy of 53 MBOE/d. Keep in mind that at last check, KUFPEC Canada Inc. held a 30% non-operated interest in Chevron Canada’s Duvernay leaseholdings. If you assumed a 70% working interest then for Chevron, the November 2023 net licensed production figure would be ~48 MBOE/d, while the April 2024 net figure would be ~37 MBOE/d. Technically the chart below is for all wells licensed to Chevron (not just Duvernay), but the Duvernay represents pretty much 100% of the company’s licensed production in Canada (Chevron does still have a 20% non-operating working interest in AOSP).

Figure 2

![]()

KAYBOB AND AREA

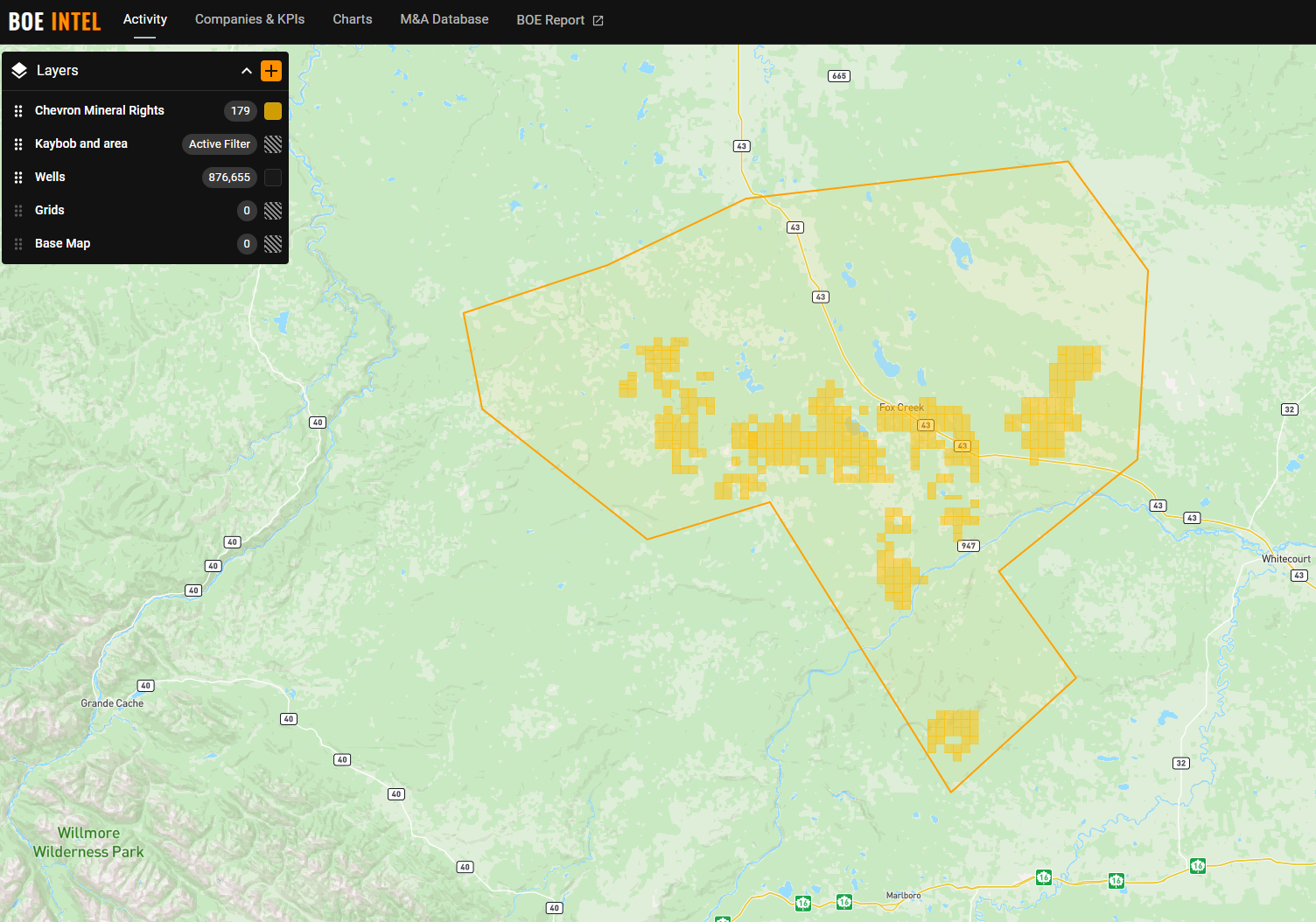

This area represents the vast majority (80%+) of the Duvernay production in the WCSB. Shown below is a rough area that encapsulates the majority of the Duvernay activity over the last decade, and we’ve used it to filter for production by operator. Also shown are the mineral rights of Chevron.

Figure 3

On a gross basis, Chevron is the top producer from the Duvernay formation, not only in this area, but in terms of Duvernay production in Canada. However, on a net basis, they are likely fairly equal with Veren. In fact, Veren’s June 2024 corporate presentation points to 2024 average guidance for Duvernay production of ~50,000 BOE/d, suggesting that Veren may already be in the process of overtaking Chevron for largest Duvernay producer.

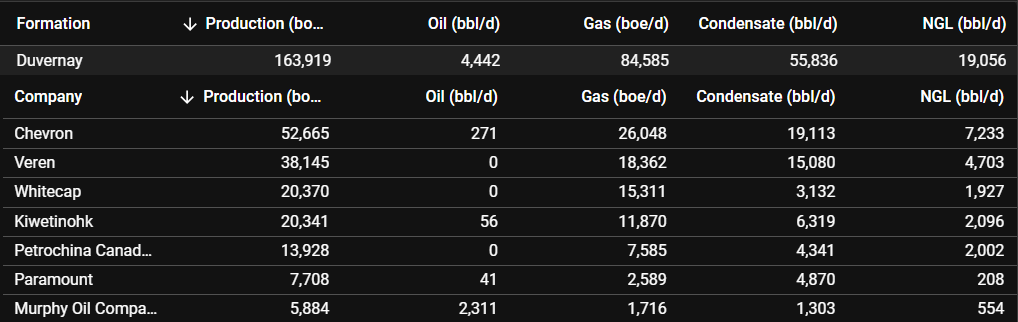

Using the area marked on the map above (Figure 3), these are the top Duvernay producers:

Figure 4 – Gross licensed production – Kaybob and area Duvernay production – April 2024 volumes

WILLESDEN GREEN AND SURROUNDING AREA

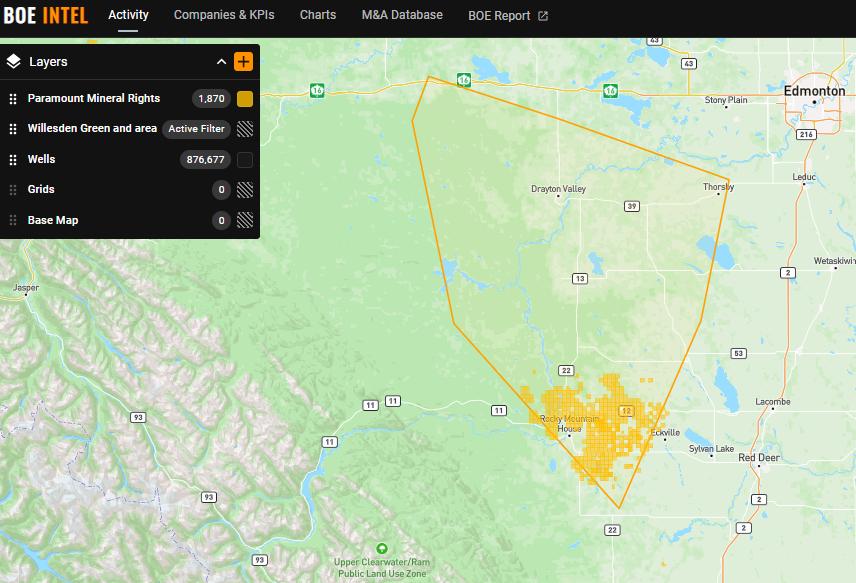

Willesden Green is the smallest Duvernay producing area, with total production in the area of around 14 MBOE/d. Most of the production comes from the southern part of the area shown, but there have been some historical spuds in the other areas so we made the polygon large enough to encapsulate many of those. The largest operator in this area is Paramount Resources, and we have shown its mineral rights below in Figure 5.

Figure 5

Using the area marked on the map above (Figure 5), these are the top Duvernay producers from that area:

Figure 6 – Gross licensed production – Willesden Green and surrounding area Duvernay production – April 2024 volumes

EAST SHALE DUVERNAY

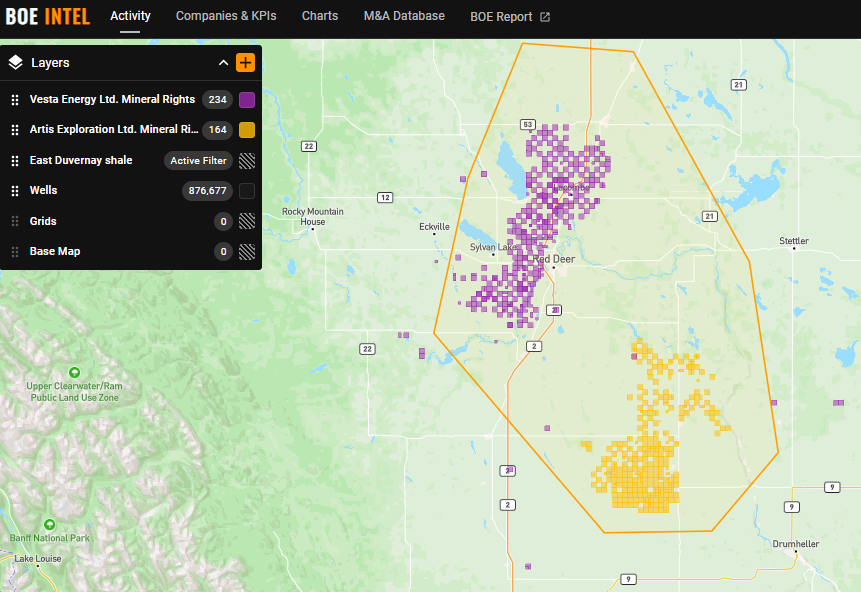

This area is dominated by two private companies, Artis Exploration and Vesta Energy. The two companies represent more than 99% of the Duvernay production in the area. We have shown the mineral rights for both below in Figure 7.

Figure 7

Using the area marked on the map above (Figure 7), these are the top Duvernay producers from that area:

Figure 8 – Gross licensed production – East Shale Duvernay production – April 2024 volumes

Confidential production

While the area continues to see strong interest, it also continues to be a highly competitive area. In fact, there are 68 Duvernay wells on production that are still under Confidential status, meaning that NGLs would not be viewable. Those companies with wells on confidential status will likely have underreported production using public sources, as often significant NGL production will be missing. In those cases, we use gas equivalent volumes as a placeholder until the NGL data comes off confidential.

| Licensee | Duvernay wells on production with confidential status |

|---|---|

| Artis Exploration Ltd. | 18 |

| Veren Inc. | 15 |

| Vesta Energy Ltd. | 10 |

| Paramount Resources Ltd. | 9 |

| Whitecap Resources Inc. | 4 |

| Baytex Energy Ltd | 3 |

| Kiwetinohk Energy Corp. | 2 |

| Gmt Exploration Zama Inc. | 2 |

| Athabasca Resources Inc. | 2 |

| Chevron Canada Limited | 2 |

| Teine Energy Ltd. | 1 |