On December 4, 2014, the Canadian Securities Administrators published amendments to National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities and those amendments became effective July 1, 2015. This blog is the first in a series that will describe the significant changes, as seen through the eyes of a qualified reserves evaluator (QRE).

Part 1: Abandonment and Reclamation

Prior to the amendments, the Canadian Oil and Gas Evaluation Handbook (Volume 1, Section 7.6.4) was interpreted to recommend the inclusion of only downhole abandonment costs for existing and future reserves wells in the future net revenue of reserves evaluations. Further disclosure, as specified in Item 6.4 (d) of Form 51-101F1, required reporting issuers to describe the portion of the abandonment and reclamation costs not included. With the amendments, Item 6.4 was repealed and, going forward, publicly disclosed estimates of future net revenue must be net of abandonment and reclamation costs.

For clarification, NI 51-101 (Section 1.1) now provides definitions for future net revenue and abandonment and reclamation costs:

Future net revenue – A forecast of revenue, estimated using forecast prices and costs or constant prices and costs, arising from the anticipated development and production of resources, net of the associated royalties, operating costs, development costs and abandonment and reclamation costs.

Abandonment and reclamation costs – All costs associated with the process of restoring a reporting issuer’s property that has been disturbed by oil and gas activities to a standard imposed by applicable government or regulatory authorities.

And, Item 2.1(2) of Form 51-101F1 formally requires disclosure of the net present value of future net revenue, by definition, net of abandonment and reclamation costs. Of course, the fundamental question is: “Which abandonment and reclamation costs need to be included in the QRE’s reserves evaluation?”

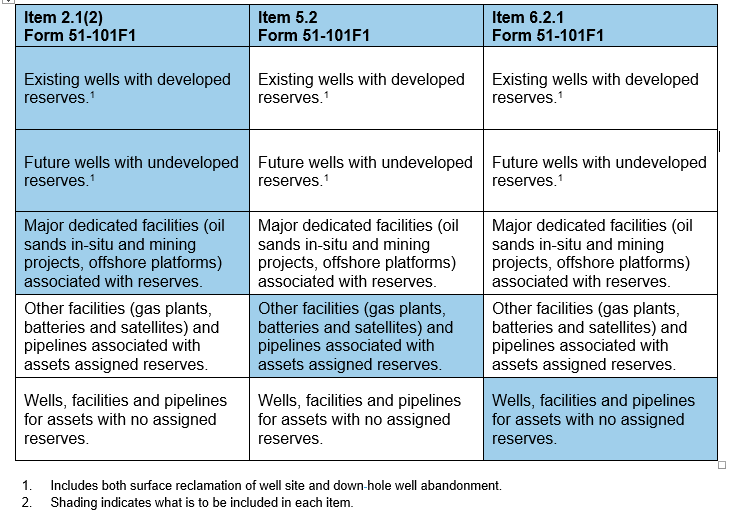

Full disclosure of abandonment and reclamation costs includes both existing and future leases, wells and facilities up to the first point of sale:

- The reporting issuer will disclose abandonment and reclamation costs for existing leases, wells, pipelines and facilities up to the first point of sale in their financial disclosure of Asset Retirement Obligations (ARO).

- Typically, the QRE will include the downhole abandonment and surface reclamation costs for existing and future reserves wells, but, in certain instances, when the abandonment and reclamation costs for major dedicated facilities (i.e. offshore platforms, thermal central processing facilities, bitumen extraction and upgrading facilities, etc.) are significant, those costs will also be included. (The reserves evaluation may not include abandonment and reclamation costs for non-reserves wells, minor facilities and other miscellaneous infrastructure, unless specifically requested by the reporting issuer.)

The following quick reference table summarizes the disclosure requirements in Form 51-101F1 Statement of Reserves Data and Other Oil and Gas Information.

If the information required for Items 5.2 and 6.2.1 is contained in the financial statements of ARO, the reporting issuer may satisfy these items by directing the reader to those relevant sections. Conspicuously, there is some overlap between the reporting issuer’s ARO and the reserves evaluation. It is recommended that the reporting issuer identify the nature and amount of the overlap.

Stay tuned for Part 2 of this series: Disclosure by Product Type.

Read more insightful blogs from GLJ Petroleum Consultants here