CALGARY, ALBERTA–(Marketwired – May 11, 2016) – Delphi Energy Corp. (TSX:DEE) (“Delphi” or the “Company”) is pleased to announce its financial and operational results for the quarter ended March 31, 2016.

First Quarter 2016 Highlights

- Generated funds from operations of $8.2 million and realized net earnings of $5.3 million;

- Successfully drilled two gross (1.7 net) wells as part of the Company’s capital program and completed, tied-in and brought on production two gross (1.5 net) Montney wells in East Bigstone;

- Produced an average of 8,395 barrels of equivalent per day (“boe/d”), a 24 percent decrease from 11,002 boe/d in Q1 2015 as a result of the 2,600 boe/d of dispositions completed in the second half of 2015;

- Increased production from the Montney in East Bigstone by six percent to 7,363 boe/d compared to the fourth quarter of 2015 and 2 percent from the comparative first quarter of 2015;

- Increased Montney natural gas liquids (“NGL”) and field condensate yields to 106 barrels per million cubic feet (“bbls/mmcf”) in the first quarter of 2016 compared to 95 bbls/mmcf in the first quarter of 2015. Field and plant condensate yield was 72 bbls/mmcf or 68 percent of the total 106 bbls/mmcf;

- Achieved a 19 percent reduction in operating costs to $6.74 per boe in the first quarter of 2016 compared to the same period in 2015. The Montney operating costs continue to trend downward achieving a record low $6.04 per boe in the first quarter of 2016;

- Achieved realized gas prices of $3.08 per mcf, prior to realized risk management gains, as a result of 88 percent of the Company’s natural gas sales now being shipped on the Alliance pipeline and sold into the Chicago market. Including realized risk management gains, the Company realized $4.35 per mcf in the first quarter 2016;

- Realized gains of $6.0 million from commodity price risk management contracts; and

- At March 31, 2016, Delphi’s risk management contracts had a mark to market value of $23.1 million, up from $18.5 million at December 31, 2015.

| Financial Highlights ($ thousands except per unit amounts) | ||||

| Three Months Ended March 31 | ||||

| 2016 | 2015 | % Change | ||

| Crude oil and natural gas sales | 17,316 | 22,650 | (24) | |

| Realized sales price per boe | 30.47 | 27.44 | 11 | |

| Funds from operations | 8,190 | 10,781 | (24) | |

| Per boe | 10.72 | 10.88 | (1) | |

| Per share – Basic and diluted | 0.05 | 0.07 | (29) | |

| Net earnings | 5,259 | 1,995 | 164 | |

| Per boe | 6.89 | 2.02 | 241 | |

| Per share – Basic and diluted | 0.03 | 0.01 | 200 | |

| Capital invested | 16,658 | 17,269 | (4) | |

| Disposition of properties | (4,583) | – | 100 | |

| Net capital invested | 12,075 | 17,269 | (30) | |

| March 31, 2016 | December 31, 2015 | % Change | ||

| Net debt (1) | 126,415 | 121,664 | 4 | |

| Total assets | 365,723 | 360,842 | 1 | |

| Shares outstanding (000’s) | ||||

| Basic | 155,510 | 155,510 | – | |

| Diluted | 169,901 | 169,951 | – | |

| (1) | Defined as the sum of long term and subordinated debt plus (minus) the working capital deficit (surplus) excluding the current portion of the fair value of the financial instruments. |

Operational Highlights

| Three Months Ended March 31 | |||

| Production | 2016 | 2015 | % Change |

| Field condensate (bbls/d) | 1,700 | 1,592 | 7 |

| Natural gas liquids (bbls/d) | 1,335 | 1,698 | (21) |

| Crude oil (bbls/d) | 5 | 8 | (38) |

| Total crude oil and natural gas liquids (bbls/d) | 3,040 | 3,298 | (8) |

| Natural gas (mcf/d) | 32,127 | 46,223 | (30) |

| Total (boe/d) | 8,395 | 11,002 | (24) |

MESSAGE TO SHAREHOLDERS

Delphi is pleased to report the operating and financial results of the first quarter of 2016 representing the first full quarter subsequent to the significant dispositions in the second half of 2015 and the first full quarter of transporting almost all of its natural gas on the Alliance pipeline to Chicago, avoiding the congested Alberta market and lower realized prices.

The commodity price environment continued to be very challenging with West Texas Intermediate (“WTI”) crude oil prices averaging US $33.58 per barrel during the first quarter of 2016, down 31 percent from the comparative quarter of the previous year. NYMEX natural gas prices averaged US $2.04 per mmbtu in the first quarter, down 28 percent from the comparative quarter of 2015.

The Company continues to successfully navigate this lower commodity price environment with a conservative approach to capital spending, with expenditures funded from cash flow generated while improving new well productivity, reducing capital costs and lowering operating costs. All contributing to a sustainable economic business. The Company generated a field operating netback of $14.62 per boe in the first quarter of 2016 while adding new reserves and production at lower well costs than in 2015, which for Montney proved producing reserves, the finding and development costs were $10.12 per boe.

Production volumes in the first quarter of 2016 averaged 8,395 boe/d. Production volumes decreased approximately 2,600 boe/d or 24 percent from the comparative quarter of 2015 due to the disposition of the Company’s Wapiti assets in the third quarter of 2015 and the disposition of its Greater Hythe assets in the fourth quarter of 2015. As planned, Montney production at the Company’s Bigstone property in the first quarter of 2016 was maintained relatively flat to the comparative quarter of 2015, averaging 7,363 boe/d and representing 88 percent of the Company’s production.

Delphi’s field condensate weighting as a percentage of first quarter of 2016 production volumes increased to 20 percent, up 39 percent, from 14 percent in the comparative quarter of 2015. The Company`s Montney natural gas liquids and field condensate yields increased to 106 barrels per million cubic feet in the first quarter of 2016, up from 95 bbls/mmcf in the first quarter of 2015. Field and plant condensate yield averaged 72 bbls/mmcf or 68 percent of the total 106 bbls/mmcf.

Delphi’s commodity price risk management program continues to be an integral part of its financial strategy to protect funds from operations during periods of price volatility. Despite the drop in crude oil prices, the Company received $56.55 per barrel for its condensate production in the first quarter of 2016, including a realized risk management gain of $14.34 per barrel for maturing contracts in the period. Delphi’s realized natural gas price for the first quarter of 2016 was $4.35 per mcf, an increase of 28 percent from the comparative period of 2015. The Company’s realized natural gas price was positively influenced by its risk management program as well and includes a gain of $1.27 per mcf for maturing contracts in the period.

Funds from operations in the first quarter of 2016 were $8.2 million or $0.05 per basic and diluted share, compared to $10.8 million or $0.07 per basic and diluted share in the comparative quarter of 2015. The decrease in funds from operations in the first quarter of 2016 as compared to the same quarter in 2015 is due to lower production volumes. Delphi’s cash netback was lower by one percent, relative to the comparative quarter, at $10.72 per boe. The average realized price per boe was up eleven percent due to natural gas sales into the Chicago market and realized risk management gains on both natural gas and field condensate. A reduction in operating costs is largely as a result of the major property dispositions completed during 2015. An increase in transportation costs is due to the shipping of the Company’s natural gas production through the Alliance pipeline to Chicago, effective December 1, 2015.

During the first quarter of 2016, Delphi invested $16.7 million primarily on drilling and completions. Delphi drilled two gross (1.7 net) wells and performed completion operations on two gross (1.5 net) wells in its Bigstone area. The Company also completed the installation of a compressor at its 7-11 Montney facility and fuel gas pipelines to deliver higher quality fuel gas to the Montney facilities. In the first quarter, Delphi received proceeds of $4.6 million in exchange for a gross overriding royalty on two gross wells completed during the quarter as part of its latest five well gross overriding royalty arrangement.

At March 31, 2016, the Company had $94.3 million outstanding in the form of bankers` acceptances and $2.0 million drawn under Canadian-based prime loans, $14.1 million outstanding under its subordinated credit facility and a working capital deficit of $16.0 million for net debt of $126.4 million and was in compliance with all covenants of the credit facilities. The Company reduced its net debt by 30 percent to $126.4 million at March 31, 2016 from $180.7 million one year earlier as a result of the dispositions successfully completed during 2015. Delphi’s lenders (National Bank of Canada, Bank of Nova Scotia and Alberta Treasury Branches) are in the process of completing their annual review of the Company’s senior credit facility and are expected to have it completed by May 25, 2016.

Operations Update

In the first quarter of 2016, Delphi drilled two gross (1.7 net) horizontal Montney wells at Bigstone. The Company also completed and brought on production 2 gross (1.5 net) horizontal Montney wells.

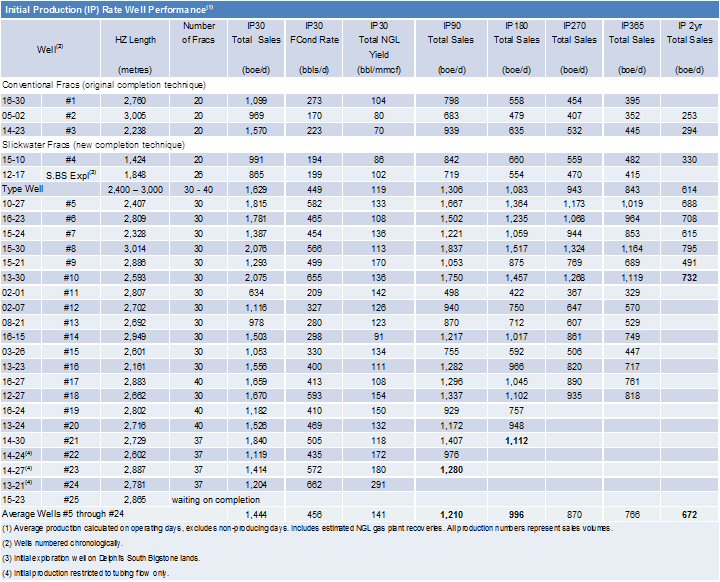

The first well brought on production during the quarter was the 14-27-60-23W5 (“14-27”) well (0.88 net). 14-27 was drilled in the fourth quarter of 2015 and completed in early January, utilizing a 37 stage slickwater frac design. This was just the third well to utilize a slickwater only completion by Delphi at Bigstone. Initial production results are very encouraging with IP90 rates of 1,280 boe/d and a field condensate to gas ratio (“CGR”) over the same time period of 97 bbls/mmcf sales.

Delphi has recently brought on production the 13-21-60-23W5 (“13-21”) well (0.66 net), the western most Montney well drilled and completed with slickwater fracs by the Company to date. The 13-21 well was fraced over 37 stages with the largest slickwater frac for Delphi Montney wells to date. Slickwater frac volumes per metre of horizontal length were increased by 19 percent and proppant pumped per metre of horizontal length was increased by 15 percent over the previous frac at 14-27. Over the first 30 days of production, being restricted to flowing up the tubing only, the well averaged 1,204 boe/d with a field condensate to gas ratio of 252 bbls/mmcf sales, which is 79 percent higher than Delphi’s next highest field condensate to gas ratio from its horizontal Montney wells. The closest offset to 13-21 is approximately 800 metres to the east at 15-21-60-23W5 (“15-21”), which came on production in February of 2014. The average field condensate to gas ratio over the first 30 days of production for 15-21 was 130 bbls/mmcf sales and had a total rate of 1,293 boe/d over the same time period.

Delphi has continued to innovate drilling and completion techniques to drive costs lower, improving year over year capital efficiencies. Despite the increasing size of the fracs used to complete the most recent wells, drilling and completion costs for the last three wells averaged $7.0 million, a 15 percent reduction from the average costs for wells drilled in 2015 of $8.3 million and a 33 percent reduction from the average costs for wells drilled in 2014 of $10.4 million.

Innovation of the Company’s frac design continues to deliver encouraging results. With higher field condensate yields Delphi will be increasing its drilling activity to the west of the current development trend at Bigstone. Additionally, tighter inter-well spacing is being evaluated to distances as low as 200 metres from the current approximate 400 metres. Industry activity offsetting Delphi’s 13-21 well to the west of its current development trends and to the south, offsetting the Company’s 12-17-59-22W5 well, all indicate higher condensate yields are being achieved. The XTO 13-13-59-23W5 well reported a condensate yield of 259 bbls/mmcf from publicly available data. Delphi’s results combined with these reported industry successes indicate the area of opportunity to realize increased field condensate yields could be much larger than just the immediate offsets to the 13-21 well.

| Q1 2016 | 2015 | 2014 | |||

| Net Montney Wells Drilled | 1.7 | 5.2 | 7.6 | ||

| Average Measured Depth | (metres) | 5,779 | 5,655 | 5,591 | |

| Average Horizontal Length | (metres) | 2,823 | 2,733 | 2,674 | |

| Average Drilling Days per Well (Spud to TD) | 27 | 30 | 31 | ||

| Average Drilling Cost | ($000’s) | 4,000 | 4,604 | 4,927 | |

| Average Drilling Cost per Horizontal Metre | ($/metre) | 1,417 | 1,685 | 1,843 | |

| Net Montney Wells Completed | 1.5 | 5.2 | 7.7 | ||

| Average Number of Stages per Well | 37 | 37 | 30 | ||

| Average Proppant Pumped per Well | (tonnes) | 3,442 | 2,979 | 2,024 | |

| Average Proppant per Horizontal Metre | (t/m) | 1.22 | 1.09 | 0.77 | |

| Average Completion Cost | ($000’s) | 3,261 | 4,214 | 5,334 |

The following table has been updated to reflect new well production data since it was previously released and continues to illustrate the significant impact the slickwater fracturing technique has had on well performance at Bigstone in comparison to smaller conventional frac methods.

To view a table associated with this release, please visit the following link: http://media3.marketwire.com/docs/1054515_tab1.jpg

{kind=link}

The Company continues to pursue opportunities to reduce operating costs. Delphi estimates $6.5 million in reduced operating costs in 2016 over 2015, as the more efficient Montney production replaces higher cost properties disposed of in 2015. A new fuel gas pipeline accessing higher quality fuel gas has been installed and the 7-11 compression and dehydration facility has been expanded with an owned compressor replacing two existing rental compressors resulting in reduced maintenance and rental costs as well as increased throughput capacity. In addition, with the disposition of the lower netback properties, the Company has reduced its staff from 36 to 24 (33 percent), resulting in expected general and administrative savings of $2.0 – $2.5 million.

Addressing and optimizing the Company’s overall cost structure continues to be a primary focus to maximize profitability. Reduced capital costs and lower operating costs combined with a superior asset has enabled the Company to continue to deploy capital to its Montney play and continue to provide a high return on investment. Targeting reductions of 30 percent for capital costs, operating costs and general and administrative costs will enable the company to grow and profit in the current environment.

Alberta Royalty Review

The Government of Alberta recently announced additional details of the new Modernized Royalty Framework to be implemented for new wells drilled in 2017. Upon initial review of the new framework, the Company believes the intent of the new royalty framework, one being to maintain internal rates of returns for a company’s investment opportunities, is generally consistent with Delphi’s Montney prospects at Bigstone under current strip pricing assumptions.

Risk Management

On December 1, 2015, Delphi began delivering the majority of its natural gas production on its Alliance pipeline firm capacity into the Chicago market rather than the AECO market. Well in advance of commencement of these deliveries, the Company continued execution of its successful risk management strategy to protect its revenue stream into the Chicago market through NYMEX, Chicago basis and Cdn/US foreign exchange rate contracts. As a result, the Company is protected through the remainder of 2016 with approximately 74 percent of its natural gas production hedged at an average price of Cdn. $4.43 per mcf (excluding transportation costs). For 2017, the Company has approximately 50 percent of its natural gas production contracted at an average price of Cdn $4.20 per mcf (excluding transportation costs). Delphi also has approximately 43 percent of its condensate volumes contracted at a floor price of $76.49 per barrel. The table below summarizes the Company’s current commodity price risk management contracts for 2016 and future years.

To view a table associated with this release, please visit the following link: http://media3.marketwire.com/docs/1054515_tab2.jpg

{kind=link}

2016 Guidance

Delphi’s 2016 guidance incorporates a NYMEX natural gas price of US $2.00 per mmbtu and a WTI price of US $38.00 per barrel. The Company expects to drill 4-5 gross wells during the year. In the current environment, quarterly production will be managed in the context of the Company’s Alliance Pipeline commitments and risk management position. The table below summarizes the Company’s current guidance for 2016.

| 2016 Guidance | |

| Average Annual Production (boe/d) | 8,300 – 8,800 |

| Exit Production Rate (boe/d) | 8,500 – 9,500 |

| NYMEX Natural Gas Price (US $ per mmbtu) | $2.00 |

| WTI Oil Price (US $ per bbl) | $38.00 |

| Natural Gas Liquids Price (Cdn $ per bbl) | $16.50 |

| Foreign Exchange Rate (US/Cdn) | 1.35 |

| Well Count | 4.0 – 5.0 |

| Net Capital Program ($ million) | $33.0 – $38.0 |

| Funds from Operations (“FFO”) ($ million) | $32.0 – $37.0 |

| Net Debt at December 31 ($ million) | $121.0 – $126.0 |

| Net Debt / Q4 FFO (annualized) | 3.0 – 3.5 |

Outlook

Delphi continues to navigate this very challenging low commodity price environment with a singular focus on its core Bigstone Montney asset. This focused effort is successfully improving foundational cash generating efficiencies that will be more fully recognized as the rate of capitalization and production growth accelerates into the recovery phase of this commodity price cycle.

The Company continues to manage its production volumes in the context of its risk management program, contracted processing and transportation arrangements. Economic returns on the new capital deployed remain attractive as a result of the improving cash generating efficiencies from superior Chicago-based natural gas pricing, increased condensate yields, lower cost structures and a successful long term risk management program. Despite the significant drop in commodity prices over the past twelve months the Company’s cash netbacks have remained relatively constant, providing a predictable cash flow source for re-investment without increasing debt levels. Favorable recycle ratios in excess of 1.4 times continue to be generated as a result of the strong realized netbacks combined with efficient 2015 Montney proved producing finding and development costs of $10.12 per boe. Drilling and completion costs in the first quarter were down a further 18 percent from the 2015 averages.

Continued innovation of our well design, driving costs lower, while maintaining full ownership and control of our infrastructure are both paramount in our continued effort towards top decile capital and cash generating efficiencies. Generating margin growth trumps production growth in the current environment. Delphi expects to spend less than its cash flow generated through the first half of 2016, while remaining relatively flat to its 2015 exit rate of 8,300 boe/d. The Company’s significant risk management position through 2016 and 2017, protects both the equity account and the balance sheet, while contributing to a meaningful capital program of four to five wells in 2016. Delphi’s significant drilling inventory is immediately accessible to deliver production growth into a strengthening commodity price environment.

On behalf of the Board of Directors and all the employees of Delphi, we would like to thank our shareholders for their continued support.

CONFERENCE CALL AND WEBCAST

A conference call and webcast to review 2016 Q1 results is scheduled for 9:00 a.m. Mountain Time (11:00 a.m. Eastern Time) on Thursday, May 12, 2016. The conference call number is 1-866-225-0198. A brief presentation by David Reid, President and CEO and Brian Kohlhammer, Senior VP Finance & CFO, will be followed by a question and answer period. The conference call will also be broadcast live on the internet and may be accessed through the Delphi Energy website at www.delphienergy.ca or by entering http://www.gowebcasting.com/7483 in your web browser.

A taped rebroadcast will be available until 6:00 p.m. Mountain Time, Thursday, May 19, 2016. To access the rebroadcast, dial 1-800-408-3053 or 905-694-9451. The passcode is 4505981. It will also be available on Delphi’s website. Delphi’s first quarter 2016 financial statements and management’s discussion and analysis are available on Delphi’s website at www.delphienergy.ca and SEDAR at www.SEDAR.com.

The Company also announces that its Annual General Meeting (“AGM”) will be held on Tuesday, May 24, 2016 at 3:00pm (MST) in the Devonian Room at the Calgary Petroleum Club (319 – 5 Avenue S.W.). Shareholders are encouraged to attend.

For those unable to attend, a webcast presentation of the Company’s AGM will begin at approximately 3:15pm (MST), following the business portion of the meeting.

To listen to this event, please visit our website at www.delphienergy.ca or enter http://www.gowebcasting.com/7553 in your web browser.

Delphi Energy is a Calgary-based company that explores, develops and produces oil and natural gas in Western Canada. The Company is managed by a proven technical team. Delphi trades on the Toronto Stock Exchange under the symbol DEE.