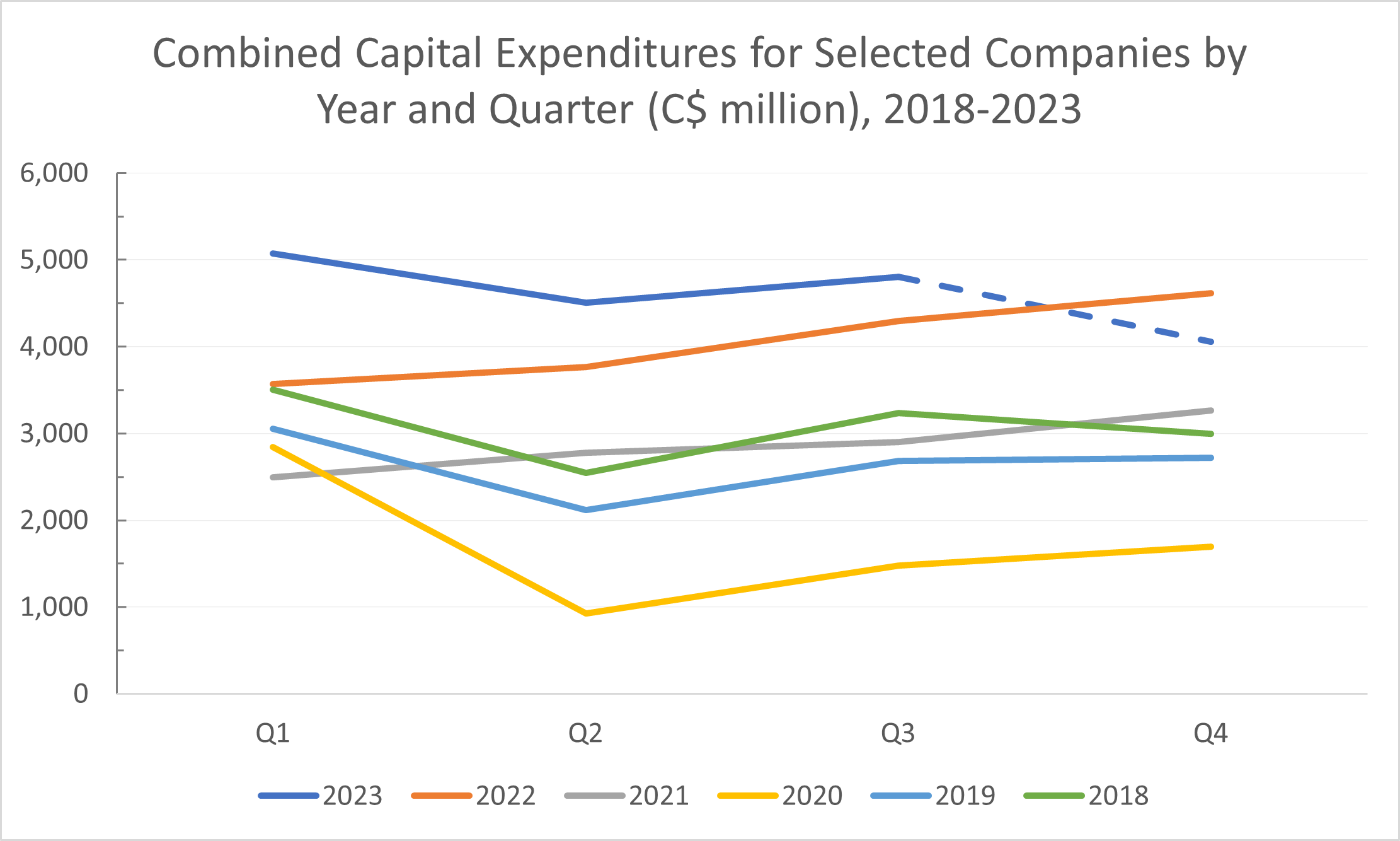

With a number of companies having now reported Q3 2023 results, we thought it was an opportune moment to check in on year-to-date capital spending. 2023 has been nothing if not eventful, with an everchanging macroeconomic picture creating significant swings in oil and natural gas markets. WTI, for instance, has oscillated from the high 60s to the low 90s throughout the year, complicating financial projections and capital planning for Canadian E&Ps despite the year having been quite positive for the industry overall.

With this in mind, we wanted to examine how actual capital spending has compared to budgets for companies that have released Q3 results, and examine implied spending in the fourth quarter (based off of the portion of each company’s budget that is still remaining).

| Canadian E&Ps | Q1 2023 | Q2 2023 | Q3 2023 | 2023 Budget | Implied Q4 2023 | % Left |

| Perpetual | 9.1 | 1.8 | 7.3 | 28.5 | 10.3 | 36% |

| Surge Energy | 45.7 | 30.6 | 43.9 | 175.0 | 54.7 | 31% |

| Athabasca Oil | 26.4 | 41.4 | 33.3 | 145.0 | 43.9 | 30% |

| ARC Resources | 487.4 | 416.5 | 401.4 | 1,850.0 | 544.7 | 29% |

| Paramount | 184.1 | 140.2 | 198.9 | 737.5 | 214.3 | 29% |

| Cenovus | 1,101.0 | 1,002.0 | 1,025.0 | 4,250.0 | 1,122.0 | 26% |

| Vermilion | 154.8 | 166.8 | 125.6 | 590.0 | 142.7 | 24% |

| Crescent Point | 314.2 | 230.1 | 315.2 | 1,100.0 | 240.6 | 22% |

| Baytex* | 233.6 | 170.7 | 409.2 | 1,035.0 | 221.5 | 21% |

| Whitecap Resources | 253.6 | 217.8 | 281.9 | 925.0 | 171.7 | 19% |

| CNRL** | 1,394.0 | 1,669.0 | 1,231.0 | 5,400.0 | 1,106.0 | 20% |

| Tourmaline | 601.8 | 238.5 | 546.2 | 1,675.0 | 288.5 | 17% |

| Tamarack Valley | 148.2 | 117.8 | 122.8 | 450.0 | 61.2 | 14% |

| Advantage Energy | 116.7 | 61.7 | 61.2 | 265.0 | 25.4 | 10% |

* Baytex increased its capital budget to $1,035 million following its acquisition of Ranger earlier this year.

** Corrected after publishing, see Editor’s Note at the end of the article.

In examining the figures above, there are only 6 companies “behind schedule” in the sense that more than a quarter of their capital budgets remain to be spent as of September 30. On the other end, 8 companies are “ahead of schedule”. As another qualifying note, we want to acknowledge that companies we tag as being behind or ahead of schedule may have timed their spending precisely as intended; capital programs are seldom spread perfectly evenly through the year, and are subject to change.

With respect to companies that have loaded spending in the first 3 quarters, a few names stand out. Advantage Energy spent 90% of its 2023 budget before September 30, most of which was devoted to developing 27 gross (23 net) wells spread across Glacier, Valhalla and Wembley. As it stands, 22 wells have been spud by the company since January 1. Tamarack Valley’s spend is also set to taper off in the fourth quarter, with 86% of its budget already spoken for primarily by Clearwater/Charlie Lake infrastructure enhancements and primary drilling (also focused in the Clearwater). Having said that, the company’s recent asset disposition may stand to alter Tamarack’s plans for the months ahead.

What the observations above suggest is that capital spending will be quite a bit lower across the industry in Q4, but that most companies are also likely to meet their budgets for the year; in aggregate, over 75% of the spend for these companies for the year has already been allocated as of September 30. We’ve examined patterns from past years in order to check for seasonality in spending between Q3 and Q4, and noticed that capital expenditures generally increase in Q4 for these companies; between 2018 and 2022, only 2018 saw a decrease in aggregate capital spending over this period.

What could the implied drop in spending mean? We believe there are three main explanations:

- Companies are taking a breather after five-year spending highs in each of the past three quarters

- Companies are diverting cash elsewhere, with acquisitions or dividends/buybacks standing out as possible destinations

- Budget overruns through the first 9 months of the year

With respect to door #2, we’ve seen companies both making deals and taking steps towards distributing capital to shareholders in recent weeks. Crescent Point made a splash days ago with its acquisition of Hammerhead Energy, and Cenovus recently had its share buyback plan approved by the TSX. A slightly depressed heavy oil price outlook for late 2023 and 2024 may also have given management teams pause with respect to spending in the short term. Looking back, however, it is undeniable that 2023 has seen producers deliver on some of the most ambitious capex plans seen in the oilpatch in years. In order to identify new well and transfer activity the moment it takes place, check out BOE Intel.

Editor’s Note: In the initial published version of this article, Canadian Natural Resources Limited’s 2023 capital budget was incorrectly reported as $5.21 billion. The company updated its 2023 capital budget to $5.40 billion in its Q2 2023 release (seen here). The article has since been updated to reflect the current budget.