With the arrival of the new year, producers across Canada have begun putting new capital to work. In order to get a better idea of what the year ahead holds for the Canadian oil patch, we’ve scoured guidance announcements for the companies within our dataset of over 30 public companies. The following data and charts are part of our BOE Intel offering that is coming soon. For more information, click the link. While a handful of companies have not published updated budgets and guidance figures, the data we have seen thus far has helped us identify a number of key themes for the year ahead:

While capital discipline remains key, production set to rise in 2023

- Coming off a year of high oil prices, Canadian producers have paid down enormous levels of debt and generally are in the best financial position that they have been in in years. As a result, the median company in our dataset is guiding to production growth of ~9%, aided in some cases by full year production from acquisitions made in 2022.

Capex expected to show modest 4.5% growth in 2023

- Our dataset, which does not include all of the large caps yet, incorporates about $16.5 billion worth of capital expenditures in 2022 (we’ve used average spending levels for Q1-Q3 to extrapolate full year 2022 spend until Q4 results come in). Based on the mid-point of company guidance, those companies look to expand capex by about $750 MM in 2023, or about 4.5%.

- Whitecap Resources and ARC Resources are driving a good chunk of the increase year over year, as both companies will have record high capex levels in 2023.

- Whitecap will have its first full year with the XTO assets that it acquired last summer, and will look to use free cash flow to support its production growth, debt reduction, dividend payouts and share buybacks. Whitecap has currently set its capital budget at a midpoint of $925 MM for 2023.

- ARC is guiding to a $1.8 billion capital budget, and will be active on the Seven Generations acreage that it acquired in 2021, as well as in its NE BC core Montney areas. ARC is pointing toward 70% of its capital going towards Alberta, and 30% in BC. 2024 capital expenditures guidance is for a decrease back into the $1.5-$1.6 billion range.

- Whitecap Resources and ARC Resources are driving a good chunk of the increase year over year, as both companies will have record high capex levels in 2023.

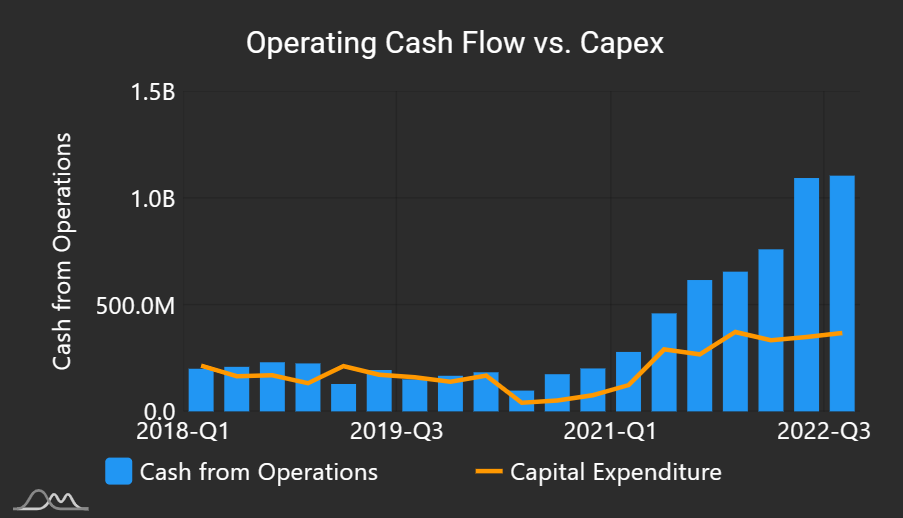

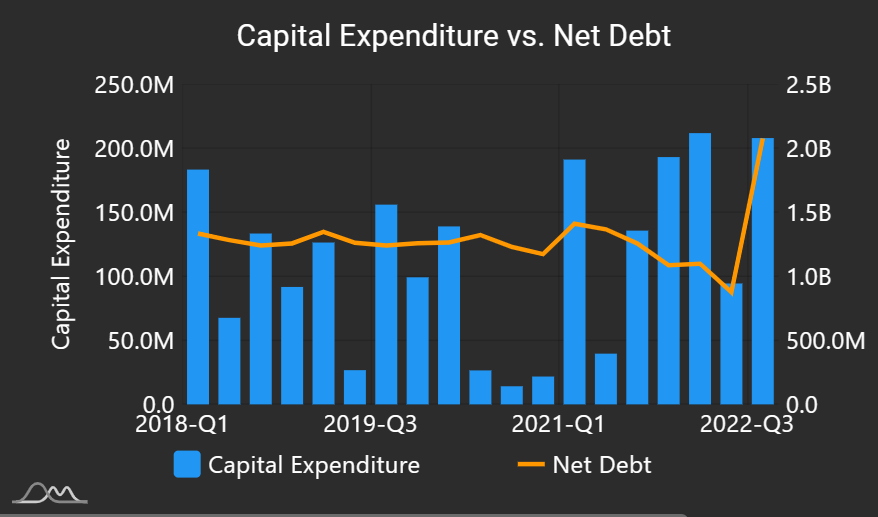

ARC Resources charts from BOE Intel

Whitecap Resources charts from BOE Intel

Companies are looking to hedge less

- While oil and natural gas prices surged in the beginning of the year, both have cooled off over the last number of months. It appears that Canadian producers are feeling optimistic about the future however; of the companies we assessed, more than 44% made clear references to pursuing reduced hedging positions in 2023. In fact, only one company indicated a clear intention to increase their use of hedging in the coming year.

More buybacks, less debt

- Share buybacks, an important use of free cash flow in recent years, are set to be a common occurrence in 2023 as well. Twelve of our assessed companies referenced pursuing share buybacks in the coming year. Paying down debt is another major priority, with just under 50% of companies stating a clear intention to reduce their debt load. The remaining companies have either already reached their debt targets, or did not reference debt as a major component of their plan for the year. As the BOE Intel chart below shows, the Canadian energy industry continues to shed debt at a very impressive pace.