It’s been a rough couple of months for Canadian energy equities, that culminated with the worst day in almost 2 years today. The XEG.to energy ETF in Canada fell by almost 5 percent today, reaching lows not seen in over a year. Tariffs and political drama have been off and on over that timeframe, and headlines out of OPEC+ earlier today that the organization was planning to go ahead with its previously guided-to supply increase added to the negative sentiment today. There had been some hope that OPEC+ may delay its previously announced supply increase, as it had done in other similar circumstances over the last couple of years, but that didn’t come to pass today.

The XEG.to ETF closed at $16/share today, its lowest since February 2004. A capitulatory feel was evident, with volume in the ETF the highest since a washout in March of 2023. It was also the single largest daily drop for the ETF since that same period in March 2023. Will this selloff mark the end of the pain as it did in 2023, or is more pain in store? Only time will tell.

Chart courtesy of StockCharts.com

While the OPEC+ headlines were likely responsible for a good chunk of the losses, not to be overlooked were the fact that tariffs on Canada look set to go ahead just after midnight tonight. Of course with the Trump administration, there is always hope for ‘a deal’, but for now this appears to be the new reality. Of course the details are yet to be fully confirmed when it comes to the energy tariffs, and the threat of retaliation from the Canadian government remains a possibility that will likely contribute to market volatility and keep everyone on edge.

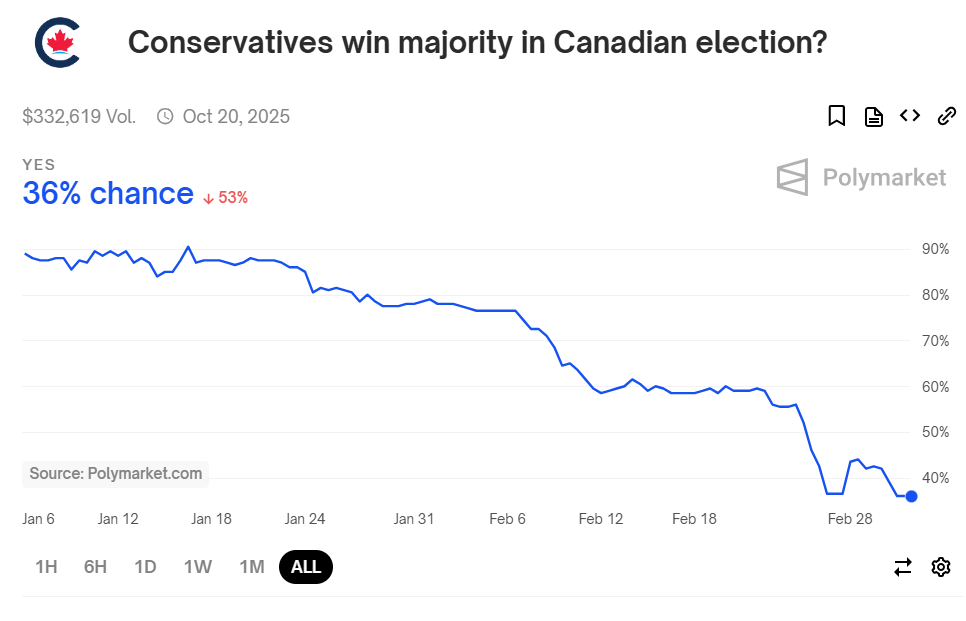

Not helping matters from a sentiment point of view when it comes to Canadian energy is the fact that the political race in Canada seems to be narrowing. What once appeared to be a near lock for a Conservative majority, now appears to be a much closer battle (if you can trust the left leaning political pollsters that is). The polls seem to be leaking into the betting markets as well.

Polymarket suggests a 36% probability of a conservative majority government, and 61% chance that Pierre Poilievre will be the next Prime Minister of Canada. While these odds seem favourable to those who have dealt with Trudeau’s anti-energy policies over the last decade, they are down dramatically from levels seen a couple months ago when Justin Trudeau was pressured into unceremoniously resigning.

The one bright spot in this trifecta of negative headlines? Natural gas. At least for most of the continent that is (sadly Canada lags behind on pricing here as well, although LNG Canada is expected to deliver its first shipment of liquified natural gas in July 2025). In the US, natural gas prices have recently hit more than two year highs on record LNG feedgas, and if one is bearish on crude oil pricing, there might be a silver lining for natural gas producers. As much of the natural gas produced in North America comes in the form of associated gas from producers who really are going after oil and liquids, if there is a drop in liquids pricing then it’s possible that capital gets cut and with it associated gas volumes.

Chart courtesy of StockCharts.com

While Canadian energy looked rocky today, we’re reminded of a famous line: “this too shall pass.”